While forensic accountant Tom Gober was testifying before the ERISA Advisory Council (EAC) meeting on private equity firms in the pension risk transfer (PRT) business in Washington on July 18, I was standing against the back wall of the windowless meeting room, a few feet from Bill Wheeler, vice-chair of Athene Holding Ltd.

Like all 21 guest commenters, Gober was given only 10 minutes to speak and answer questions from 15 council members. He presented slides showing how an anonymous “XYZ” insurance company had reduced its liabilities using offshore reinsurance and grown its assets with securities from its own affiliates. As Gober spoke, I watched Wheeler’s face.

He appeared to listen closely. He leaned forward in his chair and looked calmly at the floor. Wheeler, a former chief financial officer at MetLife and a Harvard Business School graduate, seemed untroubled. He may have been thankful that Gober didn’t identify XYZ life insurer as Athene Annuity and Life.

Later, after Wheeler and colleague Sean Brennan used their 10 minutes to describe Athene as “the most transparent” life insurer, I asked Gober what he thought when Wheeler said that. He told me, “I thought that was the opposite of the truth.”

To tweak or not to tweak “IB 95-1”

The topic of the July 18 hearing was dictated by the SECURE 2.0 Act, a retirement bill that Congress passed in 2022. Section 321 of the Act addresses the requirements that a defined benefit plan sponsor’s fiduciary advisor (an individual, or a consulting firm like Aon or Mercer) must meet when deciding which life/annuity company the sponsor should transfer its plan to (that is, the company from which to buy a group annuity) in the execution of a PRT deal.

Section 321 instructed the Department of Labor (DOL) to revisit those requirements—as first described in Interpretive Bulletin 95-1 (IB 95-1) 28 years ago—to see if they needed to be tweaked. The DOL’s Employee Benefit Security Administration (EBSA) sent a consultation paper on the topic to the EAC for its review and input. The EAC, in turn, solicited input from public. On July 18, the EAC heard testimony from 21 interested parties.

A key issue, for several pensioner-rights advocates represented at the meeting, is whether IB 95-1 should be amended to alert fiduciaries to the growing roles of certain large asset managers ( “private equity,” “private credit,” or “leveraged buyout” companies) in the life/annuity industry, to the complex investment and reinsurance policies of those companies, and to the potential danger of putting discretion over billions of dollars of defined benefit plan assets and responsibility to pay future benefits to millions of retirees (the “liabilities” of the insurers) in their hands.

Over the years, PRT deals have transferred $425 billion in assets and liabilities from corporate defined benefit plans to life/annuity companies, including about $250 billion since 2012 and an estimated $52 billion in 2022. Athene, MetLife and Prudential together accounted for about two-thirds of the 2022 PRT deal volume.

All three have enough surplus capital to handle huge PRT deals. Of the three, only Athene has a “private equity” label, thanks to its affiliation with the giant asset manager, Apollo, within Bermuda-based Athene Holding Ltd. Changing IB 95-1 to flag private equity companies could put Athene at a competitive disadvantage to other large life/annuity companies.

Meet the ‘Bermuda Triangle’

You may have read about the “Bermuda Triangle” phenomenon in the life/annuity business. That’s Retirement Income Journal’s short-hand for a business strategy that Athene is sometimes credited with originating and perfecting after the 2008 financial crisis. The strategy has been widely copied by other financial services firms, including MassMutual and, most recently, Fidelity Investments.

The strategy typically involves coordination between at least three related entities, often companies of the same holding company:

- A life/annuity company sells individual or group annuities to acquire investment capital.

- An affiliated asset manager uses some of that incoming capital to write (“originate”) long-term “leveraged loans” whose returns reflect their “illiquidity premium.”

- An affiliated reinsurer reinsures annuity liabilities under Bermuda’s favorable accounting standards and also attracts fresh capital from foreign investors who want to invest in the U.S. life/annuity business.

The Bermuda Strategy can be complex and opaque. Few people understand exactly how it works. It appears to allow life insurers to invest in riskier, higher-yielding assets while using more flexible accounting rules in certain jurisdictions to eliminate the punitive capital requirements that would make those high-risk assets too expensive for insurers to hold under domestic accounting rules.

The strategy evidently cuts two ways. By reducing its capital requirements, an insurer can make itself more profitable (and its policyholders more secure). But, as some fear, the strategy could also bring the insurer closer to insolvency during credit crises, as in 2008 and 2020.

Athene’s vice-chair speaks

The three most important speakers, for me, were Wheeler, who moved from MetLife in 2016 to become Athene’s president; David Eichhorn, president of NISA, the pension fund bond manager; and Tom Gober, a forensic accountant who studies the assets, liabilities, and reinsurance practices of life/annuity companies.

Along with Wheeler, Athene Holding sent four or five people to the hearing. It was the only life/annuity company offering public comment Tuesday. “We’re the bad guys,” Wheeler said jokingly to me during a break in the EAC meeting. Athene Holding Ltd. encompasses New York-based Apollo Global Management, a publicly-traded company; Athene, a retirement business (including Iowa-based Athene Annuity and Life Company); Apollo Asset Management; and Bermuda-based Athene Life Re, a reinsurer.

Athene has become a lightning rod because it has been the leader in disrupting, reinventing, and (depending on your point of view) either plundering or rescuing a weakened U.S. life/annuity business during the long low-interest-rate period after 2008. During Athene’s 10 minutes of testimony, Wheeler defended his firm, its investment and reinsurance practices, and private-equity firms generally. He rejected the “private equity” label, however. “Let me set the record straight. Yes, we own assets that Apollo originates. That’s eating your own cooking. We’d rather have Apollo assets than assets from some third party,” he said.

“It’s not true that we’re ‘private-equity’ backed,” he added. “We look a lot like Prudential, or MassMutual, or MetLife. [Some people] don’t want you to know that.” He seemed to be distinguishing between firm directly financed by private equity investors and companies like Athene, that have partners who lead private equity investments. He praised private equity firms, saying, “Forty percent of all new capital in the life/annuity industry has come from private equity firms. Traditional life insurers have raised no capital on their own in a decade.” For Athene’s complete letter to the EAC, click here.

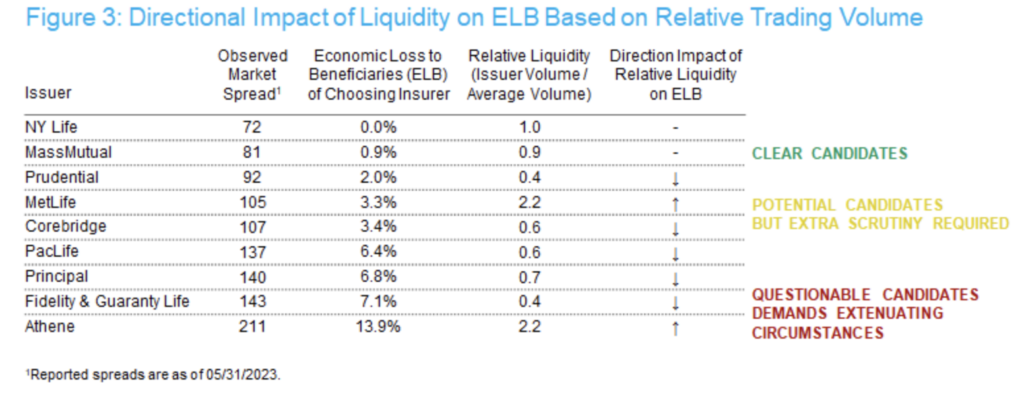

Wheeler was preceded at the commenter’s table by Eichhorn and Gober. Eichhorn co-founded NISA Investment Advisors, which manages over $400 billion in bonds for institutional asset managers. His data showed that, for professional bond buyers like himself, a certain type of debt (Funding Agreement Backed Notes, or FABNs) is considered significantly riskier when issued by Athene than when issued by its competitors or peers in the life/annuity industry. [See NISA chart below.]

Indeed, Eichhorn said he trusts the market prices of FABNs more than the ratings by credit ratings agencies. The NISA website said, “We believe our market-based measure of credit risk conclusively demonstrates an exceptionally wide range of default risk of the various PRT providers. …Any reasonable reading of the ‘safest annuity available’ standard in IB 95-1 would require narrowing the universe of potential PRT providers.”

Gober, in his presentation, focused on the conflicts of interest inherent in certain life/annuity companies’ purchase of assets from sibling firms in the same holding company (“affiliated assets”). As for offshore reinsurance, he called it a “sleight of hand” tactic for reducing the amount of surplus capital supporting pension liabilities.

Tom Gober

Under Bermuda’s accounting rules, pension liabilities (estimates of what the annuity issuer will have to pay out to pensioners in the future) are smaller. Nor does Bermuda impose U.S.-style “risk-based capital” penalties. These penalties raise the owners’ capital requirements when U.S. insurers hold riskier investments.

Bermuda, in effect, doesn’t necessarily require a U.S. life/annuity company’s owners to post as much of its own capital (on top of the savings it manages for the pension plan participants or annuity contract owners) as the U.S. does, given the same pension liabilities. Bermuda-based operations are also not as transparent to the general public as U.S. operations, Gober said.

Potential impact on 401(k) annuity market

After getting feedback from the EAC, the DOL faces a December 29, 2023 deadline for giving Congress its recommendations on amending IB 95-1. “That’s a pretty quick turnaround,” one of last Tuesday’s commenters told me. A member of the EAC told me that the consultation on IB 95-1 was “different than others” and “not part of [the EAC’s] perennial process.”

Last week’s meeting added, in a sense, a new chapter to ongoing discussions between the annuity industry and EBSA over tightening or easing regulations that govern the marketing of annuities to 401(k) plan participants or IRA owners. The state insurance commissions regulate annuities, but the DOL regulates such plans and accounts. There’s potential friction wherever the state and federal regulatory agencies overlap.

In 2016, the Obama DOL singled out marketers of fixed indexed annuities and variable annuities to owners of IRAs to act only in their clients’ “best interests.” (The industry appealed the new regulation in 2018 and a federal appeals judge voided it.) In 2020, the Trump DOL successfully amended a 1975 DOL regulation to say that advisors are committing a “fiduciary act” when they advise clients to roll over 401(k) savings into an annuity. That is, advisors can’t recommend a rollover out of their own self-interest.

Now the Biden DOL is mulling an amendment of IB 95-1 that could tighten the oversight of PRT transactions involving life/annuity companies that are affiliated with major “private equity” or “private credit” companies, such as Athene, that invest in riskier assets, and that buy reinsurance from their own affiliates.

That may be difficult, given the establishment of Athene’s already-large footprint in the PRT market and individual annuity market, and given the steady blurring of the lines between the business practices of Athene and its competitors in the life/annuity industry.

Whatever the DOL recommends to Congress regarding revisions to IB 95-1, it could affect the life/annuity companies that are competing to distribute annuities through 401(k) plans to plan participants. As in the PRT debate, defined contribution plan fiduciary advisors must follow specific rules when recommending an annuity provider. If any factor disparages, hinders or disqualifies a certain type of life/annuity company from the PRT market, the same factor might hinder its competitiveness in the much broader 401(k) market.

© 2023 RIJ Publishing LLC. All rights reserved.