There’s a transatlantic search underway for “capital-efficient savings products” that can give retirement savers the upside potential and downside floors they crave without creating capital-intensive, unhedgeable risks for the life insurers who build them.

Munich Re Group has developed such a product in Europe, and one of its U.S.-based executives, Ari Lindner, introduced it to the 200 or so actuaries and asset managers who attended the Society of Actuaries’ EBIG 2015 conference in Chicago a few weeks ago.

In the separate account product he described, policyholders split their premiums into two, buying a risky asset—an equity mutual fund or balanced fund—and a long-dated put that ensures a return of premium at maturity, which could last as long as 40 years.

Like most variable annuities, the new product allows the contract owners to invest directly in equities or other risky assets. And like fixed indexed annuities, it offers an end-of-term principal guarantee. But it differs from both VAs and FIAs in that it relieves the issuer of “lapse risk” and other risks tied to unpredictable client behavior.

Lapse risk is the risk that policyholders won’t lapse (surrender) their contracts at the rate that insurer actuaries predicted. If experience differs from assumptions, the guarantee may generate economic losses for the insurer, and the mere possibility of this occurrence results in a higher capital requirement.

Lapse risk has created big headaches for European as well as U.S. life insurers. “Almost every major variable annuity writer has absorbed large write-downs on ‘policyholder behavior assumption updates,’” Lindner said. “We’re talking about major players. And the losses have been fairly substantial, if you read the quarterly earnings reports. So the question is, how do we take out that risk?”

A portfolio of puts

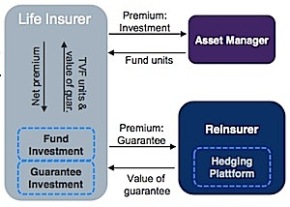

Assume a client who buys a 12-year version of the product with a $100,000 premium. The premium covers three components: the load; an investment into shares of a mutual fund; and the purchase of a terminal 12-year put (an option to sell the fund at a certain minimum price) from the insurer. Behind the scenes, the reinsurer (Munich Re, in this case) manages a portfolio of put options to finance the life insurer’s promise to keep the client whole.

[Technically the reinsurer does not physically trade options but synthetically replicates the insurance liability via a dynamic hedging program, “although this is irrelevant to both the primary insurer and the policyholder,” according to Alex Wolf, senior structurer, and Darryl Stewart, senior consultant, in Munich Re’s Life Financial Solutions unit.]

Prior to maturity, the put gains value when the mutual fund loses market value and vice-versa. The overall account value is stabilized because it is comprised of the sum of the mutual fund value and the value of the put (updated daily). At maturity, if the value of the mutual fund equals or exceeds the terminal guarantee (e.g. the initial premium), the put expires with no value. If the mutual fund doesn’t satisfy the guarantee, the put value would make up the shortfall.

“The policyholder invests in a guarantee asset rather than paying for a guarantee on a running basis,” said one of Lindner’s presentation slides. The initial allocation between load, hedge and investment depends on interest rates and market volatility at the time of purchase. In addition to the load, a policyholder pays an annual mortality and expense risk fee.

How the design conserves capital

The product conserves capital, as noted above, by eliminating lapse risk. The timing of a surrender doesn’t affect the insurer because, at any given point in the life of the contract, the surrender value and the value of the separate account are the same. The product pricing doesn’t depend on an assumption about lapse rates, so there’s no risk of a mismatch between the value of assets that support the guarantee and the guarantee, and therefore no chance of a desperate call for more capital.

In a more sophisticated version of the product, the total premium could be split into the following pieces: a front-end load, an investment budget that’s allocated to a mixed income fund (50% volatility-controlled equity fund and 50% Treasuries), a money market fund and a put for each of the two investment sleeves. Under favorable market conditions, all of the premium could go into the mixed income fund and its put.

For the past two years, brokers and both independent and captive agents of ERGO, the direct writer of life insurance policies within Munich Re group, have sold a product like the one just described, called ERGO Rente Garantie, in Germany. The number of in-force policies is in “the five digits” according to Stewart. The front end load for such a product would be about 5% and the budget for the put would be no more than 15% of the premium.

Would it fly in the US?

Would such a product transplant successfully to the United States? According to Lindner, if life insurers in the U.S. can sell GMAB products, then the Munich Re design should be marketable here—unless regulators object to the fact that the guarantee is part of the policyholder’s account.

The product’s only insurance feature at the moment is its death benefit. It can be configured to accept either single or flexible premiums; a guaranteed minimum withdrawal benefit can be added; roll-ups could be offered; the put could guarantee less than 100% of the premium.

One aspect of the product that might appeal to advisors: transparency. “On a variable annuity in the U.S., you can see the value of the risky asset, and you know there’s a guarantee under certain circumstances. But you can’t see what the guarantee is worth or collect it if you choose to terminate the contract prior to taking the guaranteed pay-out,” said Wolf.

As for the sales force, Lindner raised a couple of questions. How would policy illustrations be handled? (In Europe, Munich Re intends to simplify the current version of its product to make it easier for agents to explain and prospects to understand.) And, would the Department of Labor deem the design to be in what the pending fiduciary proposal calls the “best interest of the client.” As for administrative chores, the value of the put would have to be updated on a regular basis (e.g. daily) and reported to the client.

But there’s no question that life insurers are looking for a new kind of annuity product that can sell in the broker-dealer channel, satisfy the investor’s desire for upside potential and downside protection, and, most importantly, not have a large appetite for capital.

© 2015 RIJ Publishing LLC. All rights reserved.

compensation that they offer distributors and agents to get them to sell their products, typically indexed annuities. Only two of the manufacturers offer no prizes; the other 13 listed their Bahamian golf outings, Tag Heuer watches and other premiums.

compensation that they offer distributors and agents to get them to sell their products, typically indexed annuities. Only two of the manufacturers offer no prizes; the other 13 listed their Bahamian golf outings, Tag Heuer watches and other premiums.