Top 20 Fixed Indexed Annuity Issuers

IssueM Articles

Consider the challenge that faces advisors who want to do good for humankind and do well for themselves by specializing in the intriguing new niche called retirement income planning.

If those advisors want to serve near-retirees with $500,000 to $1 million in savings, they need a semi-scalable planning tool and they need financial contracts that sensible clients will sign at the end of a two-hour meeting (ideally).

That’s not enough time to create a thorough plan, frankly. But efficiency is important for advisors serving clients with complex planning needs but not a ton of money. Efficiency offsets the cost of drilling a lot of dry holes as well as the relative slimness of this demographic’s values.

This problem will mainly affect independent advisors who make their own decisions but who are still learning to be ambidextrous: able to solve tough income cases quickly with combinations of mutual funds, annuities and perhaps life insurance or long-term care reverse mortgages.

To win at the income game, arguably, you’re going to need, along with the right licenses, a robust piece of retirement income planning software. You’re probably also going to need to sell, or bring into your repertoire of products, fixed indexed annuities (FIAs) with guaranteed lifetime withdrawal benefits.

Stating the obvious

Excuse me for stating the obvious: FIAs are designed to sell. Their designers have systematically stripped them of objectionable qualities. They offer (within bounds) liquidity, downside protection, upside potential, and a choice of indexing and crediting options. Especially important for income specialists: Some of their riders now produce more lifetime income after a 10-year waiting period than deferred income annuities.

FIAs have survived years of controversy regarding aggressive sales practices, two attempts to regulate them at the federal level (by the SEC in 2007 and by the Obama Department of Labor in 2016) and a lot of bad press. They are now an acceptable product for old-school domestic life insurers (like Nationwide, AIG and Lincoln Financial) to manufacture and for many fee-based Certified Financial Planners (CFPs) to sell without blushing. No-commission versions are available to registered investment advisors (RIAs).

So the idea of selling an FIA after one or two meetings, to clients whom the advisor may have known for only a short time, becomes feasible—much more feasible than the sale of an irrevocable income annuity or even a variable annuity with an income rider.

Excuse me for stating another truism: Retirement income planning is more complex than investment planning, and retirement income planning software is still evolving. But a number of online tools for income planners have now emerged. And we’re not talking about robo-advice platforms.

A decade or more ago, there were pioneers like Income for Life Model (IFLM) and Advisor Software (ASI). Then came adapted versions of investment tools like eMoney and MoneyGuidePro. Mass-market and boutique tools have included Income Discovery, Financial Preserve, Savings2Income, RetireUpPro, JourneyGuide, IncomeConductor, and one created by Nobel laureate Bill Sharpe.

The most advanced of these tools allow advisors to input new assumptions or preferences or “what-ifs” and generate different versions of plans on the fly, thereby eliminating the deadening turn-around time once required to make changes to a plan. The marketers of some of these new tools claim to make even a one-hour income plan possible.

Good better than perfect?

That may not be how you or I would want to be served. But many advisors are undoubtedly arriving at the discipline of retirement income planning from a sales-oriented past, and they won’t be looking for perfect solutions. They want a great razor (the planning tool) that will help them sell blades (annuities, in addition to mutual funds, long-term care insurance, and perhaps even reverse mortgages).

At best, the financial advice industry is still in a transitional period from the accumulation mindset to ambidextrous thinking that leads to highly customized income plans. I wish it were farther along, but it’s not. For now, many intermediaries will want and need processes and products that suit their old habits and comfort zones.

© 2018 RIJ Publishing LLC. All rights reserved.

Independent broker-dealers (IBDs) have grown at a compound annual rate (CAGR) of 11% over the past five years, compared with 9% at retail bank B/Ds, 9% at regional B/Ds, and only 6% at the four wirehouse brokerages, according to a new report from Cerulli Associates.

IBDs have the second-largest advisor force at more than 59,000 and assets of $2.8 trillion, Cerulli said. When hybrid registered investment advisors (RIAs) and their assets are included in the total, those numbers reach 86,779 and more than $3.36 trillion.

Cerulli divides IBDs into four sub-segments:

“The Niche (14%) and Institutional (11%) IBD segments have buoyed channel growth over the past five years. Institutional IBDs are the largest,” a Cerulli release said. “There are only 24 in total. They control 49% of the channel’s advisor force and 59% of the assets. The segment continues to benefit from national scale, brand reputation, and increasing advisor-counts through recruiting efforts and acquisitions.

There are only 14 Niche IBDs, which are dramatically smaller and control just 11% of the channel’s advisors and 14% of assets. They focus on specific niches or products (e.g., retirement plans). Their advisors are the most productive in the channel.

The wirehouse picture is complex. “Naturally, being the largest channel in terms of wealth management assets, the four wirehouses have the most to lose in terms of market share and advisors,” Donnie Ethier, Director of Wealth Management and Consulting at Cerulli, told RIJ in an email. “Cerulli would not simply attribute their lagging the industry’s overall retail growth rate due to their size, however. There are many other factors at play.

“First, is advisor migration. Decisions by advisors, and entire teams, to relocate to other channels, including independent RIAs, has influenced these trends. Independent RIAs have expanded their advisor headcounts by about 5% over the past five and 10 years, while AUM has grown at 13% and 10% over the past five and 10 years, respectively. Hybrid RIAs have expanded at lesser, but comparable, rates.

“As noted, a portion the RIA growth is due to experienced wirehouse advisors relocating. In 2018, almost one-third of current wirehouse advisors that are considering/interested in relocating to other channels told Cerulli that they would prefer either the independent or hybrid RIA channels. Thirteen percent indicated IBDs.

“That said, there is another important element. Yes, the wirehouses’ growth rates have lagged other B/D channels’ over the past one and five years. However, this is for ‘retail’ assets. What can be overlooked is that the opposite is true in the high net worth (HNW) space. The wirehouses’ HNW growth rates have exceeded the industry average (HNW-specific) over the past 1, 5, and 10 years. Ultimately, their strategic decisions to focus on more affluent clients is paying off. This story is not necessarily observable when looking at overall asset trends.”

The growth of the IBD channel appeals to asset managers seeking broader distribution opportunities. According to Cerulli, “IBDs remain one of asset managers’ most consistent opportunities due to the large number of potential firm partnerships, advisors, and accelerating growth from the hybrid channel.”

To maintain growth, the channel will need to evaluate succession-planning models, improve advisor productivity, and protect against large teams migrating to the independent RIA model, the release said.

Cerulli’s latest report, U.S. Broker/Dealer Marketplace 2018: Escalating Margin Pressure, provides in-depth market sizing and competitive analysis of B/D channels, including wirehouses, national and regional B/Ds, IBDs, insurance B/Ds, and retail bank B/Ds. This report extensively covers recruiting and transition trends, including advisor movement sizing, advisor channel preferences, advisor retention, and transition metrics.

© 2018 RIJ Publishing LLC. All rights reserved.

Envestnet, the open-architecture, cloud-based turnkey asset management platform (TAMP), and BlackRock, the giant asset manager, are partnering to integrate BlacRock’s Digital Wealth technologies into Envestnet’s platform for registered investment advisors and other wealth managers.

The partnership calls for BlackRock, Inc., to acquire a 4.9% equity stake in Envestnet by purchasing about 2.36 million shares of Envestnet common stock for $52.13 per share. The aggregate purchase price is about $122.8 million.

Envestnet will also give BlackRock a warrant to purchase about 470,000 shares of Envestnet common stock at an exercise price of $65.16 per share, subject to customary anti-dilution adjustments. BlackRock can exercise the option for four years from the date of issue.

The Company expects the investment to close by the end of 2018, subject to clearance under the Hart-Scott Rodino Antitrust Improvements Act and other customary closing conditions.

Envestnet’s financial advisor for the deal is PJT Partners LP. Mayer Brown LLP is its legal counsel. BlackRock’s legal counsel is Skadden, Arps, Slate, Meagher & Flom LLP.

© 2018 RIJ Publishing LLC. All rights reserved.

Milliman, Inc., has introduced a new security feature on Millimanbenefits.com, which hosts account information for participants in Milliman client retirement plans. The Account Lock feature allows participants to “lock down” their accounts and prevent the initiation of any distributions or loans. It gives participants an added layer of defense against external security threats.

“It’s an intuitive and effective security innovation that we expect to see imitated by other plan administrators,” said Laura Van Domelen, a Milliman principal and Defined Contribution Client Relations Leader.

Renee Schaaf, senior vice president and chief operating officer of Principal International, will become the new president of Retirement and Income Solutions (RIS) effective March 1, 2019. The current president of RIS and chairman of Principal Funds, Nora Everett, will retire at the end of March 2019 after four years in that position.

From 2000 to 2008, Schaaf held RIS leadership positions in marketing, strategy, and Principal’s midsized retirement plan businesses. Before moving to Principal International to lead strategic planning and business development, she served as vice president of national accounts in the health division.

Her successor in Principal International will be announced in early 2019.

Everett joined Principal in 1991 as an attorney. She held senior leadership roles within the law department before becoming president of Principal Funds in 2008, and then CEO of Principal Funds in 2010.

Wells Fargo Institutional Retirement and Trust has launched a Retirement Income Planning Center, an online resource for participants over age 50 in plans that Wells Fargo Institutional Retirement and Trust administers.

The Center provides do-it-yourself resources to help participants create retirement budgets and income plans. It also features videos of retiree experiences and tools to help visitors envision what retirement might look like.

Wells Fargo Institutional Retirement and Trust has also developed Retirement Income Conversations. Participants in a Wells Fargo Institutional Retirement and Trust-administered retirement plan can call a dedicated toll-free number and talk with a trained representative about retirement income. Onsite presenters also hold meetings in person at the work sites of those companies.

Northwestern Mutual have announced two new senior leadership appointments:

Christian Mitchell has been appointed to executive vice president and chief customer officer, assuming responsibility for Northwestern Mutual’s client and planning experience.

Mitchell will maintain his role as president of the Northwestern Mutual Wealth Management Company and will retain leadership of Investment Products and Services. Mitchell received his B.A. from Indiana University and his M.B.A from Yale.

John Roberts has been appointed to executive officer and vice president of distribution performance, working with the company’s financial advisors and leaders. Roberts is responsible for driving sales and developing new advisors. Roberts received his M.B.A. from Northwestern University’s Kellogg School of Management and B.S. in Finance from Indiana University.

The 1851 novel Moby Dick by Herman Melville is easier to read than most of the content on even the best-performing banking websites, and this difficulty hurts trust in those financial firms. So says a newly published review of US banking communications by VisibleThread, a consulting firm.

“The financial services industry is one of the least trusted according to the Edelman Trust Barometer 2018. When asked what most damages trust, the number one response was unclear terms and conditions,” said Fergal McGovern, CEO of VisibleThread, in a release.

Key findings of the VisibleThread report include:

These factors make bank content complex and inaccessible. “Several banks could improve their rankings by making simple changes. Eliminate passive voice, reduce sentence length and choose less complex words,” according to VisibleThread.

© 2018 RIJ Publishing LLC. All rights reserved.

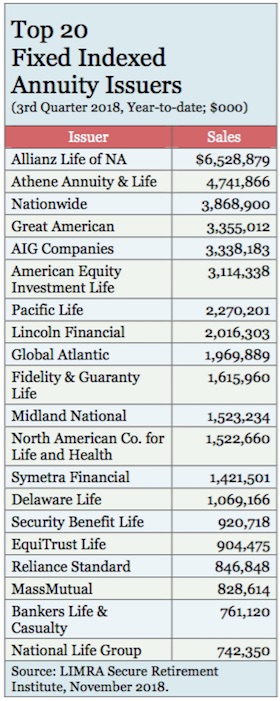

Indexed annuities used to be a joke in the loftier precincts of the life insurance industry, but not any more. Once scorned by big insurers in favor of variable annuities (VAs) ignored by academics in favor of income annuities, and assaulted by state and federal regulators, they’ve emerged from a turbulent decade with the last laugh.

“I am not surprised to see yet another record-setting quarter for indexed annuities,” said a press release from Sheryl J. Moore, president and CEO two annuity data tracking firms and a tireless advocate for fixed indexed annuities (FIAs). “I want to prepare everyone, and just say that you can count on another go-round for fourth quarter, 2018; we are going to make it a three-peat!”

The Trump victory in 2016 helped. No longer in danger of violating the Obama administration’s tough fiduciary standard of conduct, advisors, reps and agents can safely go back to selling them on a buyer-beware basis. The sales figures reflect a return to the old regulatory normal.

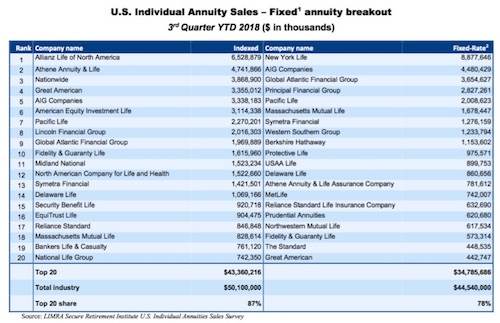

In the third quarter of 2018, FIA sales were $18.0 billion, up 38% from third quarter 2017, according to the LIMRA Secure Retirement Institute (LIMRA SRI) Third Quarter 2018 Sales Survey (representing 95% of the market). Year-to-date, FIA sales were $50.1 billion, 22% higher than the first three quarters of 2017.

Rising interest rates have not hurt. “Over the past year, the 10-year Treasury rate has increased nearly 60 basis points and ended the third quarter above the 3% mark,” said Todd Giesing, annuity research director, LIMRA SRI.

Manufacturers and distributors can both find something to like about FIAs. These bond-based products offer a more stable chassis (relative to variable annuities) on which life insurers can build the living benefit riders that offer Boomers a flexible source of guaranteed income.

“FIA products with guaranteed lifetime benefit riders showed the most growth [among annuities] in the third quarter,” said Giesing. “In a higher-interest rate environment, companies are able to increase their guaranteed lifetime withdrawal rates.” VAs are also more capital intensive than FIAs, and bull markets can hurt as well as help them. Ohio National’s recent decision to leave the annuity business after selling too much of a rich VA product is a recent example of that.

Insurance agents once sold virtually all FIAs; now fee-based advisors and even registered investment advisors (RIAs) can sell them. FIAs’ combination of attributes—a guarantee against downside loss, high commissions for agents and brokers, better lifetime income than deferred income annuities, and a bit of exposure to the equity markets—add up to a viable sales proposition. Unlike VAs, a securities license isn’t required to sell them.

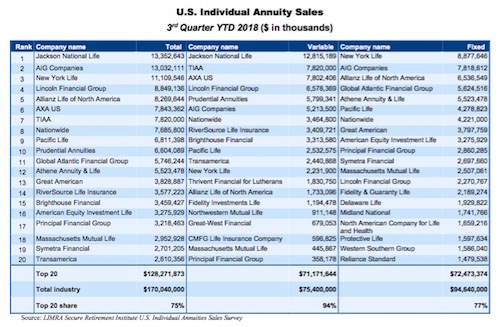

VAs still outsold FIAs through the third quarter of 2018, by $75.4 billion to $50.1 billion. VAs will likely continue to benefit from their status as the best way for high net worth investors to accumulate and trade equities on a tax-deferred basis. If you combine FIAs with other fixed deferred annuities, fixed annuities outsold VAs in the first nine months of this year by $94.6 billion to $75.4 billion.

LIMRA SRI expects total fixed annuity sales to hit record levels in 2018, with fixed annuities expected to end this year at around $130 billion, the fourth consecutive year exceeding $100 billion. This has never occurred in the more than 40 years LIMRA SRI has tracked annuity sales, LIMRA said. LIMRA SRI forecasts total 2018 FIA sales to reach about $70 billion. Slower growth is expected in 2019 and 2020.

The manufacturers

With their growing respectability—although some broker-dealers still haven’t embraced them—FIAs have found more life insurers wanting to offer them. Allianz Life of North America still rules the FIA world (as it has since buying Bob MacDonald’s Life USA in 1999 for $540 million) with a 13% market share (15.4%, according to Moore’s LooktoWink.com, which uses a slightly different survey base). Allianz Life’s Allianz 222 Annuity was the top-selling indexed annuity, for all channels combined, for the seventeenth consecutive quarter, according to LooktoWink.com.

But many new players have piled in, shuffling the sales leaderboard. The top 10 sellers of FIAs now include three FIA veterans (Allianz Life, Great American, and American Equity Investment Life), three offsprings of equity-backed firms (Athene, Global Atlantic and Fidelity Guaranty & Life) and four big insurers that have embraced FIAs in recent years (AIG, Nationwide, Pacific Life, and Lincoln Financial).

Rising competition from new entrants has been tough on American Equity Investment Life. Over the past three years, its third-quarter year-to-date sales have dropped from $4.75 billion in 2015 to $3.11 billion in 2018.

“There has not been any change in our ratings or reorganization since that time but the competitive environment has changed quite a bit over the last three years. The LIMRA reports for the 2015–2018 periods should show substantial increases in fixed index annuity sales for Athene, Nationwide and AIG Companies,” Giesing said.

Jackson National continues to sell the most VAs, with its Perspective II contract a perennial sales leader. But even Jackson is selling fewer VAs than it used to. Jackson National sold $12.8 billion worth of VAs in the first nine months of 2018, down about 30% from $17.8 billion for the same period three years ago.

VA sales were $75.4 billion in the first nine months of 2018, up 4% compared with the same period in 2017. Variable annuity sales increased 25% in the third quarter to $25.0 billion, compared with prior year results, but LIMRA SRI expects VA sales to increase less than 5% in 2018. That would, however, represent the first annual growth for VA sales in six years. VA sales are expected to slightly dip in 2019 in anticipation of equity market declines, according to LIMRA.

While fee-based VAs increased 43% over prior year to $800 million, this is down 6%, compared with second quarter results. “There continues to be operational hurdles in the fee-based VA market, which challenge adoption of these products by certain distribution channels. We expect companies will work to resolve these in the next few years,” Giesing said.

The VA product with the most sizzle is a hybrid of an indexed annuity and a variable annuity: the so-called registered index-linked annuity or RILA. “One of the factors driving VA sales growth is the increase in RILA sales, which were nearly $3 billion in the third quarter,” said Giesing.

“With more companies signaling their intention to enter the market, LIMRA SRI expects this market to top $10 billion by the end of 2018. Greater volatility in equity markets and better pricing due to rising interest rates are attracting consumers looking for a blend of growth and downside protection.”

Third quarter RILA sales grew 27% to $2.98 billion, representing 12% of the VA market. Year-to-date, RILA were $7.68 billion, 13% higher compared with prior year.

Total annuity sales were $58.8 billion, 25% above the third quarter 2017 results. For the first three quarters of 2018, total annuity sales were $170 billion, 11% higher than prior year. LIMRA SRI expects 2018 individual annuity sales to surpass $230 billion.

Fixed annuities

Fixed annuity sales drove most of this quarter’s growth. Fixed annuity sales have outperformed variable annuity (VA) sales in nine of the last 11 quarters. Total fixed annuity sales were $33.8 billion in the third quarter, a 39% increase compared with third quarter 2017 results. Year-to-date, total fixed annuity sales were $94.6 billion, up 18% from prior year.

Fixed-rate deferred (FRD) annuity sales jumped 51% in the third quarter to $11.2 billion. Year-to-date, FRD sales were $31.3 billion, 17% higher than prior year.

LIMRA SRI expects FRD sales growth to continue into the fourth quarter. Many FRD contracts are out of their surrender charge period, which could find more attractive rates in the rising interest rate environment. LIMRA SRI expects 2018 FRD sales to grow as much as 20% and as much as 25% in 2019.

Fixed immediate annuity sales were up 20% in the third quarter to $2.4 billion. Year-to-date, fixed immediate annuity sales were $7.0 billion, 13% higher than prior year. Deferred income annuity (DIA) sales rose 6% in the quarter, to $550 million. Year-to-date, DIA sales were $1.64 billion, down 2% from the same period in 2017. LIMRA SRI expects income annuity growth of 5-10% in 2018 and as much as 5% in 2019.

© 2018 RIJ Publishing LLC. All rights reserved.

Ruark Consulting, LLC today released the results of its fall 2018 studies of variable annuity (VA) policyholder behavior. The studies, which examine the factors driving surrender behavior, income/withdrawals, and annuitization, were based on experience from 13.3 million policyholders.

Twenty-four variable annuity writers participated in the study, comprising $840 billion in account value as of June, 2018. The study spanned the period from January 2008 through June 2018.

“In this study, we see new evidence of policyholder behavior changing over the course of a contract’s lifetime in ways that were not previously evident,” said Timothy Paris, Ruark’s CEO. “These include contract duration beyond the end of the surrender charge period, sensitivity of income/withdrawal commencement to moneyness levels, effects of systematic withdrawals on persistency, and guaranteed minimum income benefit (GMIB) annuitization decisions; all important factors for VA writers in pricing and managing risks for these products.”

Study highlights include:

Detailed study results, including company-level analytics, benchmarking, and customized behavioral assumption models calibrated to the study data, are available for purchase by participating companies.

Ruark Consulting, LLC (www.ruark.co), based in Simsbury, CT, is an actuarial consulting firm specializing in principles-based insurance data analytics and risk management.

Ruark’s behavioral analytics engagements range from discrete consulting projects to full-service outsourcing relationships. As a reinsurance broker, Ruark has placed and administers dozens of bespoke treaties totaling over $1.5 billion of reinsurance premium and $30 billion of account value, and also offers reinsurance audit and administration services.

Ruark’s consultants often speak at industry events on the topics of longevity, policyholder behavior, product guarantees, and reinsurance. Ruark Consulting collaborates with the Goldenson Center for Actuarial Research at the University of Connecticut.

© 2018 RIJ Publishing LLC. All rights reserved.

Jackson National Life has agreed to reinsure 100% of the Group Payout Annuity business of John Hancock Life and its affiliate, John Hancock Life Insurance Company of New York, Jackson announced in a recent release.

The portfolio of over 230,000 policies relates mainly to pension participants that are primarily in the payout phase, the majority of the policies having been issued between 1980 and 2012.

The transaction closed October 31 on the non-New York portion of the business, representing approximately 90% of the overall block of Group Payout Annuities. The closing on the New York portion is subject to New York regulatory approval and is expected to occur in early 2019.

In total, the transaction involves Jackson indemnity reinsuring approximately $5.5 billion of statutory reserves, representing an increase in Jackson’s general account liabilities of approximately 10%. John Hancock will continue to administer the business.

The acquisition is structured as 100% reinsurance of a closed block of group annuities issued by John Hancock Life Insurance Company (U.S.A.) and its New York affiliate. The transaction is expected to have minimal impact on Jackson’s U.S. statutory Risk Based Capital position.

© 2018 RIJ Publishing LLC. All rights reserved.

Charles Schwab has published a new report, “The Rise of Robo: Americans’ Perspectives and Predictions on the use of Digital Advice,” that examines people’s outlook on robo advice, its potential impact on how they invest, and its impact on the financial services industry overall.

According to the report, the expectation that robo advice will play a significant role in shaping the investing landscape spans generations from Millennials to baby boomers. At the same time, most investors also acknowledge the critical role human advisors will play into the future.

Key findings in the report include:

© 2018 RIJ Publishing LLC. All rights reserved.

UBS Equity Plan Advisory Services (EPAS) has released a financial wellness digital content offering to participants in the retirement plans it serves. The move follows an announcement earlier this year of “a re-imagined and education-focused digital user experience” for more than 800,000 plan participants.

The new content experience delivers videos, infographics, articles and “gamified” content to teach employees about planning, budgeting, saving, managing debt, investing, and retirement.

The offering is based on research on participants’ needs and wants, gathered from UBS’s corporate clients. This included researching HR related topics, such as employee retention, motivation and length of service.

EPAS will collaborate with Napkin Finance, Aon Equity Services and Imprint, to educate participants about equity compensation and their money, said Michael Barry, head of UBS Equity Plan Advisory Services at UBS Financial Services Inc., in a release.

The debut of the digital content is part of a broader financial wellness rollout to UBS’s more than 10,000 corporate clients, clients and prospective clients. The full offering will provide financial assistance from licensed UBS Financial Advisors, including a wellness assessment, seminars and webinars.

Other UBS partners include SigFig, to develop a digital advice platform; Solium, to deliver a platform for Global Equity Plan Administration; BlackRock, to offer Aladdin Risk for Wealth Management for UBS Financial Advisors; and Broadridge, to create a wealth management industry platform.

© 2018 RIJ Publishing LLC. All rights reserved.

“This time is different.” Economists say that all the time, but it never is. But we believe this time really is different largely because of improved fiscal policy and technological developments. The combination of the two is boosting GDP growth, not just for a year or two but for a protracted period, causing our standard of living to climb more rapidly, keeping the inflation rate in check, and fundamentally altering the oil market. The economic future of this country is far brighter today than it was a decade ago.

First, it is difficult to over-estimate the importance of the corporate tax cut. In 2015 and 2016 growth in investment spending came to a halt as business confidence sank. That was the worst performance for investment since the recession. Productivity growth slowed to a trickle. GDP growth shrank to a disappointing 2.0% pace, which became “the new normal.”

But then Trump pushed through his corporate tax package, which included a cut in the corporate tax rate from 35% to 20%, the ability for large multi-national firms to repatriate overseas earnings to the U.S. at a favorable 15% tax rate, an immediate tax deduction for equipment spending, and a massive movement to eliminate unnecessary, conflicting and confusing government regulations. Suddenly corporate confidence soared. Business leaders opened their wallets and began to spend money on investment.

The pickup in investment spending lifted productivity growth from 1% to 2%. That, in turn, boosted GDP growth from a sleepy 2.0% pace to 3.0%.

But is the recent faster GDP growth a temporary spurt triggered by the tax cuts, or something longer lasting? We believe it is the latter. The 20% corporate tax rate is now competitive with almost all other developed countries. Massive deregulation encourages businesses of all types—small firms in particular—to formulate long-term plans and invest accordingly. The tight labor market encourages firms to spend money on technology to make existing employees more efficient, thus increasing output without increasing their headcount. In economic jargon, they are substituting capital for labor, which boosts productivity growth.

If the pickup in investment spending lasts, productivity growth will accelerate from its anemic 1.0% pace to a steady 2.0%. That will boost the economy’s speed by one percentage point from 1.8% to 2.8%. A near-3.0% GDP growth rate is welcome relief from a few years ago.

If GDP growth accelerates by 1.0%, our standard of living will grow by 1.0%, from today’s 1.5% to 2.5% by the end of the decade. This faster GDP growth comes about partly because of the fiscal policy described above, but also because of technology.

Technology has altered our way of doing business. The Internet came into existence in 1995. The cloud and apps followed in the early 2000s. Those developments revolutionized the way that we all communicate with each other.

Amazon was founded in 1994 and followed quickly by eBay and Google. On-line shopping skyrocketed. Before we purchase anything today, we check prices on the Internet. We can find the lowest price anywhere around the globe. As a result, traditional brick and mortar stores have no pricing power. Should they choose to raise prices, they lose sales. This is having a profound influence on the inflation rate.

In the past year the core CPI has risen 2.2%. If we split the CPI into two parts—goods and services—we find very disparate movements. In the past year, goods prices have declined 0.3%. In contrast, services have risen 3.0%. This outcome highlights the complete inability of goods-producing firms to raise prices.

In the absence of online shopping, we would be looking at a 3.0% inflation rate today rather than 2.0%. That would be far above the Fed’s 2.0% inflation target, and with 3.0% GDP growth (well in excess of the Fed’s estimated 1.8% potential growth) the Fed would be raising interest rates aggressively and the end of the expansion would almost certainly be in sight. But technology has changed that scenario. Inflation remains close to the Fed’s target, which means the Fed can pursue a very gradual return to higher rates with little risk of dumping the economy into recession. All because of technology.

Finally, think about the oil market. Technological improvements like fracking and horizontal drilling have caused U.S. oil production to double in the past seven years.

As a result, the U.S. has surpassed Saudi Arabia and Russia and become the world’s largest producer of crude oil. Next year the U.S. Department of Energy expects U.S. output to climb an additional 10% and further widen the gap between U.S. production and that of its two closest rivals. As a result, OPEC countries no longer have a stranglehold on global oil production. Should they choose to curtail production to inflate oil prices, U.S. drillers can quickly step on the gas and counter much of the shortfall. The U.S. has become a major player in the global oil market. Because of technology.

The world is a different place today than it was 10 years ago. Improved fiscal policy caused by the tax cuts and deregulation have re-invigorated the previously dormant U.S. economy. Technology has changed the entire economic landscape. Because economists have no relevant history to use as a model for the future, we are all flying by the seat of our pants. I believe sustained investment spending and faster productivity growth will boost potential GDP growth from 1.8% to 2.8% within a few years. Others think the recent GDP surge will soon fade and that a recession is looming by 2020. Who is right?

Then, to what extent can we count on technology to suppress inflation?

Finally, how much has the revival of U.S. oil production altered the balance of power between OPEC countries and the rest of the world? What does that mean for oil prices?

Keep in mind that technology is not static, which raises even bigger question. What next “big thing” will fundamentally alter the economic landscape? These sea changes make economics fun—but also challenging.

© 2018 Numbernomics.

Falling equity markets and lower interest rates hurt the funding levels of the four largest Dutch pension funds in October, prompting them to contemplate benefits cuts to participants, IPE.com reported.

Two metal industry pensions, PMT and PME, drew closer to imposing benefit cuts in 2020 after figures published last week showed that their funding ratios had declined three percentage points, to about 101%.

PME said it had already been communicating to members the risk of cuts through all its information channels during the past year. “We are trying to find a balance between warning and unnecessarily worrying our participants,” it said. Cuts can be spread out over a 10-year period, but they are unconditional and cannot be reversed.

The MSCI World index declined by 6.7% during October and the 30-year swap rate dropped almost three basis points, to 1.5%. Interest rates are crucial for discounting future pension liabilities.

Civil service pension ABP saw the value of its assets drop 2.8% to €407bn, while its liabilities rose 0.1% to €399bn. To avoid benefit cuts, its funding ratio must rebound to the required minimum of about 105% by year-end. Benefit cuts must be applied when a plan has been underfunded for five consecutive years.

To PMT and PME, their funding at the end of 2019 will be crucial to avoid cuts. At the end of October, their coverage ratios stood at 102.5% and 101.7%, respectively, compared to the required 104.3%.

© 2018 RIJ Publishing LLC. All rights reserved.

Amid rising sales, Lincoln issues new bonus FIA

Lincoln Financial Group this week launched the Lincoln OptiBlend Plus fixed indexed annuity (FIA), which offers the same fixed and indexed accounts as Lincoln OptiBlend 10, plus an immediate 6% bonus added to the account value.

The product offers three index-linked interest crediting strategies in addition to a fixed account option for accumulation.

An optional lifetime income rider, Lincoln Lifetime Income Edge, is also available with Lincoln OptiBlend Plus and can be elected at issue or added on a contract anniversary for an additional cost.

“Lincoln OptiBlend Plus builds on the success we’ve seen with our Lincoln OptiBlend 10 fixed indexed annuity,” said Tad Fifer, head of Fixed Annuity Sales and RIA Sales & Strategy at Lincoln Financial Distributors. Expansion in the fixed indexed annuity market has contributed to Lincoln’s fixed annuity sales more than doubling, to nearly $900 million in the third quarter, the Lincoln release said.

Seventy percent of pre-retirees claim they can afford to lose only 10% or less of their savings before feeling forced to adjust their retirement plan or savings goals, a recent Lincoln-sponsored survey showed. Among those less than three years away from retirement, 87% were concerned with protecting their accumulated wealth.

TIAA Bank acquires leases and loans from GE Capital’s healthcare business

TIAA Bank has acquired a $1.5 billion portfolio of healthcare equipment leases and loans from GE Capital’s Healthcare Equipment Finance (HEF) business. The move expands the bank’s commercial banking business and enhances its ability to serve institutional clients and healthcare providers, according to a release from the bank.

The acquired healthcare portfolio includes loans and leases to approximately 1,100 hospitals as well as 3,600 physician practices and diagnostic and imaging centers across the United States. Assets financed include imaging, monitoring, respiratory, surgical, ultrasound and lab equipment.

TIAA Bank and GE Capital have also entered into a five-year vendor financing agreement for U.S. customers of GE Healthcare. GE Healthcare Equipment Finance’s team will continue to originate and service transactions under a co-branding arrangement with TIAA Bank.

Executives involved in the deal include Lori Dickerson Fouché, senior executive vice president and CEO of Retail & Institutional Financial Services at TIAA, Blake Wilson, CEO of TIAA’s Retail Financial Services and chairman and CEO of TIAA Bank, and Trevor Schauenberg, president and CEO of GE Capital Industrial Finance.

MassMutual names Carroll as new head of Workplace Distribution

MassMutual has appointed Bob Carroll as its new head of Workplace Distribution. Reporting to Teresa Hassara, head of Workplace Solutions for MassMutual, he will be responsible for executing the firm’s workplace distribution strategy, developing sales talent, increasing revenue and growing MassMutual’s share of the retirement and worksite markets.

Carroll will also represent MassMutual as a thought leader in the retirement and voluntary benefits markets, and partner with key accounts and relationship management teams to drive business growth and retention, a MassMutual release said.

Carroll comes to MassMutual from John Hancock Financial Services, where he was most recently Vice President of National Sales, spearheading strategy for retirement plan product development, marketing, and product distribution through broker dealers, RIAs, and third-party administrators. Previously, he served in a variety of sales leadership roles at Hancock.

Carroll has a Bachelor of Science in Finance and Business Administration from Illinois State University and Series 7, 24 and 63 licenses.

MassMutual provides retirement savings plans through advisors for mid-, large and mega-sized employers in the corporate, Taft-Hartley, government and not-for-profit markets. Its voluntary group benefit offerings include whole life, universal life insurance, critical illness and accident coverage, and executive life and disability income insurance.

The company maintains two nationwide wholesaling networks, including 70 managing directors who support retirement plans in the institutional and emerging markets, and 15 voluntary benefits wholesalers. MassMutual said it plans to expand its voluntary benefits wholesaling team to 21.

Investors Heritage Life enters MYGA annuity business

Investors Heritage Life, a Kentucky-domiciled life insurer specializing in preneed life and final expense insurance, has launched Heritage Builder Annuity, a single-premium deferred, multi-year, rate-guaranteed (MYGA) annuity.

The annuity marks the first product introduced Investors Heritage went private in a transaction with Aquarian Holdings in March, said Harry Lee Waterfield II, Investors Heritage CEO, and John Frye, operating partner at Aquarian, in a release.

The Heritage Builder Annuity was developed after consultations between Investors Heritage, Aquarian and leading annuity distribution companies, the release said. Investors Heritage and Aquarian also refreshed the insurer’s brand and launched a new website in September.

Rudy Sahay, chairman of Investors Heritage and managing partner at Aquarian Holdings, said in a statement that “this annuity [will be] the first of many to come.”

As sponsors of 401(k) plans, employers can boost plan participation by automatically enrolling new employees in plans–a practice made possible by the Pension Protection Act of 2006). They can also raise participation and contribution rates by matching a portion of each employee’s contributions.

There’s been some debate over the years about which factor—auto-enrollment or the (more expensive for the employer) match—drives participation more. A study by a team of Harvard and Yale economists in 2007 showed that most auto-enrolled participants will stay in a plan even if the employer suspends its match.

The match may be more important than previously thought, however. The results of a recent study by analysts Nadia Karamcheva and Justin Falk of the Congressional Budget Office’s Microeconomic Studies Division found that “most of the estimates from the literature substantially understate the effect of matching.”

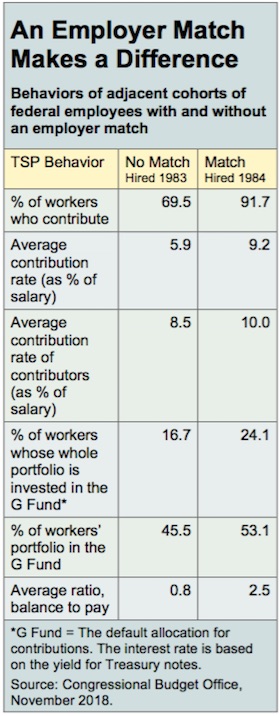

The analysts took advantage of two natural experiments. Before 1984, the federal government offered only a defined benefit pension (without Social Security). In 1984, it began offering federal employees a defined contribution plan (the Thrift Savings Plan or TSP) with a match. It allowed people under the old CSRS system to also contribute to TSP, but with no match. This change provided an opportunity to test the impact of a match on contribution rates.

The second natural experiment took place in August 2010, when the government implemented a policy of automatic enrollment with a default contribution rate of three percent and the “G Fund” as the default investment option. (The G Fund invests in government securities. Its yield is based on the yield for Treasury notes.) This change provided a test of the impact of auto-enrollment.

A microeconomic analysis of the results of these two natural experiments showed that the match had a bigger effect. It increased contribution rates by 22 percentage points. Auto-enrollment increased it by 19 percentage points.

Looking at the long-term impact of the matching contribution, the analysts found that for those with a match, the average ratio of balance to pay was 2.5 to 1 (after an average accumulation period of 28 years). The average ratio of balance to pay for those without a match was 0.8 to 1. Looking at the impact of auto-enrollment (over an average accumulation period of five years), the average ratio of balance to pay was the same (0.4 to 1) for those who were hired just before and just after auto-enrollment was introduced.

In the 2007 Harvard-Yale study, the economists studied the behavior of participants whose plan sponsor switched from a matching contribution to a voluntary employer contribution not contingent on a worker’s contribution. They found that participation rates declined by “at most five to six percentage points” and average contribution rates fell by 0.65%.

Our “results suggest that the match has only a modest impact on opt-out rates,” wrote John Beshears, David Laibson and Brigitte Madrian of Harvard and James Choi of Yale in a 2007 paper, “The Impact of Employer Matching on Savings Plan Participation under Automatic Enrollment.” The same team also looked at data from nine different employers who all used auto-enrollment and varying match structures. It drew similar conclusions.

“We find that a one percentage point decrease in the maximum potential match as a fraction of salary is associated with a 1.8 to 3.8 percentage point decrease in plan participation at six months of eligibility,” the paper said. “We estimate that moving from a typical matching structure of 50% up to 6% of pay contributed to no match would reduce participation under automatic enrollment at six months after plan eligibility by 5 to 11 percentage points.”

The CBO and Harvard studies are quite different, so it’s impossible to say which carries more weight. CBO examined the effect of a match on workers who did not have auto-enrollment, whereas other researchers have looked at the effect of taking away the match from workers who have auto-enrollment.

© 2018 RIJ Publishing LLC. All rights reserved.

Non-variable annuity sales for the third quarter of 2018 were up 4.72% over the prior quarter and 46.26% higher than in the same period last year, based on preliminary sales data gathered by Wink’s Sales & Market Report. Non-variable deferred annuities include the indexed annuity, traditional fixed annuity, and MYGA product lines.

Indexed annuity sales increased by more than 2% over the prior quarter and by more than 38% over the same period last year. Indexed annuities have a floor of no less than zero percent and limited excess interest that is determined by the performance of an external index, such as Standard and Poor’s 500.

Traditional fixed annuity sales increased by 16.7% over the prior quarter and rose by 28.7% over the same period last year. Traditional fixed annuities have a fixed rate that is guaranteed for one year only.

Sales of multi-year guaranteed annuities (MYGA) increased by 8.1% over the prior quarter and were up 63.4% over the same period last year. MYGAs have a fixed rate that is guaranteed for more than one year.

“Recent increases in annuity rates, coupled with incentives being offered by product manufacturers have really translated to sales momentum!” said Wink CEO Sheryl Moore.

Structured annuity sales are estimated to be up nearly 40% from the prior quarter. Structured annuities have a limited negative floor and limited excess interest that is determined by the performance of an external index or subaccounts. “These aren’t indexed annuities, although some companies are marketing them in that manner,” Moore said.

These preliminary results are based on 94% of participation in Wink’s quarterly sales survey representing 97% of the total sales.

Wink currently reports on indexed annuity, fixed annuity, multi-year guaranteed annuity, structured annuity, and multiple life insurance lines’ product sales. It plans to report on variable annuity and all types of income annuity product sales in the future, a release said.

© 2018 RIJ Publishing LLC. All rights reserved.

Almost six in 10 investors (59%) were not aware of any of names of 10 digital advice platforms that were offered to them in a questionnaire, according to a recent survey of investors by Cerulli Associates, the research and consulting firm.

The ten companies (in order of brand-recognition) were Betterment, Merrill Lynch Edge, Go (Fidelity), Intelligent Portfolios (Schwab), Vanguard Personal Advisory Services, Acorns, Wealthfront, Essential Portfolios (TD Ameritrade) Adaptive Portfolios (E*Trade), and Personal Capital.

Awareness of the names of the ten robo-advisors and robo/human hybrid platforms varied by age. Younger investors, predictably, were more aware of the digital advisors than older ones. The percentage answering “none of the above” after seeing the list ranged from 34% (among those under age 30) to 75% (among those age 70 or older).

Cerulli’s fourth quarter 2018 issue of The Cerulli Edge—U.S. Retail Investor Edition details the efforts of 10 of the leading digital-focused financial advice platforms in establishing brand awareness among retail investors and looks at the degree of familiarity that each firm has achieved among prospective investors on a wealth tier basis.

“While increasing awareness is an excellent near-term goal, the ability to accumulate assets under management will determine the ultimate success of these platforms,” said Scott Smith, director at Cerulli, in a press release.

“The largest platforms are affiliated with firms with a long history of serving investors directly, largely through brokerage relationships. In many cases, investors on these platforms began their relationships with the intention of remaining completely self-directed, but eventually found the responsibility more burdensome than rewarding.

“During the five-year time horizon, conversion of brokerage clients to advisor relationships at the largest direct providers will be the primary driver of the digital advice segment,” Smith said. “But more recent entrants’ persistent efforts will allow them to consistently improve their awareness levels among affluent investors and achieve sustainable scale.”

© 2018 RIJ Publishing LLC. All rights reserved.

Self-employed persons, gig economy workers and other individual workers in Oregon can now participate in OregonSaves, the state of Oregon’s public savings option for workers without a savings option at work.

OregonSaves began with a pilot program in July 2017 and is expanding statewide in waves under the direction of Oregon Retirement Savings Board and State Treasurer Tobias Read.

Since the first wave of the program launched in November 2017, tens of thousands of workers have saved more than $9 million towards retirement, according to an OregonSaves release this week. More than 45,000 employees have enrolled through a facilitating employer. Participants in OregonSaves contribute $114 per month on average.

OregonSaves offers Individual Retirement Accounts (IRAs) that are designed to follow workers throughout their careers. Individuals can sign up at saver.oregonsaves.com and save as little as $5 per month through automatic contributions from their bank accounts or through payroll deduction. A simple menu of investment options is available

Oregon workers will continue to be enrolled automatically in OregonSaves if their employer facilitates the program. Oregon employers that do not offer an employer-sponsored retirement plan for their workers are joining the OregonSaves program in a series of waves.

The deadline for the next wave, for employers with 20 or more employees, is December 15, 2018. The program will be fully implemented by the end of 2020.

The retirement savings gap in America is estimated to be at least $6.8 trillion and growing, and more than half of workers have saved nothing, according to the National Institute for Retirement Security. In Oregon, an estimated one million workers lack access to a work-based retirement plan.

“With stylists, usually they don’t retire—they don’t have a retirement,” said Molly Finster, stylist for Annastasia Salon and an OregonSaves participant. “[OregonSaves] makes me feel like I actually have a career, and that’s what I’ve always wanted. Even for my parents to know that I can retire, that I’ll have a retirement someday, is huge … huge.”

© 2018 RIJ Publishing LLC. All rights reserved.

The “sidecar” savings account—a source of emergency cash that rides beside a worker’s retirement account—is being piloted in Britain by the National Employment Savings Trust (NEST), the UK’s nationwide, public-option, auto-enrolled defined contribution plan.

The first employer to test the savings account concept will be Timpsons, a chain of shops specializing in shoe repair. Timpsons will offer the service to its 5,600 workers starting next year, according to a report this week at IPE.com.

In the U.S., the Family Savings Act of 2018, recently passed by the House of Representatives, would clear the way for similar “rainy day” accounts within 401(k) plans in the US. Such funds are inspired by the fact emergency expenses force millions of Americans to dip into their 401(k) accounts.

Title III of the Family Savings Act “permits an individual to establish a universal savings account. An individual may contribute up to $2,500 each taxable year and withdraw the funds tax-free and without penalty at any time and for any use.”

In the UK, the sidecar accounts are designed to improve what officials call “financial resilience.” Employees can save into what NEST has dubbed “jars.” Plan contributions above the auto-enrollment minimum (currently 8% of salary) will overflow into the sidecar savings account until the sidecar balance reaches £1,000. Subsequent contributions go to the retirement fund.

The account would be labeled “for emergencies.” Studies have shown that this kind of framing can influence how judiciously people use the money. Once the sidecar balance falls back below the cap, contributions will automatically split again to pay into both accounts, until the savings account rises to its limit again.

Caroline Rookes, a trustee at NEST and chief executive of the UK’s Money Advice Service (MAS), said roughly a quarter of the UK population had no savings for sudden emergencies.

NEST, which manages £3.8bn (€4.4bn), developed the model with help from the Harvard Kennedy School. JP Morgan Chase’s charitable foundation and MAS are providing financial resources for the trial, while Salary Finance will provide the savings accounts.

© 2018 RIJ Publishing LLC. All rights reserved.

“Auto-portability,” a technology that would expedite a participant’s assets from one 401(k) plan to another when he or she changes jobs, moved closer to reality this week.

The Department of Labor proposed a “prohibited transaction exemption,” or PTE, that would allow Charlotte, NC-based Retirement Clearinghouse (RCH) to offer such a service.

The CEO of RCH (formerly RolloverSystems) is Spencer Williams, a former MassMutual executive. The executive vice president who worked with him to obtain the ruling is Tom Johnson, Head of Policy & Development, also a life insurance industry veteran. Robert L. Johnson (no relation), founder of Black Entertainment Television, owns RCH.

RCH had sought the PTE for several years; the exemption would allow RCH to default participants into its program and charge a fee for its plan-to-plan transfer service, as long as RCH meets a list of DOL conduct requirements.

The public policy argument for auto-portability is that it can prevent “leakage” from 401(k) plans when people change jobs. Too often, workers withdraw small balances when they change jobs rather than roll their money into their next plan–a process that employers don’t necessarily make easy. The problem affects low-income people the most, since they change jobs more often, are more likely to have small account balances, and are more likely to need the cash for emergencies.

The DOL will accept public comments on the proposal for the next 45 days. Once the PTE is granted, RCH, which has piloted the program and proven the concept, will work on building a network of recordkeepers and plan sponsors to use the service.

“The advisory opinion is especially important to the plan sponsor. It makes clear the plan sponsor is not a fiduciary. Plan sponsors are averse to things that are not clear in the law today. By naming us as a fiduciary and granting us relief, the PTE also allows us to get paid for the roll in service,” Williams told RIJ this week.

“There are a significant number of conditions that we have to meet. Early on, we’ll have to prove that our fees are reasonable. There is also an extensive system of notices that we have to provide to participants to ensure that it’s a voluntary system. DOL is only granting the exemption for five years. The comment period for the Proposed Exemption closes on Dec 24th and we would expect the final Exemption to be issued 2-3 months later.”

Williams and RCH vice president Tom Johnson, with guidance from Groom Law Group, spent much of the past five years speaking to various groups about auto-portability and building bipartisan support it.

“We went to nearly all the groups that have a dog in this fight, on the left as well as the right,” Johnson said. “At one point we were asked, ‘Whose ox do you gore with this?’ And I said, ‘Other than Bob’s Big Screen TV Outlet, everybody wins.’” (The reference was to the perceived conflict that some 401(k) participants have between saving and buying a large smart television.)

“To deliver auto-portability we have to create a giant network where RCH sits at the hub and the recordkeepers are the spokes,” Johnson said, noting that as few as 10 large recordkeepers account for 80% of the 401(k) business in the U.S. “We have to go to the recordkeepers and ask them to implement our technology. It’s not complicated, but it still represents a technology spend.

“Along the way, you also have to create transmission standards. We act as an aggregator so that the recordkeepers don’t have to talk to each other, just to us. We’ll have transmission standards for that,” he added. RCH acts as the transmitter of assets and data from one plan to the next, not as an asset custodian. Independent custodians will warehouse the small accounts after they leave one 401(k) and before they arrive at the next.

© 2018 RIJ Publishing LLC. All rights reserved.