Only two years ago, AXA Equitable was the 800-pound gorilla of variable annuity sales. In the first three quarters of 2007, the insurer sold nearly $12 billion worth of its Accumulator contract, which boasted a 6.5% roll-up on a GMIB rider.

Then the gorilla slimmed down, due largely to the financial crisis. AXA variable annuity sales totaled less than $6 billion in the first nine months of 2009, a 50% decline in 24 months. But because the whole industry suffered, its market share fell only to 6.4%, from 8.8%.

Now the global insurance giant is pounding its chest again, with its first new variable annuity product since the crisis. The new product is designed to give investors a way to benefit from the interest rate increases that seem inevitable. And if rates do go up, it could give them a higher roll-up and higher payout rate than the five percent currently offered by competitors.

“In times of historically low interest rates, we’re giving clients an opportunity to benefit from rising rates. They can let their benefit base grow by 10-year Treasury rates plus one percent or withdraw at 10-year Treasury plus one percent,” said Steve Mabry, senior vice president of annuity product development. The current rate for the product, which has been rolled out through AXA Equitable career agents but not third-party distributors, is rounded to 5%, based on a 3.8% 10-year Treasury rate.

“In times of historically low interest rates, we’re giving clients an opportunity to benefit from rising rates. They can let their benefit base grow by 10-year Treasury rates plus one percent or withdraw at 10-year Treasury plus one percent,” said Steve Mabry, senior vice president of annuity product development. The current rate for the product, which has been rolled out through AXA Equitable career agents but not third-party distributors, is rounded to 5%, based on a 3.8% 10-year Treasury rate.

Called the Retirement Cornerstone Series, the contract contains two buckets or “sleeves.” The first sleeve is a traditional variable annuity separate account with some 90 investment options, ranging from cheap index funds to aggressive actively managed growth funds.

The second sleeve is also a separate account, but its value is protected by a living benefit rider that provides a roll-up and a guaranteed lifetime income benefit. Both the roll-up and payout rates are linked to the 10-year Treasury rate. The client pays a rider fee only on the assets (or rather, on the benefit base achieved by the assets) in the second sleeve.

On each contract anniversary during the accumulation period, the guaranteed benefit base—the sum of contributions to the second sleeve minus withdrawals—automatically compounds at a rate equal to about one percent over the prevailing 10-year Treasury rate, but no less than four percent and no more than eight percent. Every three years, the value of the benefit base is also ratcheted up to the market value of the assets in the sleeve, if it’s higher.

In any year during the life of the contract, the client can also withdraw money at a rate determined by the same formula—one percentage point above the prevailing 10-year Treasury rate (but no less than four or more than eight but percent)—without reducing the guaranteed income base. As is typical for such riders, excess withdrawals reduce the benefit base on which the value of subsequent withdrawals will be calculated.

“It’s income insurance,” Mabry said. “If you retire with $500,000, what do you do with it? If you invest in mutual funds, there’s no guarantee that if markets go down you won’t be out of money when you’re 80. With this, you’re guaranteed a certain amount of income for life. It means you can invest in equities with peace of mind.”

The contract is designed to adapt to an investor’s changing needs. The contract owner or advisor decides how much money to put in each sleeve, or when to transfer money from the growth sleeve to the income sleeve. Presumably, clients will gradually move assets into the protected sleeve as they get older as a way of taking money off the table.

“We’re targeting younger audiences by saying, ‘If you don’t want to pay for the guarantee right away, you don’t have to. When you’re ready to lock in some of your gains, you can switch to lifetime income.’ That’s where we’re seeing excitement in the field,” Mabry said.

“People can invest on the mutual side, and not incur the guarantee fee until they’re ready. When they are ready, they can do a 10% sweep per year or whatever they want into the guaranteed account. We give them a lot of flexibility to engineer their income,” he added. If the client’s account value in the protected sleeve falls to zero during his or her lifetime, the insurer pays either a fixed 4%, 5% or 6% (depending on whether the money runs out when the client is younger than 85, 86 to 94, or over 95, respectively) of the benefit base each year until death.

The contract’s separate account fees range from 1.3% to 1.7% per year, depending on the share class chosen. There’s a “ratchet” death benefit option for 25 basis points and an enhanced death benefit for 80 basis points. The guaranteed income benefit charge starts at 0.80% per year, with a maximum of 1.1%. Annual fund management fees range from 39 basis points to 1.68%, depending on the fund.

“We actually looked at this product before the crisis,” Mabry told RIJ. “We were trying to think of something for people who were worried about inflation. Now we’re in a period of historically low interest rates. Most people think rates are going up and this design allows people to participate in a rising interest rate environment.”

Noel Abkemeier, an annuity analyst at Milliman, liked the new AXA contract, based on a reading of the prospectus. “Historically, the 10-year Treasury rate has been around 6% and in the ‘aughts’ it was 4.5%. This suggests that the roll-up might average around 6% and withdrawals can be around 6%. And the withdrawals are based on a growing roll-up benefit base.”

At those rates, Abkemeier said, a healthy person stands a good chance of still being alive if or when his actual account balance drops to zero, and of getting something other than his own money back from the insurance company. “The chance of collecting is reasonably good,” he noted. He pointed out, however, the payout rates become somewhat less generous—and fixed, rather than floating—after the contract owner’s account goes to zero.

© 2010 RIJ Publishing. All rights reserved.

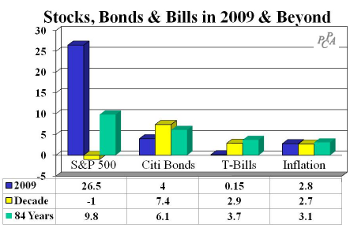

The worst calendar-decade ever

The worst calendar-decade ever

As the exhibit on the right shows, every investment style had substantial gains in 2009. Smaller companies gained more than 40%, exceeding the 24% return to larger companies. Similarly, growth outperformed value, earning 37% versus 29%.

As the exhibit on the right shows, every investment style had substantial gains in 2009. Smaller companies gained more than 40%, exceeding the 24% return to larger companies. Similarly, growth outperformed value, earning 37% versus 29%.