Liquidity Origination/Consolidation Platforms, 2003-2019

IssueM Articles

COVID-19 and the associated economic crisis are set to cause the first decline in global asset management industry assets under management in a decade, according to Cerulli Associates’ latest report, Global Markets 2020: A Sharper View of the Asset Management Sector.

The global analytics and consulting firm expects the global asset management industry to recover and grow after 2020, fueled by increasing demand in developing countries, particularly Asia. Advances in technology and product will give global asset managers more ways to access growing investor segments.

“As the coronavirus pandemic continues to impact the global economy in the second half of 2020 and beyond, asset managers will need to find ways to keep investors in their products and prevent a widespread flight to cash,” says André Schnurrenberger, managing director, Europe at Cerulli Associates.

“Managers should dedicate resources to investor education on how to handle a market correction, implementing scenario analysis from the last significant global drawdown in 2008.” These resources will be especially useful in those countries where emerging middle-class investors have entered the market within the past decade and had not experienced a substantial correction before COVID-19.

As the global economy reacts to the coronavirus pandemic, Cerulli expects mutual fund allocations globally to become more conservative through the first half of the next decade. Global investors will look to re-allocate and assets pulled from equity funds are likely to flow not to bond products, but to money markets. With central banks around the world committing to keeping interest rates low for the foreseeable future, investors may not feel that the yields on bond funds are compelling enough to move them away from the safety and stability of money market vehicles.

The U.S. Federal Reserve has reduced short-term rates to nearly zero in a bid to spur the economy and the European Central Bank was at 0.00% and the Bank of Japan at -0.10% in July 2020. Bond yields are set to remain low for the rest of 2020—and likely into 2021.

Though global markets have stabilized somewhat after substantial losses during March and early April this year, fund managers worldwide stand to lose a significant market performance tailwind in 2020. Losing the aid of market appreciation will be a substantial challenge for managers already facing numerous hurdles, including fee compression, the rise of passives, and an increasing view of asset management as a commodity.

Cerulli expects manager consolidation, which largely paused in the first half of 2020 due to the coronavirus pandemic, to return in 2021 as markets stabilize. Underperforming managers present a ripe target for acquisition by multinational investment giants.

Around the world, investments into private markets slowed in the first half of 2020, with only US$433.7 billion of capital raised. The lockdown measures implemented in many countries to curb the spread of COVID-19 have affected business operations, due diligence, and investment decision-making processes for both managers and investors. Despite the headwinds, however, Cerulli expects investors to continue the process of diversifying into alternatives in search of better long-term returns.

In the institutional space, COVID-19’s effects on investors will be negative in the short term. Its impact will include insurers’ profit margins narrowing due to payouts on policies and pension sponsors reducing contributions where possible to keep their businesses going. However, institutional investors are starting to return to planned projects, boosted by the quick recovery in the financial markets.

“Overall, the volatility in the global financial markets caused by COVID-19 is likely to persist for the rest of 2020,” adds Schnurrenberger. “It is still unclear what the full impact of the coronavirus pandemic on the asset management industry will be, but it will inevitably dominate managers’ thinking and activity in the coming months and years. Nevertheless, those managers that respond effectively to their clients’ needs in these unprecedented times will find a growing opportunity set.”

© 2020 RIJ Publishing LLC.

The U.S. response to the coronavirus pandemic and resulting economic collapse has been impressive in scale and speed, dwarfing the reaction to the 2008 global financial crisis. Provisions in the CARES Act and other measures were designed largely on the assumption that the economic shock would be sharp but short-lived. Policy support was intended to be a temporary bridge lasting a few months as things returned to normal.

With lay-offs mounting and many small businesses on the brink of failure, more fiscal assistance is necessary. A new stimulus round presents an opportunity to rethink employment incentives and get as many people back to work as possible. As the economy reopens, businesses should see demand rise, increasing the need to bring back workers. We need policies to encourage workers to rejoin the labor force, while assisting those who are working and experiencing reduced wages, hours or both.

A voluntary payroll tax holiday could play a pivotal role in boosting disposable income and incentives to work. Although Congressional Republicans are resisting this idea, that is a mistake. If structured correctly, it would also make Social Security more sustainable. The payroll tax withholding rate, currently 6.2% for the employee component, could be cut to zero for the first two years, delivering a much-needed income boost for workers who opt in. The rate could gradually rise after that, returning to 6.2% for the seventh year.

This would increase disposable income for existing workers, which would spur consumption and ignite a virtuous cycle that would encourage even more hiring. Under such a program, an average worker aged 40 earning an average wage ($53,756 in 2019) would receive $15,767 in increased disposable income over the next six years.

As a supply-side incentive to increase hiring, the employer could receive the same kind of tax holiday. Under the CARES Act, employers are allowed to defer 2020 payroll taxes. Outright elimination would deliver an even bigger economic boost. By driving down the after-tax cost of labor, businesses would receive an immediate incentive to hire and retain workers.

The result would be more record-setting job gains and a relatively rapid reduction in unemployment. Employer payroll tax relief would also relieve pressure on small businesses and limit failures and bankruptcies that threaten the economy’s structural potential.

This temporary payroll tax holiday could be offset by raising the retirement age for those who choose to participate. For instance, the full retirement age, now 67, could be increased by six months each year until it reaches 78 or retirement, whichever comes first. According to the Social Security Administration, the net present value of the Social Security Trust Funds’ unfunded liabilities over the next 75 years is $16.8 trillion.

This reform could eliminate $14.1 trillion of that deficit over the next 60 years, assuming a weighted average take-up rate of 66% among current workers. Moreover, roughly 36 million new entrants to the workforce over the next 15 years would produce extra savings of $4 trillion.

For those seeking current income, a higher net paycheck now would be available in exchange for delaying retirement. This could be attractive for younger workers whose expected retirement date is decades away. Aiding those who are working puts more money in the pockets of consumers, in turn lifting aggregate demand. Since the payroll tax cut is progressive — the 6.2% tax is only charged on the first $137,700 in personal income — lower-income workers, precisely those who need the most assistance right now and are most likely to consume the increased income, will see the largest relative increases in take-home pay.

Unlike a mandatory reform, workers who opt for the payroll tax holiday would do so willingly in exchange for an extended retirement age. Those who wish to retain their current retirement benefits would continue in the existing program. This would give them greater freedom and flexibility to customize their retirement.

A payroll tax holiday is a useful incentive to stimulate employment while creating an opportunity for entitlement reform that will shore up Social Security for future generations. Clearly, this proposal must be just one component of a much larger fiscal package. Such measures should be complemented by continued advances in public health policy and support from monetary policy. We should grab this chance to design a program that returns the U.S. to work, while enhancing its financial stability and economic growth.

John B. Taylor, Stanford economics professor and Hoover Institution fellow, also contributed to this article.

An AM Best analysis of U.S. life/annuity companies’ investment strategies amid the past decade of low interest rates found that the number of companies considered non-interest-sensitive more than doubled those deemed interest-sensitive.

However, those companies exposed significantly to interest rates have managed an average 76% of the industry’s invested assets in the last 10 years, and have different investment risk tolerances and strategies to aid in backing a product profile that is linked more to interest rates.

The low interest rates continue to hamper the life/annuity (L/A) industry, and with the COVID-19 pandemic impact, the trend is likely to exacerbate. In a new Best’s Special Report, “Interest Rates: Different Impact Severity, Different Strategies,” AM Best notes that insurers have been strategically de-risking their product portfolios for some time to counter the impacts on spread compression and earnings volatility.

Strategies have included exiting, re-pricing or de-emphasizing certain business lines, particularly those that are interest-sensitive. According to the report, companies considered interest-sensitive were those with a liability and premium mix concentrated in individual and group annuities, deposit-type contracts and interest-sensitive life products, as defined by the NAIC for statutory statement reporting.

Interest-sensitive companies typically generate the bulk of the industry’s earnings. Based on 2019 capital and surplus levels, interest-sensitive companies have nearly four times the amount of capital on average—approximately $2.3 billion, compared with roughly $610 million for non-interest-sensitive companies.

Commercial mortgage loans remain a staple of life insurers’ investment holdings, growing more than 80% to $578.5 billion in 2019 from $317.1 billion in 2010. Interest-sensitive companies were responsible for the growth, as their average exposure rose to 8.2% in 2019 from a low of 5.8% in 2010, versus a slight decline in non-interest-sensitive companies, whose average exposure came to 4.2% of invested assets in 2019.

Pre-tax net operating gains have been relatively consistent for non-interest-sensitive companies. In contrast, interest-sensitive companies have reported much more fluctuation over the last 10 years, although earnings have been consistently positive. Interest-sensitive companies also earn higher yields on average than non-interest-sensitive companies.

The low interest rates will remain a key obstacle as L/A insurers continue to invest new money, as well as the proceeds from higher-yielding maturing assets, into new assets at lower rates. The COVID-19-fueled economic slowdown has amplified the likelihood of dampened earnings in 2020 for spread and fee-driven businesses.

AM Best believes there is the potential for further swings in the equity markets, and will be looking closely at companies’ asset-liability management programs as closely matched assets and liabilities can immunize against interest-rate sensitivities.

© 2020 RIJ Publishing LLC.

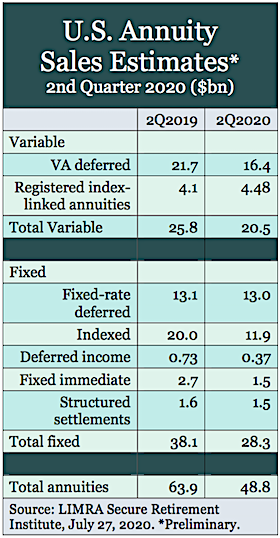

Total U.S. annuity sales fell to $48.8 billion in the second quarter of 2020, down 24% from the second quarter of 2019, according to preliminary results from the Secure Retirement Institute (SRI) U.S. Individual Annuity Sales Survey.

“The second quarter annuity sales decline is a direct result of the global pandemic and its economic fallout,” said Todd Giesing, senior annuity research director, SRI, in a release this week.

“In addition to the record-low interest rates and continued market volatility, social distancing has significantly disrupted business operations for companies and advisors over the past three months,” he added.

“While most annuity products saw double-digit sales declines, products that offer investment protection, like fixed-rate deferred and registered index-linked annuities, were able to maintain and even grow business in the second quarter.”

After four consecutive quarters of growth, total variable annuity (VA) sales dropped 20% in the second quarter to $20.5 billion. VA sales were $46.5 billion in the first half of 2020, down 4% from the first half of 2019. This was the lowest quarterly level of variable annuity sales since 1996.

While overall VA sales declined, registered index-linked annuity (RILA) sales (also known as structured variable annuities) continued to grow. RILA sales were almost $4.5 billion in the second quarter, 8% higher than in second quarter 2019. RILA have now seen quarter-over-quarter growth for 22 consecutive quarters. Year-to-date, RILA sales were $9.4 billion, up 22% from the first half of 2019.

“As we saw over the last few quarters, the low interest rates have hampered fixed indexed annuity (FIA) rates. As a result, we believe advisors are gravitating to RILAs, which offer downside protection with greater upside potential,” Giesing said.

The growth in RILA sales has come at the expense of FIA sales. In the second quarter, FIA sales fell 41% to $11.9 billion. This is the lowest quarterly total for FIAs since first quarter 2015. Year-to-date, FIA sales totaled $28.1 billion, falling 26% compared with prior year.

Total fixed annuity sales were $28.3 billion in the second quarter, a 26% decline from second quarter 2019. In the first half of 2020, fixed annuity sales dropped 24% to $58.1 billion.

Fixed-rate deferred annuity sales jumped 33% from the prior quarter to $13.0 billion. Year-to-date, fixed-rate deferred annuity sales totaled $22.8 billion, which is 19% lower than prior year results.

“Low interest rates dampened fixed-rate deferred annuity sales in the first quarter. But, as we saw during the Great Recession, sles of these products soared in the second quarter as consumers looked to protect their investment from market volatility and losses,” Giesing said.

Income annuity sales suffered as a result of historically low interest rates. Single premium immediate annuities (SPIAs) were $1.5 billion in the second quarter, down 44% from the second quarter of 2019. This is the lowest quarterly level of SPIA sales in 13 years. Year-to-date, SPIA sales were $3.4 billion, down 38% compared with sales results from the first six months of 2019.

Deferred income annuity sales (DIA) were cut in half to $370 million in the second quarter. Year-to-date, DIA sales were $840 million, sinking 38% from prior year results. “We believe investors will hold off purchasing income annuity products, hoping interest rates rebound over the next 6–12 months,” Giesing said.

Preliminary second quarter 2020 annuities industry estimates are based on monthly reporting, representing 81% of the total market. A summary of the results can be found in LIMRA’s Fact Tank.

The top 20 rankings of total, variable and fixed annuity writers for the first half of 2020 will be available in August, following the last of the earnings calls for the participating carriers.

© 2020 RIJ Publishing LLC. All rights reserved.

More than half (57%) of Americans say that they or a close family member have been financially impacted by COVID-19, according to Charles Schwab’s 2020 Modern Wealth Survey. But the survey also revealed positive changes in Americans’ financial behaviors.

According to the survey:

Americans report that their overall happiness depends much more on the quality of their personal relationships than on the amount of money they have. Still, only one quarter feel highly confident about reaching their financial goals—down from one-third when surveyed in January 2020.

Schwab’s 2020 Modern Wealth Survey is comprised of data gathered from 1,000 respondents in January 2020 before the widespread COVID-19 outbreak in the U.S., and again in June 2020.

When asked in June “what it takes to be financially comfortable now,” Americans, on average, named a net worth of $655,000. say it takes much less than it did in January. That was down nearly 30% from the January 2020 survey, when their comfort level stood at an average of $934,000.

The bar for the level of assets that Americans think it takes to be considered wealthy has been lowered as well. Today they feel that an average of $2.0 million in net worth equates to wealth, down 23% from an average of $2.6 million in January.

In the midst of the COVID-19 pandemic, 30% of survey respondents say they or a family member have experienced a salary-cut or reduced work hours, and 25% say either they or a family member have been furloughed or laid off. Millennials are the most affected of all generations, with 41% stating that they or a family member have experienced one of these issues.

Regarding financial stress (on a scale of 0 to 100), the survey showed that Americans are almost 15% more financially stressed today than they were at the end of 2019. Americans also expect their financial stress levels to stay somewhat elevated even after the pandemic passes.

In both the January and in June surveys, Millennials were the most financially stressed generation and Baby Boomers were the least financially stressed.

Logica Research conducted both waves of the Schwab survey, in which 1,000 Americans aged 21 to 75 were polled. Quotas were set to make each wave of the survey demographically representative. The margin of error for the total survey sample is three percentage points.

Athene Holding Ltd., the $142 billion owner of life insurers and a Bermuda-based reinsurer, will release financial results for the second quarter 2020 on Wednesday, August 5, 2020, before the opening of trading on the New York Stock Exchange.

The news release, financial supplement, and earnings presentation will be available on the ir.athene.com website. Management will host a conference call to review Athene’s financial results on the same day at 10:00 a.m. ET.

Conference Call Details

Live conference call: Toll-free at (866) 901-0811 (domestic) or (346) 354-0810 (international). Conference call replay available through August 19, 2020 at (800) 585-8367 (domestic) or (404) 537-3406 (international)

Conference ID number: 4259196

Live and archived webcast available at ir.athene.com

Athene, through its subsidiaries, issues, reinsures and acquires retirement savings products designed for the increasing number of individuals and institutions seeking to fund retirement needs. The products offered by Athene include:

Athene had total assets of $142.2 billion as of March 31, 2020. Its principal subsidiaries include Athene Annuity & Life Assurance Company, a Delaware-domiciled insurance company, Athene Annuity and Life Company, an Iowa-domiciled insurance company, Athene Annuity & Life Assurance Company of New York, a New York-domiciled insurance company and Athene Life Re Ltd., a Bermuda-domiciled reinsurer.

Pacific Life’s commission-free variable annuity and fixed indexed annuity are now integrated with the Orion Advisor Solutions platform and available for purchase by registered investment advisors for their clients, the insurer announced this week.

Orion is a “tech-enabled fiduciary process” or platform that enables “financial advisors to prospect, plan, and invest” within a single platform, according to a release.

The Orion integration will allow financial advisers to monitor and bill on their clients’ tax-advantaged retirement-income solutions. RIAs can manage a client’s portfolio of both taxable and tax-advantaged assets within a single workstation. This feature allows advisers to combine investments and insurance products more easily.

To support its outreach to RIAs, Pacific Life has added a dedicated RIA channel team, and “continues to add new custodians and insurance licensing companies to make it as simple as possible for financial advisors to include critical guaranteed income in their clients’ portfolios.”

The Federal Reserve issued the following statement this week:

The Federal Reserve is committed to using its full range of tools to support the U.S. economy in this challenging time, thereby promoting its maximum employment and price stability goals.

The coronavirus outbreak is causing tremendous human and economic hardship across the United States and around the world. Following sharp declines, economic activity and employment have picked up somewhat in recent months but remain well below their levels at the beginning of the year.

Weaker demand and significantly lower oil prices are holding down consumer price inflation. Overall financial conditions have improved in recent months, in part reflecting policy measures to support the economy and the flow of credit to U.S. households and businesses.

The path of the economy will depend significantly on the course of the virus. The ongoing public health crisis will weigh heavily on economic activity, employment, and inflation in the near term, and poses considerable risks to the economic outlook over the medium term.

In light of these developments, the Committee decided to maintain the target range for the federal funds rate at 0 to 1/4 percent. The Committee expects to maintain this target range until it is confident that the economy has weathered recent events and is on track to achieve its maximum employment and price stability goals.

The Committee will continue to monitor the implications of incoming information for the economic outlook, including information related to public health, as well as global developments and muted inflation pressures, and will use its tools and act as appropriate to support the economy.

In determining the timing and size of future adjustments to the stance of monetary policy, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective.

This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.

To support the flow of credit to households and businesses, over coming months the Federal Reserve will increase its holdings of Treasury securities and agency residential and commercial mortgage-backed securities at least at the current pace to sustain smooth market functioning, thereby fostering effective transmission of monetary policy to broader financial conditions.

In addition, the Open Market Desk will continue to offer large-scale overnight and term repurchase agreement operations. The Committee will closely monitor developments and is prepared to adjust its plans as appropriate.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michelle W. Bowman; Lael Brainard; Richard H. Clarida; Patrick Harker; Robert S. Kaplan; Neel Kashkari; Loretta J. Mester; and Randal K. Quarles.

The Securities and Exchange Commission has charged Houston-based VALIC Financial Advisors Inc. (VFA) in a pair of actions for failing to disclose practices that generated millions of dollars in fees and other financial benefits for VFA. Teachers and other investors were affected, the SEC said.

In the first action, the SEC found that VFA failed to disclose that its parent company paid a for-profit entity owned by Florida K-12 teachers’ unions to promote VFA and its parent company services to teachers.

In the second action, the SEC found that VFA failed to disclose conflicts of interest regarding its receipt of millions of dollars of financial benefits that directly resulted from advisory client mutual fund investments that were generally more expensive for clients than other mutual fund investment options available to clients.

“VFA agreed to pay approximately $40 million to settle the charges in these two actions. In the first action, VFA agreed to cap advisory fees for all Florida K-12 teachers who currently participate (and, in some cases, those who prospectively participate) in its advisory product in Florida’s 403(b) and 457(b) retirement programs. This will result in significant savings for thousands of teachers,” an SEC release said.

© 2020 RIJ Publishing LLC. All rights reserved.

Willis Towers Watson and Aon, two publicly-traded, global, diversified human resource and financial consulting firms are looking to create large defined contribution retirement plans—”Pooled Employer Plans,” or PEPs—and invite dozens or hundreds of smaller companies to join.

That was my takeaway from reading their comments in response to the Department of Labor’s (DOL) Request for Information about potential conflicts of interest as financial services companies take advantage of the 2019 SECURE Act to initiate retirement plans, serve as the plan fiduciary, and also sell their own products to the participants.

“Willis Towers Watson is considering establishing a PEP [Pooled Employer Plan] and becoming a PPP [Pooled Plan Provider],” the firm said in its letter to the DOL. Aon’s letter said, “The Aon PEP is designed to be a bundled solution for participating employers, utilizing the expertise of both affiliated and non-affiliated service providers of Aon.”

The era when small business owners often relied on their own personal (but not necessarily pension-savvy) financial advisers to help them start tiny, over-priced, labor-intensive 401(k) plans for themselves and a handful of employees—or go without a plan at all—may be ending on January 1, 2021. That’s when PEPs can go live.

It’s possible that the history of retirement savings in the U.S. is about to turn a corner. The current moment reminds me of the early 1980s, when deregulation began to transform the banking and health insurance businesses.

Or PEPs could turn out to be a small phenomenon, already enabled under current law. In his comment letter, attorney Robert Toth said that the new PEPs, though now formally permitting unrelated employers to join single plans, won’t in practice add much to the status quo, beyond offering those employers consolidated annual reporting. In PEPs each employer will remain a co-sponsor of the plan, rather than ceding sponsorship to the PPP.

“What could have happened in SECURE, but did not, was to turn 401(k)s into a pure commodity, with employers not having much of any responsibility other than adopting it,” Toth said in an email to RIJ. “AON, for example, is not sponsoring the plan. They are merely a sort of ‘super’ service provider of the type we are already using.”

Instead, the PEP rules specifically kept the traditional obligations of the employer/sponsor; they are treated as if they were sponsoring their own plan, with all the obligations.

It’s confusing, and it’s not at all clear where all this will lead.

Many of the other 30 letters to the DOL—all from law firms, trade associations, or specific companies, plus AARP—attested that financial services companies, or different arms of the same company, should be able to provide oversight to the plan while marketing their products to plan participants.

Some firms said the DOL needs to issue new and specific exemptions from certain existing conflict-of-interest prohibitions before they can legally offer 401(k) plans. Empower Retirement’s letter said, perhaps signaling its interest in marketing group annuities to participants in its own PEP:

“We do not believe there is an existing prohibited transaction exemption that would allow a PPP or an open MEP sponsor, acting with investment manager under ERISA Section 3(38), to retain compensation associated with general account group annuity contracts. Therefore, we recommend the DOL engage with the industry in discussions about a workable prohibited transaction exemption to allow insurance company commercial entities operating as PEP or open MEP sponsors to offer proprietary general account products.”

Empower expressed a definite concern that the DOL rules currently don’t make it clear that existing full-service plan providers like itself can offer retirement plans, be its own primary watchdog, largely determine its own compensation, and offer proprietary products, without committing a conflict-of-interest violation under current law.

Transamerica, which has a history of serving as the recordkeeper for Multiple Employer Plans (a predecessor of PEPs), also submitted a letter. It asked the DOL to ensure that a trustee of a PEP could transfer the chore of collecting participant contributions to a PEP 401(k) account to a recordkeeper like Transamerica. Evidently, Transamerica wants to make sure that it has a seat at the table in PEPs.

I was scouring the letters for references to annuities. A letter from attorney Steve Saxon of the Groom Law Group sought to clarify the rules around the setting of direct or indirect compensation—revenue sharing, for instance—for fixed annuity providers that may or may not be affiliated with the PEP recordkeeper. He seemed to tie fixed annuities with target date funds; adding an annuity to a target date fund is one way that a lifetime income feature could be added to a 401(k) plan.

My sense is that the Trump DOL leans toward deregulating the retirement industry. In effect, that’s what the SECURE Act seems to have done by letting a wide variety of companies start offering retirement plans and, to an unprecedented degree, letting them police their own conduct to an unprecedented agree. (As noted above, Bob Toth doesn’t agree with my dramatization of the situation.)

This contrasts sharply with the Obama DOL’s fiduciary rule, which would have extended the umbrella of consumer protections that govern tax-deferred employer-sponsored retirement plans to include tax-deferred brokerage IRAs. The current Labor Secretary, Eugene Scalia, was part of the legal team that led the successful fight to void the Obama DOL’s “fiduciary rule.”

I have been wary of the SECURE Act because its public policy goal was never transparently stated. Bipartisan sponsors of the bill said it would help small companies “band together” to bargain for better, less expensive retirement plan services.

That’s not quite how the bill was ever meant to foster new economies of scale, in my understanding. Rather, it appears to encourage the creation of industry-led retirement plans, run by a wide variety of companies, that will serve dozens or hundreds of small companies and their employees. I’ve been told that the two descriptions amount to the same thing, but I disagree.

© 2020 RIJ Publishing LLC. All rights reserved.

The Federal Reserve reiterated its intention to “act as appropriate to support the economy” at the conclusion of this week’s policy meeting while worrying that resurgence of the virus threatens to derail the recovery.

Federal Reserve Chair Jerome Powell emphasized the importance of fiscal policy in supporting the recovery, a not-thinly veiled hint that Congress (or, more specifically, Senate Republicans) need to get their act together.

No new policy measures were announced although Powell did hint that the policy review would be complete by September. Overall, a dovish message. The Fed intends to maintain accommodative financial conditions for years.

The FOMC statement was little changed from June, with the most notable addition being:

“The path of the economy will depend significantly on the course of the virus.”

This is not exactly news for most of us, but the Fed felt it important to emphasize that there is no tradeoff between the economy and public health. Until the virus comes under control, the economy can’t full recovery. The Fed is especially concerned that a resurgent virus already worsens the outlook. From Powell’s opening statement:

“Indeed, we have seen some signs in recent weeks that the increase in virus cases and the renewed measures to control it are starting to weigh on economic activity.”

Powell reviewed the Fed’s actions to support the economy and highlighted the importance of fiscal policy in minimizing the extent to the recession:

“Elected officials have the power to tax and spend and to make decisions about where we, as a society, should direct our collective resources. The fiscal policy actions that have been taken thus far have made a critical difference to families, businesses, and communities across the country. Even so, the current economic downturn is the most severe in our lifetimes. It will take a while to get back to the levels of economic activity and employment that prevailed at the beginning of this year, and it will take continued support from both monetary and fiscal policy to achieve that.”

Powell commented heavily on fiscal policy, including praising the steps taken to date while making clear that the job is not done. It is hard to interpret Powell’s position as anything less than a rebuke to Senate Republicans who have positioned the U.S. economy to fall over a fiscal cliff despite months of warning.

Powell could not be happy that he has to be the adult in the room; the Fed would prefer to stay out of fiscal policy. My suspicion is that he doesn’t think staying quiet is an option. Why? Because buried under Powell’s plead for more fiscal support was the implication that the Fed would be unable to compensate for a fiscal retreat.

To be sure, in response to a reporter’s question Powell said the Fed has more tools available. Those tools, however, would not be sufficient to compensate for the fiscal cliff that lies ahead.

Powell said that meeting participants discussed the policy and strategy review and that they will “wrap up our deliberations in the near future.” That to me sounds like September. He did not give any hints as to the outcome of that process. He played his cards a little closer to his vest than I anticipated. We will need to wait until the Fed releases the meeting minutes to learn more about the discussion.

The overall message was dovish: Powell indicated that disinflationary pressures were likely to dominate for the foreseeable future, that the recovery would not happen quickly and hence unemployment would remain persistently high, and that people really need to stop asking him when they will consider raising rates. That question is so far from his mind that he can’t even begin to answer it.

Bottom Line: The Fed remains committed to accommodative policy. I expect that the Fed will conclude its policy review by September and then they will be free to take additional action. The three most obvious future actions are enhanced forward guidance, shifting asset purchases to the long-end of the yield curve, and yield curve control at the short end. Those would most likely occur prior to an expansion in the pace of asset purchases.

© 2020 Tim Duy’s Fed Watch. The original blogpost was published here.

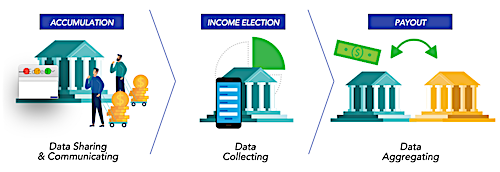

Before income-generating annuities can become a common feature in 401(k) plans—as they are in TIAA’s 403(b) plans—plan recordkeepers will need an easier way to swap data with the life insurers who badly want to market annuities through those plans.

The SECURE Act of 2019 partly relieved plan sponsors of legal anxiety about offering annuities. But it didn’t solve the need for headache-free administration of annuities, which, like molting insects, are born in plans and take flight after participants retire.

“With the passage of the SECURE Act, the fiduciary concern is no longer the primary concern,” said Mike Westhoven, who has worked for years on this issue. “So the top concern now is about administration. All parties know they can’t have messy one-off connections. They want one place to access data on a variety of products.”

Westhoven now works for Micruity, a tech startup with a blueprint for the much-needed data hub. He and Micruity CEO Trevor Gary have been running demos of their “middleware” solution for asset managers and life insurers, who could include it in their proposals to plan sponsors.

Trevor Gary

Micruity’s solution can accommodate the inclusion of any type of annuity in a 401(k) plan. That flexibility is essential, because 401(k) annuity can take many shapes. The annuity can be purchased in or outside the plan, and with multiple premiums or a lump sum. It can require an “opt-in” by the participant or use a default.

As for the contract itself, it might be a permanently liquid deferred variable annuity, or an irrevocable life annuity, or a tax-deferred QLAC (qualified longevity annuity contract). The participant might switch on the guaranteed income stream at retirement, or after 10 to 20 years, or never. The plan sponsor might offer annuities from one insurer or from two or three. Given the evolving state of this industry, all options are on the table.

Selling one annuity to a retail client can be complicated; scaling the sale of dozens or hundreds annuities to waves of retiring plan participants every year is much more so. The plan’s existing stakeholders—the recordkeeper, asset managers and participants—need to accommodate the data needs of one or more annuity providers.

“You need a system to keep the books and records straight,” said Mark Fortier, who in 2012 helped add income riders from three life insurers to an AllianceBernstein TDF in United Technology Corp.’s 401(k) plan. “Someone needs to connect the recordkeeper data with the insurer data, the way it’s currently done on the investment side. You need an entity in the middle.”

Ideally, there should be a single point of contact where every entity can access all the data that’s required to fund participants’ annuities, close the sale of the annuity at retirement, and make sure participants receive checks at the correct addresses throughout retirement.

Less than three years ago, Toronto native Trevor Gary was on the pension actuarial team at Deloitte Canada working on longevity risk swaps. Recognizing the need for personal pensions in the U.S., he decided to build a retail app with which individuals could calculate the gap between their expected retirement expenses and their expected Social Security benefits.

“Then on the back end of the app, our system would enable people to pay as little as $100 would be the Micruity system, where people could contribute $100 every payday to an annuity,” Gary, who is 30, told RIJ recently. “We would have annuities from eight different providers. I wanted to build it on the blockchain. Everybody took a meeting with me but they all said, ‘You’re nuts.’”

Instead, Micruity spent four months in a tech incubator program in Des Moines, the Global Insurance Accelerator, getting mentored by life insurance executives. There Gary learned about the opportunity in the 401(k) annuity space for a service that could track participant data to and through retirement. after they’d bought annuities and retired.

“The [life insurers] said, ‘When people leave the plan, we need to be able to track them.’ That was the Eureka moment for me,” Gary said. “From there, we built our current system from scratch.”

Last April, Micruity made presentations of his system to an audience at SPARK, the association of recordkeepers. This spring, Gary and Westhoven produced a webinar on the Micruity system called, “Making Lifetime Income Real.” As they explain in the webinar, Micruity’s product has three components:

“The sponsor is thinking, ‘This is a new product, so how do we make the process as frictionless as possible?’ Westhoven said. “They don’t want to add a speed bump that makes it difficult to use. With participants, there’s no such thing as a speed bump; every obstacle to usage is more like a brick wall.”

Mike Westhoven

Outside observers are encouraged by Micruity’s efforts so far. “The data hub and administration is the foundation, but Micruity could probably help on the participant experience and education, if stakeholders desire,” said Fortier. “Data-privacy, administration, and the regulatory aspects of education between recordkeepers and insurers have risks that have challenged the unbundled approach in the past.”

Robert Melia, the executive director of the Institutional Retirement Income Council (IRIC), a coalition of plan providers started by Prudential when it launched its IncomeFlex TDF/GLWB, told RIJ that Micruity could bring standardization to what is still a disjointed business.

“Micruity could say, ‘Let us provide these services, and we’ll establish the standardization that’s needed to drive annuities in DC plans,’” Melia said. “They have the credibility, the reputation and the knowledge to put it all together. Standardization, more than anything else, might propel the income part of the DC industry into the future.”

Legal liabilities and data gaps are not the only things stopping plan sponsors from adopting annuities. Participants aren’t demanding annuities, or pressuring employers to offer them—though that’s not necessarily a deterrent for Micruity and its clients. (“The plan sponsors say that participants aren’t asking for annuities. But participants didn’t beg for TDFs either,” Westhoven told RIJ.)

Micruity’s End-to-End Service

Lack of active demand for annuities could be a problem, however. The target market for annuities includes participants who’ve been defaulted into TDFs. Their very passivity makes them attractive to annuity vendors, since they can be defaulted into a GLWB rider as they near retirement. But will plan sponsors acquiesce to such an arrangement, especially if the rider costs as much as 100 basis points per year?

Efforts by full-service plan providers like Prudential and Empower to market TDF/GLWB products to their institutional clients have yielded lackluster results. Westhoven’s former employer, DST Systems (since acquired by SS&C Technologies), created middleware called RICC (for “Retirement Income Clearinghouse Calculator”), but it has remained largely on the shelf.

Historically, annuities have shown the most promise in two distinct types of plans. They appear to work well in 403(b) plans, where millions of people have access to TIAA annuities. They also seem to be a good fit at large companies that recently closed defined benefit pensions and where a critical mass of employees misses an income option. United Technologies is the singular example of such a company.

Micruity will be aiming its future marketing efforts at just such large firms. “We’re looking at the top 1,600 plans, with a combined 20 million or more participants, Gary told RIJ. “These plans have strong human resource teams, and often have a unionized or union-like environment. They employ a lot of mid-market Americans, and their turnover rate is low as they get closer to retirement. These are the plans where it will start. And once momentum catches on, changes will trickle down to smaller plans.”

© 2020 RIJ Publishing LLC. All rights reserved.

A retirement income budget can be defined as the amount of money that one can generate on a gross (pre-tax) basis from all potential sources. A spending budget in retirement in important, but an income budget should come first. It sets the limits of the spending budget.

Retirees can generate income, for instance, from Social Security, a company pension, an insured annuity, investments (including earnings and principal), home equity, as well as other sources. Individual sources of income could be constant, increasing, or decreasing. The combined income should ideally be designed to last for the lifetime needs and to meet the goals of the individual or couple.

The challenge stems from the complexity of addressing individual uncertainties regarding life expectancy, financial markets, and events that may require an unknown financial expenditure such as home repair, a real estate assessment, or long-term care. (To help predict life expectancies, the American Academy of Actuaries offers an Actuaries Longevity Illustrator.)

Among the actuarial principles that apply to retirement income budgeting are periodic reevaluation and risk pooling (specifically longevity pooling). Without longevity pooling, an individual might need to plan to spend a fixed amount of assets over the longest plausible lifetime, resulting in less income each year.

Longevity pooling can provide more each year by allowing the individual to plan around the average longevity of many similarly aged retirees. It shares a pool of assets that provides lifetime income to all participants regardless of how long they live. Social Security, defined benefit pension plans, and lifetime annuities sold by insurance companies are examples of this practice.

This report describes three general approaches for drawing down personal savings and assets that are not part of a longevity risk pool. All three approaches could include either or both tax-qualified and non-tax-qualified funds, thereby adding tax consequences as a consideration.

The required minimum distribution (RMD) approach entails an annual redetermination of the amount to withdraw, based on an approximation of life expectancy and the account balances at the end of the prior year.

The approach is simply to draw down assets (from qualified and non-qualified sources) at the rate specified for RMD, either starting at age 72 or before. (That is, the RMD approach works even if the individual has not reached the IRS’ “required beginning date.”)

This approach improves on other simple approaches such as the “X% Rule” (e.g., 4% rule), which do not adjust for remaining life expectancy. With other simple approaches, a market decline could mean that the income doesn’t last for the individual’s entire lifetime, doesn’t generate enough income to maintain the retiree’s standard of living, or results in an larger-than-desired bequest.

Pros. The calculation is relatively simple and can be done by the retiree with the published values in the IRS tables. The annual drawdowns are based on the life expectancy tables, so the income will continue throughout a lifetime while automatically adjusting for a reducing life expectancy. This method doesn’t require investment return assumptions because actual returns are reflected in the assets supporting the next year’s spending level.

Cons. The life expectancy used is “one size fits all.” It is not tailored to an individual’s situation. It is based on the lives of the retiree and a beneficiary (with a 10-year-younger age for the beneficiary), and thus will understate the amount of income that can be withdrawn for only a single life expectancy.

It neglects to recognize health status, so a person in poor health might want to withdraw funds more rapidly. Income will vary from year to year. The greater the investment allocation to equities, the larger the annual swings in income could be. There is no formal inflation adjustment, although, absent investment volatility, income often will rise in earlier years and fall much later in retirement. In addition, this approach does not coordinate income from other sources with the income generated by the investments.

The deterministic scenario approach requires assumptions such as life expectancy, the overall investment return, and possibly inflation. The life expectancy is calculated from a mortality table and is based on current age and gender. This is then often adjusted to reflect health status, conservatism (addition of several years to life expectancy),

and the availability of other reliable sources of income.

The investment-return assumption can range from a conservative rate to an actual expected return based on the portfolio’s asset allocation and capital market expectations. The calculations can be done with either set of investment return assumptions to provide a range of outcomes.

Then, based on the assumed life expectancy, expected investment return, and the amount of retirement savings, an expected income level is determined. The model can also be adjusted for annual increases in income, modifications to desired income at later stages of retirement, and market volatility. It can also encompass other sources of income.

There is the option to consider the impact of longevity pooling by measuring the results of alternative approaches that take into account the purchase of fixed income immediate annuities or delayed Social Security.

This approach should be revisited annually to adjust for past investment income experience, actual expenditures, changes in the planned income pattern, or modified mortality, investment, and inflation assumptions.

Pros. Calculators for this approach can be found on the Internet, provided by investment managers, brokers, and financial bloggers. Performing calculations with several sets of assumptions, particularly those relating to investment income, life expectancy, and inflation, can reveal the range of affordable lifetime income possibilities.

The method provides a specific amount that can be available for spending, which makes it easy to put into action; however, the calculations must be periodically updated to reflect actual investment returns.

Cons. Care must be taken in the choice of assumptions. Use of unrealistic assumptions can lead to either overstating or understating an affordable lifetime income level. Modeling can be more complex when considering non-investment-portfolio sources of income.

Like the deterministic scenario approach, the probabilistic scenario approach is based on a model with certain assumptions. Instead of relying on a single life expectancy or investment return assumptions, it uses stochastic modeling to generate thousands of simulations based on a range of possible experience.

A planning strategy generally comprises an annual income goal, which can be flat or varying, and includes all sources of income Within the simulations, rates of return are generated for each year based on Monte Carlo techniques. Rates of return generated are based upon both an expected return and volatility. Simulations recognize age-based mortality rates, or incorporate a randomly generated age at death that is based on mortality tables that reflect sex, health, and possibly other factors.

The thousands of results from the simulations can then be categorized in various ways to determine the probability of certain outcomes, such as the expected range of the level of income or the range of bequests. Alternative planning strategies can be considered. This approach should be revisited periodically. Longevity pooling is considered if annuities or the timing of Social Security are taken into account.

Pros. This method produces thousands of potential outcomes for each planning strategy that’s analyzed. Those outcomes can be categorized to assign probability of occurrence. For example, a given strategy might show that it would satisfy the retiree’s lifetime income goal 95% of the time. Competing strategies can be analyzed to determine their relative attractiveness. The model must be kept up to date with periodic updates.

Cons. The results require the ability to interpret a percentile range or a chance of failure. The results are only as good as the assumptions. Selection of assumptions regarding expected returns, expected variances in those returns, and covariances in returns among asset classes can be complex. The required effort may discourage periodic reevaluation and readjustment.

© 2020 American Academy of Actuaries. A longer version of this white paper can be found here.

UBS Financial Services Inc., one of four “wirehouses” or full-service brokerages in the U.S., will pay more than $10 million to resolve federal charges that for four years it “improperly allocated bonds intended for retail customers to parties known in the industry as “flippers,” the Securities and Exchange Commission announced this week.

These individuals purchase new issue municipal bonds, often by posing as retail investors to gain priority in bond allocations. The defendants then “flip” the bonds to broker-dealers for a fee.

The order imposes a $1.75 million penalty, $6.74 million in disgorgement of ill-gotten gains plus over $1.5 million in prejudgment interest, and a censure. Two UBS registered representatives, William S. Costas and John J. Marvin, were fined and will incur a 12-month “limitation” from trading in negotiated new municipal securities.

The SEC previously settled charges against Jerry E. Orellana, a former UBS Executive Director, for submitting retail orders to the underwriting syndicate from certain UBS customers who were flippers.

Without admitting or denying the findings, UBS consented to a cease-and-desist order that finds it violated the disclosure, fair dealing, and supervisory provisions of Municipal Securities Rulemaking Board Rules and the Securities Exchange Act of 1934.

“UBS registered representatives knew or should have known that flippers were not eligible for retail priority,” the SEC order said, adding that “UBS registered representatives facilitated over 2,000 trades with flippers, which allowed UBS to obtain bonds for its own inventory, thereby circumventing the priority of orders set by the issuers and improperly obtaining a higher priority in the bond allocation process.”

The SEC also charged UBS registered representatives William S. Costas and John J. Marvin with negligently submitting retail orders for municipal bonds on behalf of their flipper customers. Costas was charged with helping UBS bond traders improperly obtain bonds for UBS’s own inventory through his flipper customer.

Costas and Marvin agreed to settle the charges without admitting or denying the SEC’s findings, and consented to orders finding they violated MSRB Rules G-11(k) and G-17. Costas agreed to pay disgorgement and prejudgment interest totaling $16,585 and a civil penalty of $25,000, and Marvin agreed to pay disgorgement and prejudgment interest totaling $27,966 and a civil penalty of $25,000.

The SEC’s investigation was conducted by the Division of Enforcement’s Public Finance Abuse Unit, which is led by LeeAnn G. Gaunt. The investigators included Joseph Chimienti, Laura Cunningham, Warren Greth, Cori Shepherd, and Jonathan Wilcox, with assistance from Deputy Unit Chief Mark Zehner and Assistant Director Kevin Guerrero. Ivonia K. Slade supervised the investigation.

Jackson National Life Insurance Company today announced the completion of a $500 million equity investment from Athene Holding Ltd. in return for a 9.9% voting interest corresponding to an 11.1% economic interest in Jackson.

Jackson has $297.6 billion in total IFRS assets and $269.5 billion in IFRS policy liabilities set aside to pay primarily future policyowner benefits (as of December 31, 2019).

Jackson is an indirect subsidiary of Prudential plc, an Asia-led portfolio of businesses focused on structural growth markets. Prudential plc has 20 million customers (as of December 31, 2019) and is listed on stock exchanges in London, Hong Kong, Singapore and New York.

Prudential plc is not affiliated in any manner with Prudential Financial, Inc., nor with the Prudential Assurance Company, a subsidiary of M&G plc, a company incorporated in the United Kingdom.

AM Best has removed from under review with negative implications and downgraded the Financial Strength Rating to B+ (Good) from A- (Excellent) and the Long-Term Issuer Credit Rating to “bbb-“ from “a-” of Foresters Life Insurance and Annuity Company (FLIAC) (New York, NY).

The outlook assigned to these ratings (ratings) is negative. “Although FLIAC is fundamentally sound in terms of risk-adjusted capitalization and operating earnings, the rating downgrades reflect drag from Nassau’s insurance operating entities,” AM Best said in a release.

On July 1, 2020, Nassau Financial Group, L.P. (Nassau) announced that it had completed the acquisition of FLIAC from The Independent Order of Foresters. Concurrently, AM Best withdrew the ratings following its merger into Nassau Life Insurance Company.

The ratings reflect FLIAC’s balance sheet strength, which AM Best categorizes as adequate, as well as its adequate operating performance, limited business profile and appropriate enterprise risk management.

AM Best expects the earnings impact of the acquisition for Nassau to be modest in the near term, although accretive in the longer term assuming satisfactory execution of strategic plans.

New York Life’s board has elected Craig DeSanto as its president of the company, the New York Life reported this week. DeSanto, 43, had been co-Chief Operating Officer. New York Life chairman and CEO Ted Mathas had been president since former president John Y. Kim retired in 2018. DeSanto continues to report to Mathas.

As president, DeSanto will oversee all businesses of the company, including the Individual Life Insurance and Agency Distribution units, as well as Retail Annuities, New York Life Investment Management, and the company’s portfolio of strategic businesses.

DeSanto joined New York Life in 1997 as an actuarial intern, later becoming head of the Institutional Life Insurance business, Individual Life Insurance business, and Eagle Strategies. In 2015, he was appointed to lead the company’s Strategic Businesses, where he built businesses that support the company’s core retail life insurance franchise.

In 2017, DeSanto joined the company’s Executive Management Committee, and in the two subsequent years, he assumed oversight for Retail Annuities and New York Life Investment Management, respectively.

DeSanto helped lead New York Life’s pending acquisition of Cigna’s Group Life and Disability Insurance business, which is the company’s largest acquisition to date. The transaction is expected to close in the third quarter.

© 2020 RIJ Publishing LLC. All rights reserved.

Conceding that its information systems are outdated—based on obsolete mainframe computers and decades-old software—Vanguard, the Valley Forge, PA-based $6.2 trillion financial services company, is transferring its retirement plan administration business to the Bengaluru, India-based tech giant, Infosys.

The Times of India reported the value of the recordkeeping business at $1.5 billion, with the value possibly rising to $2 billion over a 10-year period. Infosys beat Wipro Technologies for the contract, which was also pursued by Accenture and TCS, the news service said this week.

Infosys, founded in 1981 and listed on the New York Stock Exchange, has revenues of $12.7 billion, 239,000 employees, almost 1,500 IT customers in 46 countries. Its CEO since early 2018 has been Salil Parekh, an aeronautical engineering graduate of the Indian Institute of Technology with masters degrees in mechanical engineering and computer science from Cornell University.

According to the Vanguard website, “Infosys currently serves half of the top 20 retirement service firms in the U.S., helping clients to manage risk, improve participant experience, and deliver better retirement plan outcomes through business transformation, technology services, and digital solutions.

“The firm offers end-to-end, enterprise-wide insurance and retirement business-process solutions across five core businesses: life insurance and annuity services, producer services, retirement services, employer sponsored services, and functional BPO services.”

“Industry consolidation in recordkeeping has been a long-term trend,” said Tim Rouse, president of SPARK, the recordkeepers’ trade association, in an interview with RIJ. “If you look back ten years, the number of companies that still do their own recordkeeping is much lower. For example, Wells Fargo sold its recordkeeping business to Principal last year. The driver ultimately is cost savings.”

Infosys stock has risen from about $7 on March 13 to $12.55 on Tuesday. There’s been little or no mention of the potential for a culture clash or even financial clash between Vanguard, which operates like a cooperative and has never disclosed the precise financial relationship between its funds and its back-office operation, and a publicly held partner.

Comments by Vanguard Institutional Investor Group chief Martha King suggested that Vanguard would rather focus on its virtual advice capabilities and reduce the costs of recordkeeping, a low-margin business.

“Coupled with Vanguard’s increasing investment in advice capabilities and client experience, we will set a new bar for personalization, ease, and efficiency for sponsors and participants alike,” King said in a release.

Of Vanguard’s $6.2 billion of assets under management (AUM), $1.3 trillion is in its defined contribution business. It is the largest manager of defined contribution assets in the world, and a leading issuer of target-date funds and exchange-traded funds.

Over the past decade, as investors have flocked to low-cost index funds, a Vanguard specialty, the firm’s AUM has grown dramatically—with asset flows in some years surpassing the flows of the next nine largest asset managers in the U.S., according to Morningstar.

Approximately 1,300 Vanguard roles currently supporting the full-service recordkeeping client administration, operations, and technology functions will transition to Infosys. All Vanguard employees currently performing these roles will be offered comparable positions at Infosys in close proximity to Vanguard’s offices in Malvern, PA, Charlotte, NC, and Scottsdale, AZ.

Infosys will start this project with 300-400 employees in India and eventually increase to 3,000-4000 employees; Infosys has a plan to set up the facility in Electronics City in Bengaluru to service this deal.

© 2020 RIJ Publishing LLC. All rights reserved.

Imagine that you’re a 65-year-old participant in a 401(k) plan, preparing to retire. You’ve got $500,000 invested in a 2020 collective investment trust (CIT), which is similar to a 2020 target date fund. The manager of the CIT offers you this prepackaged retirement income strategy:

You’ll split your $500,000 into two parts. You’ll leave $425,000 in the 401(k) plan, and spend about $22,500 of it per year. With the other $75,000, you’ll buy a deferred income annuity that will start paying you about $18,000 a year if and when you reach age 85.

Meet the Wells Fargo Retirement Income Solution, which the brand-bruised, $2 trillion bank and asset management firm launched this spring. The firm is eager to grow its $12 billion target-date CIT business, and it believes that an income option will add cachet as well as new functionality.

“We did survey work at the participant and sponsor levels, and we heard a lot about the need for ‘liquidity’ and ‘flexibility,’” Nate Miles, head of retirement at Wells Fargo Asset Management, told RIJ in an interview. Participants need liquidity; and plan sponsors need the flexibility to change annuity providers if for any reason they need or decide to.

Many investment companies have tried, are trying, and will try to retrofit the tail end of a 401(k) plan to produce lifetime income for participants. They have to, or they risk losing access to trillions in tax-deferred money as baby-boomers age out of the “accumulation” stage and into the retirement spending (or “decumulation”) stage.

DCIO (Defined Contribution Investment Only) specialists like Wells Fargo are arguably not positioned as well as full-service retirement plan providers to control their own destinies. On the other hand, they offer “unbundled” a la carte solutions that some plan sponsors are said to prefer.

Nate Miles

With luck, elements of the 2018 SECURE Act will make plan sponsors more receptive to incorporating income solutions into plans. But the process is complicated—for many reasons. And, except in isolated areas, such as the academic market, neither plan participants nor plan sponsors are clamoring for this service.

Wells Fargo isn’t the mostly likely pioneer in the decumulation business. The company is still recovering from a multi-year “cross-selling” scandal that cost billions of dollars in refunds, fines and settlements, as well as a chunk of the firm’s reputation. As of 2019, it has a new president and CEO, Charles Scharf. Last year, Wells Fargo Bank sold its retirement plan business to Principal Financial for $1.2 billion. Now, boldly, it’s tackling the age-old “annuity puzzle.”

Wells Fargo Retirement Income Solution has its own particular nuances, but the company is not developing it entirely from scratch. For the two years ending in August 2016, Miles was head of U.S. Defined Contribution Investment Strategy at State Street Global Advisors (SSgA), where he worked on a similar target-date/deferred income annuity program.

As noted above, the actual design of the Wells Fargo Retirement Income Solution is pretty simple. (In fact, it resembles a strategy published by Jason S. Scott at Financial Engines over a decade ago.) Plan participants would be defaulted into an age-appropriate Wells Fargo target date CITs. As they approach retirement, they would learn about a packaged solution for their future income needs, combining a systematic withdrawal plan with an annuity.

A small portion (15%) of their CIT balance would be applied to the purchase of a QLAC or qualified longevity annuity contract. These are fixed deferred income annuities for qualified money, whose monthly payouts can be postponed until age 85. QLACs were created by the U.S. Treasury Department in 2014 to help retirees delay their annuity payments without running afoul of the requirement for minimum distributions (RMDs) from retirement accounts starting at age 72.

The remaining 85% of the retiree’s plan assets would remain in the Wells Fargo CIT. Wells Fargo would distribute it at the non-guaranteed rate of 5% a year. “We envision fees of 18 to 21 basis points on the money that stays in the plan,” Miles said. The recordkeeper will add an as-yet undetermined charge for running the systematic withdrawal plan. The cost of the annuity will be built into its payout rate.

Wells Fargo hopes to use the participants’ own inertia to carry them into the solution. People who have been invested for years in target date funds are characteristically passive. Wells Fargo is betting that when they reach age 65 and Wells Fargo offers them a packaged solution to their retirement income dilemma, a significant number of them will accept it.

“Our guess is that the auto-enrolled, auto-escalated participants are not engaged enough in the process to feel confident about choosing among many different retirement income options and strategies. We went back and forth on how much choice to offer,” Miles told RIJ. “We think that offering less choice, not more, is right for participants [who have consistently been passive investors].”

“From a marketing perspective, we would hope that our participants would be aware of the program from the beginning,” he said. “We would increase communications starting at age 60, and then have multiple points of communication as they approach age 65. We aren’t licensed to sell insurance, so the participants ages 65-plus would work with a representative of the insurance carrier [that issues the annuity].”

Wells Fargo Retirement Income Solutions is just getting started. It hasn’t formally engaged any life insurers who sell QLACs. Retail sales of all deferred income annuities in 2019, including QLACs, were $2.5 billion, or about one percent of total annuity sales. The “opt-in” aspect of the Wells Fargo plan also presents a potential pricing problem for annuity issuers.

Since participants aren’t defaulted into the annuity purchase, there’s a risk of “adverse selection.” That’s the risk, prevalent in the retail annuity space, that only the healthiest people—with above-average life expectancies—will opt-in. Insurers have to raise prices to compensate for that effect, which lowers the annuity payout rate and makes it less attractive.

In pitching the solution to plan sponsors, Wells Fargo stands to benefit from a provision in the 2018 SECURE Act that reduced the risk that plan sponsors might be sued for choosing an annuity provider that fails someday. “While assets leave the plan when annuity purchases occur, the money is still inside the plan when we’re asking the participant to choose the solution. So the plan sponsor could still benefit from the protections of the SECURE Act,” he said.

Miles also assures liability-conscious plan sponsors that Wells Fargo has a process for vetting and contracting life insurers. His firm will be acting as a fiduciary—a so-called “3(38)” fiduciary—in choosing the life insurer. “We’ll be taking responsibility for the selection of the insurance carrier,” he said. The selection process will be done by Wells Fargo’s Insurance Credit Analysis Group, which also evaluates annuity providers with products for sale via Wells Fargo Advisors’ 13,500 financial advisors.

Given his experience at SSgA, Miles appears to have few illusions about the difficulty of what he’s trying to accomplish—convincing multiple parties with dissimilar financial needs and imperatives to swim in the same direction.

“There are three or four sales here,” he told RIJ. “There’s the participant, the plan sponsor, the insurance carrier, and the recordkeeping platform. Each one of them requires time and thoughtful product development.”

© 2020 RIJ Publishing LLC. All rights reserved.

When private equity (PE) firms like Guggenheim, Apollo, and Goldman Sachs bought struggling life/annuity businesses at bargain prices after the 2008 financial crisis, they strode into the insurance industry with a certain Wall Street swagger.

As the PE firms grabbed blocks of in-force annuities, they radiated a self-assurance that their big-city risk-wrangling skills would enable them to squeeze more yield out of general account assets than long-established life insurers ever did.

But how would they do it, exactly? Were they smarter? Did they have more chutzpah? The evidence suggests that at least one way they outperformed was by exploiting a regulatory measure, created on an emergency basis to prevent fire sales during the 2008-2009 crisis but never withdrawn, which reduced the capital requirement for one particular class of troubled securities.

In a research paper published early this month, Natasha Sarin, who teaches financial regulation at the Wharton School, and Divya Kirti of the International Monetary Fund, present the results of examining the asset purchases by new PE-led insurance companies during the period from 2009 to 2014.

In their paper, “What Private Equity Does Differently: Evidence from Life Insurance,” Sarin and Kirti show that after PE firms acquired insurance companies, they loaded up on “non-agency residential mortgage-backed securities”, or RMBS—knowing that their capital requirements had been lowered. [“Non-agency” means not issued by Fannie Mae or Freddie Mac and not guaranteed by the U.S. government.]

In November 2009, regulators at the National Association of Insurance Commissioners (NAIC) decided to help insurers who were holding lots of suddenly downgraded non-agency RMBS. They allowed the insurers to hold the RMBS on their books at a reduced value reflecting the expected loss (as estimated by PIMCO and BlackRock for the NAIC) but not at an increased risk of loss.

This regulatory change, Sarin and Kirti say, prevented beleaguered life insurers from dumping their RMBS on the market in droves, or facing the prospect of having to raise capital to support the risky assets. At the time, there were some 18,000 RMBS outstanding, all difficult to put a value on.

A PE firm, once it had acquired a life insurer (between 2009 and 2014), immediately seized on this arbitrage opportunity by investing heavily in RMBS—acquiring large amounts of them at depressed prices but without elevated capital requirements.

Natasha Sarin

The NAIC capital requirements for insurance company assets range from very low for top-rated bonds to very high for lower-rated bonds, Sarin told RIJ. The highest rating is NAIC-1. But things changed during the Great Recession when the NAIC decided to give the insurance industry some relief.

“NAIC-1 used to be just AAA-rated bonds, but that’s not true any more,” she said. “[After the rule change], if you have $100 of mortgage-backed securities with a five percent risk of default, you can hold it at a value of $95 and have the same capital requirement as a $95 AAA bond with no chance of default. You’re conflating an expected loss with guaranteed loss, and it can’t possibly be true that both should have the same capital requirements, because the underlying risks are different.”

Sarin and Kirti reached their conclusions after comparing the investment activity of PE-owned and non-PE-owned insurers. “For many PE-owned insurers in our sample, we observe that immediately after a PE firm takes over, the insurer shifts—within just a few days—to take advantage of the NAIC treatment of non-agency mortgage-backed securities,” she said. None of the PE-led life insurers are named in the paper.

Using the regulatory change—which still exists after more than 11 years, but still only for non-agency residential and commercial mortgage-backed securities—made a significant difference in capital requirements.

“On average,” the authors wrote, “PE-owned insurers’ capital charges across all bond holdings are 20% lower than they would have been absent the crisis-era regulatory change. For subsidiaries of two of the largest PE groups in our sample, capital charges are only half the level that would have been previously required.”

The research also showed that the ability to spot an arbitrage opportunity and act quickly was the main difference between PE-led and non-PE life insurers. “Beyond this capital arbitrage, we find no evidence that PE firms display any specialized investment skill in portfolio allocation, nor is there evidence that they deliver operational improvements,” the paper said.

The authors make the bold assertion that PE-led insurers may be over-rated by ratings agencies. “Were capital charges still assigned based on underlying bond risk, government intervention to address capital deficiencies could have been triggered for a quarter of PE-backed insurers,” they wrote.

“This risk appears to be missed by rating agencies: Many PE-backed insurers are rated A- to B++; ratings that fully accounted for their junk bond holdings would be several notches lower and among the lowest in the industry.”

“This is a concern for us, and we’re monitoring it closely,” an NAIC spokesperson told RIJ this week. “The original idea was that you don’t want to see a fire sale. So we said, if you write your security down to 50 cents on the dollar, the capital charge will be applied to the book value, not to the par value or purchase price. We’re concerned, but the situation is not as dire as they paint it in the paper.”

Today, the 2009 regulatory change for non-agency RMBS and CMBS (commercial mortgage-backed securities) is still on the books. The ruling doesn’t affect other asset-backed securities that PE-owned life insurers have been investing in, such as collateralized loan obligations or CLOs. These are bundles of auto loans or other consumer loans. Life insurers typically buy the higher-rated tranches.

The NAIC recently completed a study of CLO ownership by U.S. life insurers. RIJ will be reporting further on the private-equity-led life insurers and CLOs in the weeks ahead.

© 2020 RIJ Publishing LLC. All rights reserved.

People of color, women, younger generations and small business owners have been disproportionately affected financially by the COVID-19 pandemic so, according to Prudential’s 2020 Financial Wellness Census. More than half of Americans reported damage to their financial health.

Nearly one-in-five respondents said their household income was cut by half or more in the months following the pandemic’s outbreak, with 17% losing employer contributions to a retirement plan, 14% losing health insurance and 10% losing group life insurance benefits, eliminating critical safety nets, according to the census, which was conducted in May 2020.

One-third (34%) of those with household incomes under $30,000 reported being unemployed, only 8% of those with household income over $100,000 reported being unemployed. The overall unemployment rate was 17%.

Gig workers, LGBTQ Americans and those employed in the retail industry were more likely than average to say that their household income was cut in half or more.

A Prudential survey in December 2019 showing Americans were financially on the upswing. More than half (52%) ranked themselves financially healthy by objective measures, up from 46% in Prudential’s first Financial Wellness Census conducted in October 2017.

Regardless of household income, the survey revealed nearly half of Americans (48%) are worried about their financial future, up from 38% just a few months earlier.

Census respondents said they would like to see more affordable health care, more flexible work options and more government support for small businesses. Those with lower incomes want affordable health care and universal health care coverage, better government support of small businesses and the unemployed, a higher minimum wage and more protections for workers.

Americans most often look to the federal government for financial assistance in times of crisis (32%), the data showed, followed by family and friends (28%), then state and local governments (27% and 17%, respectively).

The workplace benefits Americans most value include retirement savings plans, paid time off, and comprehensive health care and prescription drug coverage, according to the census.

The financial strength and credit ratings of Global Atlantic Group remain unchanged after KKR & Co. (KKR) announced its intention to acquire a controlling interest in these companies, according to AM Best, the credit rating agency.