Visions of beggars pushing wheelbarrows of banknotes sprang to America’s collective financial conscience on May 12 when the Bureau of Labor Statistics issued its monthly Consumer Price Index report. It showed a 4.2% rise in the index between April 2020 and April 2021.

Rising prices of petroleum products, used cars and trucks, lodging away from home, and airline tickets drove the increase. Because we’re so accustomed to low inflation (except in housing, equities and health care), that unusual increase launched a thousand headlines.

Will the Fed act, Wall Street wondered? Will it try to cool off the economy with an interest rate hike? That’s not likely (the Fed has been propping up bond prices and trying to stimulate employment), but the S&P 500 dropped 4% on May 12. It has since recovered, though not quite to its all-time high of 4,232, posted on May 3.

How does the Fed formulate inflation policy? How do CEOs form their inflation expectations? In a new study from the National Bureau of Economic Research, academic researchers try to answer those questions. Given the timeliness of the topic, we give this paper top billing in this month’s edition of RIJ’s Research Roundup.

Below, you’ll also find synopses of new research about:

- The reasons why rational retirees keep saving

- The hybridized stock-picking capabilities of “centaurs”

- The four financial biases that affluent people avoid

- The impact on male mortality rates of working longer

“The Inflation Expectations of US Firms: Evidence from a New Survey,” by Bernardo Candia and Yuriy Gorodnichenko, University of California-Berkeley, and Olivier Coibion, University of Texas-Austin. NBER Working Paper 28836, May 2021.

Economics, like life, is rife with irony. Although Federal Reserve policymakers say they take their cues about inflationary trends from the CEOs of US companies, CEOs don’t pay much attention to inflation, aren’t informed about it, and most can’t name the Fed’s target inflation rate.

And, contrary to economic theory, the inflation expectations of CEOs are not “anchored” in any past inflation rate. CEOs aren’t much more informed about inflation than households, which aren’t informed at all.

“The inflation expectations of US firms’ managers display little anchoring: high and dispersed inflation expectations, high levels of uncertainty in their inflation forecasts, large revisions in both short-run and long-run expectations, and a strong correlation between the changes in short-run and long-run inflation expectations,” write authors Bernardo Candia, Olivier Coibion, and Yuriy Gorodnichenko.

The findings were based on the authors’ Survey of Firms’ Inflation Expectations (“SoFIE”) since 2018. Each quarter, a representative panel of CEOs respondents is asked for their inflation expectations in the US over the next 12 months and monetary policy. They are also asked for their “ long-run inflation expectations, perceived recent levels of inflation, uncertainty about future inflation risk, as well as knowledge of the Federal Reserve’s inflation target.”

Only 20% of CEOs correctly identified the Fed’s inflation target (2%) and nearly two-thirds were “unwilling to even guess what the target is.” Of those who did, less than 50% thought it was between 1.5% and 2.5%. “Managers disagree just as much about what inflation has been over the last twelve months as they do about what it will be in the future, even though the former is publicly and freely available,” the study showed.

Data from the survey shows “just how uninformed US firms are with respect to both inflation and monetary policy,” according to the paper. The irony of the findings is stated below.

“Firms’ inflation expectations are central to understanding the link between the nominal and real sides of the economy and therefore play a fundamental role in determining the nature of optimal monetary policy. Indeed, policymakers themselves have long emphasized the importance of firms’ inflation expectations in how they think about optimal policy, as illustrated in the initial quote,” the authors write.

“Why Do Couples and Singles Save During Retirement?” by Mariacristina De Nardi, University of Minnesota and Federal Reserve Bank of Minneapolis, Eric French, Cambridge University, John Bailey Jones, Federal Reserve Bank of Richmond, and Rory McGee, University of Western Ontario. NBER Working Paper No. 28828, May 2021.

Florida’s retirees are famous for lining up at oceanside diners for the “Early Bird Special” discounts. But what compels retirees in general to economize? A team of economists at the Federal Reserve and elsewhere provide answers in their new paper: “Why Do Couples and Singles Save During Retirement?”

“While the savings of singles tend to fall with age, those of retired couples tend to increase or stay constant until one of the spouses dies.” the researchers write. “While medical expenses are an important driver of the savings of middle-income singles, bequest motives matter for couples and high-income singles, and generate transfers to non-spousal heirs whenever a household member dies.”

The study implies that the high-PI elderly get as much or more “utility” (i.e., reward) from giving money to heirs to enjoy than spending it on their own pleasures. Those who have high PI are by definition already protected from running out of money before they die. Pursuit of personal pleasures presumably ebbs as people enter their “no-go” 80s.

The paper’s results have policy implications. “Couples and high-PI singles can easily self-insure against medical spending risk because they save to leave bequests,” the authors write. “Low-PI singles are well insured through Medicaid and do not need to save for medical expenses.

“In contrast, middle-PI singles set aside significant amounts of wealth for precautionary purposes because they are not rich enough to want to leave bequests, but are too rich to qualify for Medicaid. It is thus the middle-PI singles who would respond most to changes in public health insurance.”

“From Man vs. Machine to Man + Machine: The Art and AI of Stock Analyses,” by Sean Cao and Baozhong Yang of Georgia State University, Wei Jiang, Columbia University, and Junbo L. Wang, Louisiana State University. NBER Working Paper No. 28800, May 2021.

If IBM’s Big Blue could outplay grandmaster Gary Kasparov at chess, could an artificial stock analyst using machine learning techniques (“artificial intelligence”) outperform Wall Street analysts at evaluating public companies and predicting future returns?

Yes and no, say four professors at US graduate business schools who built their own AI equity analyst and then compared its alpha-predicting abilities to those of humans after feeding it masses of corporate financial information, qualitative disclosure and macroeconomic indicators.”

The most accurate stock analyst, they found, is what Kasparov himself called a centaur: a human analyst assisted by an AI co-pilot.

The AI analyst tends to outperform people when the “firm is complex, and when information is high-dimensional, transparent and voluminous. Human analysts remain competitive when critical information requires institutional knowledge (such as the nature of intangible assets).

“The edge of the AI over human analysts declines over time when analysts gain access to alternative data and to in-house AI resources. “Combining AI’s computational power and the human art of understanding soft information produces the highest potential in generating accurate forecasts. Our paper portraits a future of ‘machine plus human’ (instead of human displacement) in high-skill professions.”

The best analyst is the “‘centaur’ analyst, i.e., an analyst who makes forecasts that combine their own knowledge and the outputs/recommendations from AI models.” When the researchers supplemented the AI analyst’s information with forecasts by human Wall Street analysts, the resulting “man + machine” or “centaur” model outperformed 57.3% of the forecasts made by analysts, and outperformed the AI-only model in all years.

“Thus, AI analyst does not displace human analysts yet; and in fact an investor or analyst who combines AI’s computational power and the human art of understanding soft information can attain the best performance.”

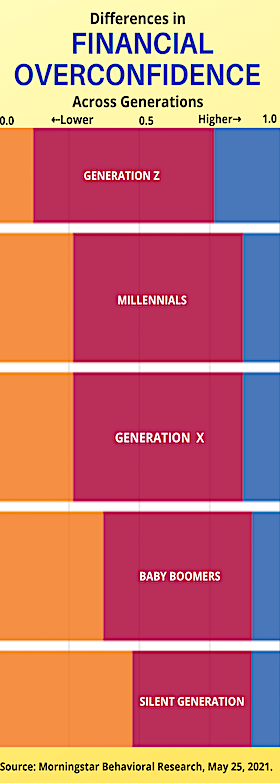

“The Financial Impact of Behavioral Biases: Understanding the extent and importance of behavioral biases,” by Sarwari Das, Behavioral Researcher, Sagneet Kaur, associate director of Behavioral Research, Steve Wendel, head of Behavioral Science, at Morningstar Behavioral Finance, May 25, 2021.

The more biased a person’s financial behavior—for example, the more a person believes in their own uneducated judgments, or the less a person understands how compound interest works—the less money they tend to have, according to a study released this week by Morningstar, Inc. Morningstar’s researchers found:

- The majority of Americans show biases of present bias, loss aversion, overconfidence, and base rate neglect. Each of these biases reflects a kind of intellectual myopia where people give too much importance to very recent events, very negative events, and personal views, and where they give too little importance to the effects of long-term compound interest.

- On average, younger people showed higher levels of overconfidence compared with older individuals.

- Higher bias levels directly correlate with lower checking and 401(k) balances, lower self-reported credit scores, failure to plan ahead and failure to save and invest.

- Some common perceptions about financial biases may be misguided—neither gender is more biased than the other.

The Morningstar analysts surveyed a nationally representative sample of 1,211 Americans, sourced from NORC’s (University of Chicago) AmeriSpeak panel. Participants completed a “bias assessment” survey, which included questions for six biases and a measure of a person’s financial health. The biases included were:

Present Bias: The tendency to overvalue smaller rewards in the present at the expense of long-term goals.

Base Rate Neglect: The tendency to estimate the likelihood of an event on the basis of new, readily available information while neglecting the actual underlying probability of that event.

Overconfidence: The tendency to overweigh one’s own abilities or information when making an investment decision.

Loss Aversion: The tendency to fear losses relative to gains and relative to a reference point.

Exponential Growth Bias: The tendency to underestimate the impact of compound interest.

Gambler’s Fallacy: The tendency to believe that a random event is less (or more) likely to happen following a series of similar events—thus over (or under) predicting reversals in series like market trends.

“Do Men Who Work Longer Live Longer? Evidence from the Netherlands,” by Alice Zulkarnain, the CPB Netherlands Bureau for Economic Policy Analysis and Center for Retirement Research at Boston College, and Matthew S. Rutledge, an associate professor of the practice of economics at Boston College and a CRR research fellow, May 2021.

For tenured professors and others who live by their brains and more or less dictate their own schedules, working past age 60 or even 65 isn’t a heavy lift. Not so for electricians and plumbers, whose knees and hips are worn out by that age. So governments find it difficult to set one-size-fits-all retirement ages.

Yet, with the ratio of retirees-to-workers rising, governments have financial reasons to encourage everyone to work longer, pay taxes longer, save longer, and spend fewer years in retirement. But if working longer caused people to live longer—and collect public or government pensions longer—the policy could backfire.

Analysts at the Center for Retirement Research (CRR) at Boston College reviewed a real-world experiment in the Netherlands to see the impact of delayed-retirement tax incentives on worker behavior and mortality.

A few years ago, the Dutch government established a tax incentive aimed at encouraging men to work past age 60. The Netherlands’ Dootwerkbonus, introduced in 2009 and repealed in 2013, reduced taxes on labor income for each year a person worked after age 62. This bonus, in the form of a tax credit automatically applied at filing, was substantial: up to 5% of taxable income (subject to a cap) for people age 62, increasing to 10% at age 64 before phasing out at older ages. Those born from 1946 to 1949 stood to benefit the most. A group of workers born in 1943-1945 served as a control.

Men who worked longer due to the policy change saw their mortality rate in their 60s fall from about 8% to 6%. That suggests a two-month extension to their life expectancies between the ages 62-65. Extrapolating into the future, the increase in life expectancy could end up being more significant.

“If the reduction in men’s mortality is only temporary, their remaining life expectancy after age 60 would rise from 21.5 years to 21.7 years, or about two extra months. If, however, the effect on mortality is longer lasting, remaining life expectancy could increase by about two full years,” the authors wrote.

© 2021 RIJ Publishing LLC. All rights reserved.