Canadian firm buys Ohio National for $1 billion

Constellation Insurance Holdings Inc., an insurance holding company financed by Canadian public pension plans, is buying the mutual holding company that owns Ohio National Financial Services for $1 billion, the companies announced today.

Ohio National Mutual Holdings Inc. is the parent of Ohio National Financial Services. The firm’s flagship subsidiary, The Ohio National Life Insurance Company, has operated in Cincinnati since 1909.

Constellation plans to help Ohio National shift away from the mutual holding company structure, through a process called a “sponsored demutualization,” the companies said. Constellation will provide $500 million that Ohio National could use to pay the policyholder owners to extinguish their mutual holding company ownership interests, the companies said.

Also, Constellation will add $500 million in capital to the company over four years, to strengthen its capital position and its ability to meet its obligations, the companies said in a release.

Barbara Turner, Ohio National’s CEO, said in a statement that the company agreed to the deal “in the midst of a challenging economic environment, historically low interest rates, increased regulatory costs and pressure for the entire industry.” The Constellation deal will fortify Ohio National with more capital and create a more flexible capital structure, she said.

Anurag Chandra, the founder, chairman and CEO of Constellation, said his firm wants to give Ohio National and other insurers more access to capital, “while preserving the independence, brand, existing operations and culture for which they are recognized.”

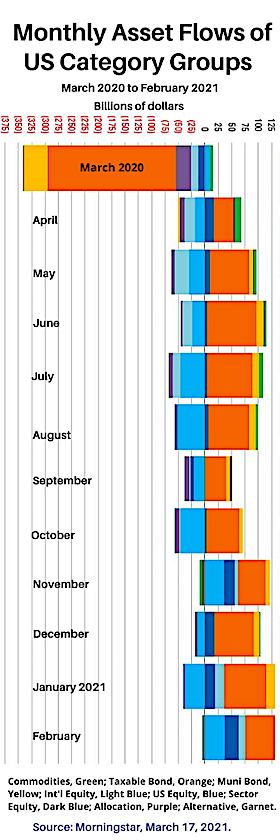

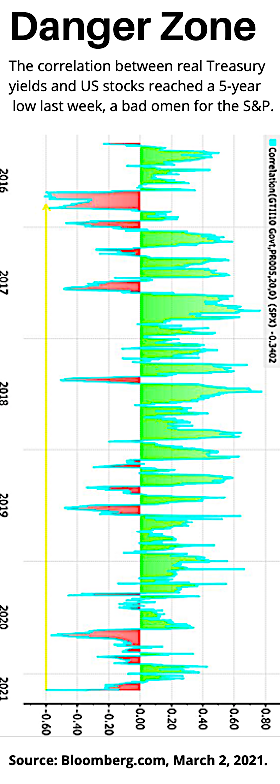

Net income of life/annuity industry fell almost 50% in 2020

The US life/annuity (L/A) insurance industry saw its net income cut nearly in half in 2020, to $24 billion from $45 billion. These preliminary results are detailed in a new Best’s Special Report, titled, “First Look: 12 Month 2020 Life/Annuity Financial Results.”

The data is derived from companies’ annual statutory statements received as of March 17, 2020, representing an estimated 98% of total industry premiums and annuity considerations.

According to the report, premiums and annuity considerations for the L/A industry declined 8.3%, as Jackson National Life entered into a coinsurance agreement with Athene Life Re and ceded $24 billion of individual annuities to Bermuda. Increases in the amortization of interest maintenance reserve and other income offset the decline, and resulted in a 4.7% drop in total income, compared with prior year.

Due to the drop in income exceeding a 2.6% reduction in expenses, pretax net operating gain fell by 35.0% to $39.9 billion from the prior year. Income tax expense was also down in 2020, by $4.1 billion, but net realized capital losses increased by $3.9 billion, resulting in the drop of total industry net income to $24 billion.

New index annuity income rider from AIG

AIG added a new “protected lifetime income benefit,” to the contracts in its Power Series of index annuities, according to a release this week from AIG Life & Retirement, a division of American International Group, Inc. The contracts are available only through agents of independent marketing organizations (IMOs).

The Lifetime Income Choice benefit rider is automatically included at contract issue in the Power 7 Protector Plus Income and Power 10 Protector Plus Income Index Annuities for an annual fee of 1.10% of the so-called Income Base.

The Income Base is initially equal to the first eligible purchase premium. It increases when new premiums are paid, and it is adjusted for withdrawals. On each contract anniversary, the owner’s Income Base is marked up to which ever is greater: the contract value on the anniversary value or the Income Base plus any available income credits.

The rider includes two options, Max Income and Level Income. The Max Income option weights income toward the early, so-called go-go years of retirement. Level Income provides a consistent income for life. Both options guarantee income growth every year prior to activating the lifetime income benefit.

Lifetime Income Choice locks in the greater of cumulative interest earned or an annual income credit of 5.50% as a deferral bonus for every year that lifetime withdrawals are delayed, “ensuring that future income will increase, even if index performance is flat or down,” the release said.

When contract owners start taking income, Max Income offers initial annual withdrawal rates ranging from 3.65% at ages 50 to 59 to 7.25% at age 72 and older for a single person. Rates are lower for couples. If the annuity’s account balance is depleted before the contract owner(s) die, the contract owner(s) will receive annual income of up to 4.00% for life.

The Level Income option offers a level payout for life, even if the annuity’s account balance is depleted. The annual withdrawal rate for one person ranges from 3.4% at ages 50 to 59 to 5.85% at age 72 and older. The Max Income option may not provide more cumulative income than the Level Income option.

SIMON adds First Trust Target Outcome ETFs

First Trust’s Target Outcome ETFs are now available at SIMON, a structured products sales, education and management platform serving some 85,000 asset managers with more than $3 trillion under management. SIMON offers “on-demand education, an intuitive marketplace, real-time analytics, and lifecycle management,” a release said.

First Trust Advisors L.P., the second largest provider of actively managed funds in the US, said in the release that its recently issued Target Outcome ETFs have grown to over $1.6 billion, as of the end of last year.

First Trust is initially offering buffered ETFs tied to the SPY, QQQ, and EFA indexes in SIMON’s ETF Marketplace, with additional offerings in the pipeline. The ETFs offer index gains up to a cap and down to a “buffer,” which protects investors up to but not beyond a downside buffer limit.

SIMON’s digital platform enables financial professionals to learn about, analyze, and invest in defined outcome ETFs.

KKR, owner of Global Atlantic, reports earnings

Between January 1 and March 22 of this year, KKR, the investment company that recently acquired Global Atlantic Holdings, earned gross realized carried interest and total realized investment income of approximately $600 million, according to a “monetization activity update” by the firm.

The earnings were driven primarily by strategic and secondary sale transactions that have closed quarter to-date, as well as dividend and interest income from KKR’s balance sheet portfolio, according to the update.

“The estimate disclosed above is not intended to predict or represent the total revenues for the full quarter ending March 31, 2021, because it does not include the results or impact of any other sources of income, including fee income, losses or expenses. This estimate is also not necessarily indicative of the results that may be expected for any other period, including the entire year ending December 31, 2021,” the release said.

KKR offers alternative asset management and capital markets and insurance solutions. The company sponsors investment funds that invest in private equity, credit and real assets and has strategic partners that manage hedge funds. Its insurance subsidiaries offer retirement, life and reinsurance products under the management of The Global Atlantic Financial Group.

Voya, Morningstar in managed accounts partnership

Voya Financial, Inc., and Morningstar Investment Management LLC are collaborating on a new adviser managed accounts advisory program for Voya’s suite of financial wellness offerings, to be used by Registered Investment Advisors (RIAs) who advise retirement plan participants.

A new Voya survey shows that 76%)of working Americans currently enrolled in a workplace retirement plan want access to a financial adviser. New research from Morningstar Investment Management suggests that remote-working arrangements are likely to increase demand for managed accounts.

Remote workers are less likely to use default investments (such as target-date funds) than personalized advice options (such as managed accounts), Morningstar’s research showed..

The same study also notes that participants who use managed accounts tend to save more for retirement — both when the service is offered as an opt-in and opt-out method.3

When Voya serves as plan recordkeeper, Morningstar Investment Management provides the technology support for adviser managed accounts and serves as the fiduciary for portfolio assignment and recommendations on savings rates and retirement age. Participants use a “single sign-on” to enroll in the plan and the managed account.

Voya has already launched the adviser managed accounts program with advisory firms CBIZ Investment Advisory Services LLC, and Resources Investment Advisors – A OneDigital Company. As the program advances, Voya expects to work with additional RIAs.

A ‘longevity’ biotech SPAC

Shareholders of Longevity Acquisition Corporation (LOAC) have approved its merger with 4d pharma plc, a British biotech firm focused on Live Biotherapeutics (LBPs). In October 2020, 4d pharma announced its intention to merge with LOAC and seek a NASDAQ listing.

The merger and the NASDAQ listing of 4d pharma American Depositary Shares (ADSs) under the ticker symbol ‘LBPS’ are expected to become effective in early 2021, subject to approval of 4d shareholders and Longevity shareholders, and the SEC review process.

LOAC, a “blank check” or Special Purpose Acquisition Company (SPAC), is sponsored by Whale Management Corporation, a Bermuda-based LLC. 4d pharma develops LBPs, a class of drugs that contain a live organism, such as a bacterium, that is applicable to the prevention, treatment or cure of a disease.

4D has developed a proprietary platform, MicroRx, that “rationally identifies LBPs based on a deep understanding of function and mechanism,” according to a release. 4d pharma’s LBPs are orally delivered single strains of bacteria that are naturally found in the healthy human gut.

The company has six clinical treatment programs underway, for cancer, Irritable Bowel Syndrome, COVID-19, Parkinson’s disease and other maladies. It has a research collaboration with MSD, a trade name of Merck & Co., Inc., Kenilworth, NJ, to discover and develop LBPs for vaccines.

© 2021 RIJ Publishing LLC. All rights reserved.