What middle-class retirees like/don’t like about Obamacare

The Affordable Care Act’s elimination of pre-existing condition exclusions, provision of free annual Medicare check-ups, and initiatives to cut Medicare costs are the aspects of the new health care law that middle-income U.S. retirees like best, according to a survey by Bankers Life and Casualty Company Center for a Secure Retirement.

Just over half (52%) of retirees surveyed disliked the law’s so-called personal mandate—the requirement that individuals own health insurance or pay a penalty, the survey showed. A nationwide sample of 800 retired Americans ages 55+ with annual household incomes of $25,000 to $75,000 participated in the internet-based survey.

Only about half of middle-income retirees say they understand how the ACA affects them. Women are the least familiar with “Obamacare”. Three times as many women do not feel confident in their understanding of ACA as compared with those who say they understand how the law affects them (56% to 17%, respectively).

Two aspects of the ACA that affect retirees are not well understood by retirees. One in six (18%) retirees doesn’t know that ACA caps health insurance premiums for older people relative to rates for younger people. The same percentage doesn’t know that ACA the “donut hole” in Medicare Part D prescription drug coverage.

Retirees and insurance exchanges

Nearly one-fourth (23%) of middle-income retirees say they retired for personal health or disability reasons, suggesting that they will need the ACA until they reach age 65. Of the 27% of middle-income retirees ages 55 to 64 who don’t receive any type of government insurance coverage, 15% have purchased their own private health insurance policy and 12% don’t currently have health insurance.

A slightly greater total percentage of retirees ages 55 to 65 find themselves as potential beneficiaries of the state health insurance exchanges than the percentage of the working population. More than four in ten (42%) middle-income retirees ages 55 to 65 say they either have or will investigate the cost of health insurance through an exchange.

The research for this report was conducted in September 2013 for the Bankers Life and Casualty Company Center for a Secure Retirement by The Blackstone Group conducted the research for the report for Bankers Life in September 2013. The full report is online at CenterForASecureRetirement.com. All survey participants had heard of the Affordable Care Act (Obamacare) and were not enrolled in Medicaid.

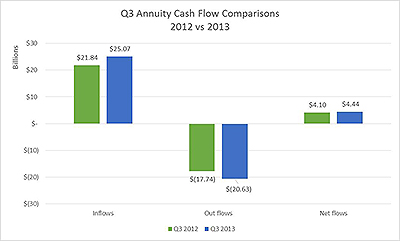

New York Life claims dominance in SPIA and DIA markets

New York Life said in a release this week that it has a 33% share of the U.S. market for fixed immediate annuities and a 44% share of the market deferred income annuities, according to LIMRA.

According to the company, its overall income annuity sales rose 13% in the first half of 2013 over the same period in 2012. This year is the first time that deferred income annuities have their own category in the leading industry rankings.

The release said that, according to LIMRA (the life insurance marketing and research association), there is a “growing interest in this market,” and it estimated that “collectively consumers age 45-59 have almost $10 trillion in financial assets so we anticipate these products will to continue to have remarkable growth.”

RICP designation gains momentum at The American College

With more than 3,000 licensed advisors and insurance agents registered so far, and about 250 graduates, The American College of Financial Services said its program for offering a Retirement Income Certified Professional (RICP) designation is the fastest-growing financial advisor credential program launched in the school’s 87-year history.

“Many consumers don’t have pensions to rely on, and there is deep confusion about the safety of government bonds and how Medicare and Social Security may change in the future,” said Larry Barton, president and CEO of the Bryn Mawr, Pa-based university, in a release.

“The three, intense courses that are delivered strictly online, with detailed case studies and challenges on how to help all clients, from those at-risk for poverty all the way to the ultra affluent, has delivered unlike anything we have seen over nine decades.”

The program addresses such questions as:

- What is the best strategy for meeting a client’s income needs in retirement?

- What is the safe withdrawal rate from a portfolio?

- How should portfolios be managed differently during the course of retirement?

- How can clients maximize income in a low-interest-rate environment?

- What is the most tax-efficient withdrawal strategy?

- How can clients choose the best Social Security claiming strategy?

- How do income annuities and employer-sponsored benefits fit into the mix?

The RICP curriculum contains college-level courses on:

- Retirement Income Process, Strategies and Solutions

- Sources of Retirement Income

- Managing the Retirement Income Plan

Head of Vanguard fixed income group to retire

Robert F. Auwaerter, principal and head of the Vanguard Fixed Income Group, today announced his intention to retire after 32 years with the firm, effective in March 2014. He joined Vanguard in 1981 when the company internalized the management of its money market and municipal bond funds, which then had assets of about $1.3 billion.

Today, the Vanguard Fixed Income Group manages nearly $750 billion invested in 70 taxable and tax-exempt bond, taxable and tax-exempt money market, and stable value funds. The Group oversees about $450 billion in actively managed funds and approximately $300 billion in bond index and exchange-traded funds.

Mr. Auwaerter, who plans to step down in March 2014, is responsible for the portfolio management, strategy, credit research, trading, and planning functions for the Fixed Income Group, which comprises 120 investment professionals and support staff.

Gregory Davis, CFA, will assume the position of head of the Vanguard Fixed Income Group. Mr. Davis, 43, currently serves as chief investment officer of the Asia Pacific region and is a director of Vanguard Investments Australia.

Mr. Davis joined Vanguard in November 1999 and, prior to his current position, served as a senior portfolio manager and head of bond indexing in the Vanguard Fixed Income Group. Mr. Davis and his team then managed more than $200 billion in bond index fund portfolios.

Mr. Davis earned a B.S. in insurance from Pennsylvania State University and an M.B.A. in finance from The Wharton School of the University of Pennsylvania.

Mr. Auwaerter began his career in 1978 at Continental Illinois National Bank and Trust Company. He serves on the Fixed Income Forum Advisory Board and the Credit Roundtable Advisory Board. In 2012, the Fixed Income Analysts Society elected Mr. Auwaerter to its Fixed Income Hall of Fame.

Mr. Auwaerter earned a B.S. in finance from The Wharton School of the University of Pennsylvania and an M.B.A. from the Kellogg Graduate School of Management of Northwestern University.

MassMutual to pay record $1.49 billion dividend

MassMutual will pay its largest dividend in 150 years—$1.49 billion—to eligible participating policyowners in 2014, the company announced this week. The payout reflects a dividend interest rateof 7.1% for eligible participating permanent life and annuity blocks of business, up from last year’s rate of 7% even.

The approved estimated payout represents an increase of $101 million – or about 7.3% – from the 2013 estimated payout and reflects updated investment, mortality, morbidity, expense and other experience, the company said in a release.

Strong performance by MassMutual’s asset management subsidiaries—OppenheimerFunds, Babson Capital Management and Baring Asset Management—and its non-participating businesses (retirement services and non-participating product lines) were key contributor to the strong dividend, the release said.

The estimated record payout comes at a time when MassMutual maintains among the highest financial strength ratings2 in its industry and is reporting very strong levels of surplus of approximately $12 billion and total adjusted capital over $14 billion; both are key indicators of the company’s overall financial strength. The 2014 payout marks the 16th consecutive year that MassMutual’s estimated payout exceeds $1 billion, and the company has paid $20 billion in dividends over the past 20 years.

Of the total dividend payout, an estimated $1.47 billion was been approved for eligible participating owners of whole life policies. More than 99% of eligible participating life policies will receive a dividend in 2013 that is the same or higher than they received in 2013. Whole life policyowners can use dividends in cash or use them to pay premiums, purchase paid-up additional insurance coverage, accumulate at interest, or repay policy loans and policy loan interest.

Investors want trustworthy advisers: Jackson National

Jackson National’s inaugural 2013 Jackson Investor Education Survey was released week, revealing the opinions of 500 representative U.S. pre-retirees between ages 45 and 65 about retirement, investing and financial education.

Examples of findings from executive summary include: 2013 Jackson Investor Education Survey Executive Summary.

- “Having an advisor whom I trust and who really gets me” was the answer chosen most frequently by men (42%) and women (44%) to the question, “What would make the most positive difference in your current financial outlook?” (Less than half of all respondents were currently working with an advisor.)

- “Honesty, financial/investment knowledge and track record” are more important than “ability to communicate” and “responsiveness to needs” in an advisor, men and women agreed.

- 33% of women and nearly 40% of men said they would benefit from professional financial advice, even though they said they understood the fundamentals of investing.

- 5% of women and 3% of men classified themselves as “Ostriches,” or those who just bury their heads in the sand and hope for the best.

- Less than one percent of both genders classified themselves as “Socializers;” i.e., those who based financial decisions on information from social media outlets.

- Financial education was considered a top educational priority by fewer than half of those surveyed.

- “Saving enough for retirement” was the top financial concern for 74% of women and almost 76% of men.

- 14% of men and 13% of women said they don’t have a good understanding of financial/investment products.

- 11.8% of women respondents and 4.3% of men said they would need intensive education to feel “even remotely confident” making investment decisions.

Jefferson National touts the savings made possible by its Monument Advisor VA

Jefferson National estimates that its flat-fee Monument Advisor variable annuities have reduced insurance fees for Registered Investment Advisors (RIAs), fee-based advisers and their clients by over $60 million since it was launched in 2005.

An exchange from a traditional VA with insurance fees averaging 1.35% per year to Jefferson National’s flat-fee VA of $20 per month can save an average of $2,500 in one year and $144,794 over 20 years, based on tax-deferred compounding.

Unlike most variable annuities sold in recent years, which emphasis their lifetime income benefits, Monument Advisor is sold to advisers who want to take advantage of the ability to invest almost unlimited of after-tax money in an account where the assets grow tax-deferred until withdrawal.

Alternative investments drive hiring by asset managers

Almost half (47%) of asset managers expect to hire dedicated marketing personnel and 41% expect to hire dedicated sales personnel in the next 12 months to support alternative investments, according to new research from Cerulli Associates, the Boston-based global analytics firm.

Firms have hired more dedicated sales professionals than any other alternatives-related position in the past year, Cerulli said in a release. The number of sales personnel dedicated to alternative products increased 54% from 2012 to 2013 among managers that distributed alternatives to both retail and institutional clients.

As alternatives are becoming an increased focus and a larger business line for some firms, Cerulli recommends continued evaluation of support levels to ensure that the appropriate resources are committed to alternative product lines on an ongoing basis.

© 2013 RIJ Publishing LLC. All rights reserved.