While Prudential Financial’s history dates to 1875, the Newark, NJ-based insurance and asset management firm has changed dramatically in recent years. After demutualizing in 2001, the firm acquired American Skandia’s variable annuity business, then CIGNA’s retirement plan business, then Hartford’s life insurance business, among other changes.

During the variable annuity arms race of the 2000s, Prudential regularly topped the variable annuity sales charts with its flashy Highest Daily income guarantee. The product came through the financial crisis relatively unscathed, thanks to a self-protective risk management method. Prudential has also been a prolific advertiser, notably for its longevity-awareness TV campaign with Harvard’s Dan Gilbert.

Within the last five years, Prudential has pivoted to new initiatives in global pension risk transfers, financial wellness programs for retirement plan participants, and a global wealth management business. It has launched new individual annuities, such as the PDI (Prudential Defined Income) variable annuity, the PruSecure and SurePath index annuities, and the GIFT (Guaranteed Income for Tomorrow) multi-premium deferred income annuity.

Kent Sluyter, an actuary and 28-year Prudential veteran who became president of Prudential Annuities in 2017, recently spoke with RIJ at length about annuities, financial wellness, and more. Here’s a condensed transcript of the conversation.

Sluyter.

RIJ: Financial wellness is a big topic among retirement plan providers today. Prudential has added financial wellness and financial education programs to its menu of services for retirement plan sponsors, and published white papers about the importance of financial wellness programs. What’s the business reason for developing and marketing these programs?

Sluyter: From a business perspective, there’s a near-term, medium-term, and long-term driver of financial wellness programs. At the near-term, they increase our ability to win and retain institutional clients in the retirement and group insurance space.

RIJ: I see. So it helps you compete against other plan providers.

Sluyter: Yes. In the intermediate-term, we believe that our engagement with those employees will increase their utilization of our retirement savings and other benefits. Participants increase their contributions to 401(k) plans when they’re more educated about the benefits of saving. And the participants often feel less stress and have higher productivity.

RIJ: So financial wellness helps you build assets under management. And what would be the long-term benefit?

Sluyter: The third benefit for us, in the long-term, is that we can provide those individuals with retail solutions, beyond the worksite benefits. We can drive a deeper relationship with them and offer them different solutions. Winning rollovers would be an element of that long-term strategy. Financial wellness is also an opportunity to sell life insurance, in a way that reaches more individuals than will ever talk to an advisor. It’s primarily an avenue for selling more life insurance, but I wouldn’t rule out the income side.

RIJ: What does financial wellness cost the plan sponsor? Plan sponsors are said to be hungry for data that these programs pay off for them.

Sluyter: Financial wellness programs are not an added cost.

RIJ: Now, within, or in addition to financial wellness, you have a financial education program called Prudential Pathways, right?

Sluyter: Today, we serve about five million individual customers through our advisory channels. Prudential’s existing financial wellness offerings, including the company’s digital financial wellness platform, has been deployed to more than seven million individuals across more than 3,000 organizations.

Prudential Pathways, our on-site financial education program, has been adopted by nearly 600 employers. It’s a natural pipeline for us to reach an added 20 million people that we wouldn’t have the capacity to reach through 3,000 advisors. It is also a powerful retention tool and source of qualified lead generation for Prudential Advisors, and because of the access to new retail customers that the program offers, we’ve also been able to attract a meaningful number of experienced financial advisors to Prudential.

RIJ: Are you watching the progress of the SECURE Act/RESA closely? If they become law, and it becomes safer, from a liability standpoint, for plan sponsors to embed almost any type of annuities into their plan, would that be a game changer for Prudential?

Sluyter: As you have seen, there’s also a potential for greater in-plan guaranteed income solutions. Some of the bills and proposals in Washington are creating awareness of that. But that will take a little bit longer.

RIJ: So, from the provider’s perspective, financial wellness can generate new and higher revenues. But do ‘grownup’ employees actually need assistance with their household finances?

Sluyter: There are individuals who are struggling. We’ve seen the data on debt. We’re helping people manage through that debt to a better situation. There’s also a sizable segment that is saving but not sure they are doing the right thing. Our data shows that almost half of people 55 and over give themselves a ‘C’ for financial literacy.

RIJ: But people are deluged with financial information all the time, aren’t they?

Sluyter: Despite today’s information overload, there’s a real gap with respect to the amount of knowledge people have about saving for retirement. A sizable population is trying to save. But there is not an equally sizable number who reach retirement having saved enough. We’re trying to help those who are struggling, or who are in ‘the middle of the pack,’ as well as those who have done a good job saving.

The solution might be as simple as managing day-to-day finances better. Or, if the opportunity is there to consider both options, it could mean helping people decide whether to stay in their plan or capture a rollover. It’s hard to say where things are headed.

RIJ: We reported recently that Prudential has introduced its first fixed indexed annuity, or its first one in many years. What are your plans for that product line?

Sluyter: We are relatively new to that space. We launched our first one last year, PruSecure, and we’ve gotten traction in the IBD (independent broker dealer) channel. That’s a commission-based product. We just launched an additional product this week in the IMO (insurance marketing organization) channel, SurePath, which has GLWB (guaranteed lifetime withdrawal benefits) capability.

We recognize that about half of FIA sales are in the IMO channel. FIAs represent only about 10% of our annuity sales now. But, given where the market seems to be going, we see fixed annuity sales growing more than variable sales.

On the variable side, business hasn’t changed much. Sixty to 70 percent is GLWB. The IMOs make greater use of the GLWB than the banks or the wirehouses. I would like to see that start to grow.

RIJ: Many annuities are looking toward the RIA channel and fee-based advisors in general for ‘blue ocean’ growth. Do you plan to create a no-commission FIA, perhaps to put on the DPL Financial Partners or RetireOne platforms, where RIAs without insurance licenses can buy FIAs?

Sluyter: We are not on either the DPL Financial or the RetireOne platforms. We’ve been focused on the Envestnet Insurance Exchange. We expect to see that develop. Nobody has begun doing business there yet.

RIJ: Do you see the RIA market as having potential for annuities? The data that I’ve seen from a Practical Perspectives report shows only a handful of RIAs saying they recommend annuities to their clients.

Sluyter: It’s hard to get a good number on the percentage of RIAs recommending annuities. It might be larger than the raw data might suggest. We think as many as 40% of RIAs are recommending life insurance or annuities to clients. The technology is a critical element for this to work. It’s absolutely where we need to be. Envestnet is closing that gap with its Insurance Exchange.

RIJ: What’s required to convert RIAs to annuities?

Sluyter: It’s more than a matter of ‘if we built it they will come.’ The insurance carriers need to speak the language of RIAs. We must engage with how they look at the world. We think of our obligation to RIAs in four quadrants: product solution, technology, engagement, and fee withdrawals.

We have a fee-based product on the market, and we are working on new product designs that will be launched later this year. They’re intended to be responsive to what RIAs are looking for. That includes the kind of transparency they want. It’s still a work in progress. There’s a simplicity aspect to that. We also have to provide them with the type of investments they’re familiar with, like low-cost institutional share classes. We have to make it easer for them to handle fee withdrawal management.

RIJ: What kind of income solution would you pitch to RIAs?

Sluyter: It could involve some longer-term solutions, like the CDA [contingent deferred annuity] longevity wrap products. We might potentially go back to that kind of stand-alone living benefit solution. There’s technology that makes that possible. We could see a resurgence in those ideas. It’s not a new idea, but its time may be coming closer.

RIJ: CDAs are essentially GLWBs, though, and the number of annuity owners opting for the GLWB rider has been declining for several years, right?

Sluyter: The GLWB has become less in favor. That’s occurring at a time when returns are strong. It’s natural for advisors to look more to accumulation, and not feel the need to lock in the gains with guaranteed products. In a more uncertain time, maybe that would be different. I think we’re seeing more advisors thinking about taking some of the money off the table.

So it remains to be seen what will happen with the GLWB. That might come back into favor. The industry sold the most variable annuities right after the market crashed. Given the run up in equity prices in the last 10 years, advisors should be looking at taking some of that off the table. That’s one of the drivers in the sale of FIAs. The RIA channel might not be the first place where that will show up.

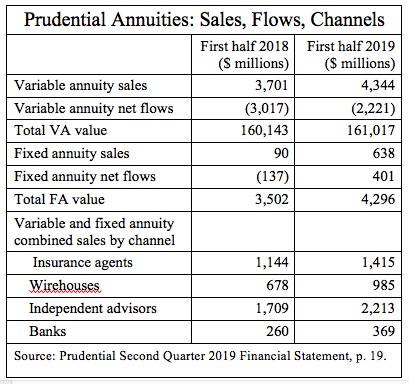

RIJ: Speaking of variable annuities, a lot of insurers have had trouble managing their VA blocks of business since the Great Financial Crisis. Contract owner behavior with regard to using living benefits is hard to predict. Is that the case with Prudential? Your VA block is worth about $161 billion, as of June 30, 2019.

Sluyter: We are actually very happy with our in-force block of variable annuities. That’s not a universal sentiment in this industry. Our in-force block is performing well.

RIJ: As I understand it, Prudential’s individual variable annuities with living benefits were the only products of that type to use something like the Constant Proportion Portfolio Insurance (CPPI) risk management technique. It allowed Prudential to use an automatic, algorithm-driven asset allocation process by which policyholders’ portfolios are rebalanced into safer assets when the account value starts falling below the amount needed to cover the guarantee. As I understand it, that methodology has protected Prudential’s ability to meet its obligations when stocks drop.

Sluyter: We feel that we’ve taken the right steps to manage and hedge that risk. We continue to use the same techniques as in the past. We are using even more sophisticated techniques to drive down volatility. From a capital standpoint, we continue to manage that system the way you described, but we do not refer to the algorithm as a CPPI strategy, because it works a little bit differently from pure CPPI. We officially refer to the algorithm as the “predetermined mathematical formula.” The key driver of the predetermined mathematical formula in our product is the spread between the guarantee, or “Protected Withdrawal Value,” and the account value. Transfers could happen even if sub-accounts are growing, but not keeping pace with the guarantee.

RIJ: What’s your top VA product today?

Sluyter: A fairly significant part of our VA growth has come from our Prudential Defined Income (PDI), where the subaccounts only hold bonds. It responds to the “income now” market [as opposed to the deferred income or “income later” market served by GLWBs with deferral bonuses]. PDI has grown significantly in popularity and now accounts for about half of our VA sales.

RIJ: With respect to distribution, a certain portion of Prudential annuity sales still goes through your career agent force, right?

Sluyter: We do have a captive force. About 25% of our annuity sales come thorough our captive agents, the Prudential Advisors. They sell the same products that we sell though third parties. But as we get into the IMO [insurance marketing organization] space and develop products for the RIA channel, we’re headed for customization. We’ll customize either by distribution channel or on a client-by-client basis.

RIJ: Could you tell us something about Prudential’s “Guaranteed Income for Tomorrow,” or GIFT program. It’s a flexible premium deferred income annuity, right, delivered partly or mostly over the Internet?

Sluyter: Yes, GIFT involves contributing small amounts every month to build income at retirement. We’re still learning how to engage individuals, and how to present information around guaranteed income concepts. It sounds easy, but it’s difficult. We’ve gone through multiple iterations. GIFT was intended to be an all-digital consumer channel. But we’ve found that very few consumers are comfortable making an annuity purchase decision until they talk to an advisor. The industry is not at a point where people can just click and buy an annuity. That’s been a learning experience for us.

RIJ: So how will you deliver the service?

Sluyter: Right now we’re looking at the “omni-channel” model. We provide web-based education and, once people educate themselves, they can pivot to a live advisor. The advisor and client could have an online conversation or a live, face-to-face meeting. Or people could engage face-to-face and then go digital.

RIJ: Who’s the target audience for GIFT?

Sluyter: We offer GIFT through institutions and through associations. We have benefit plans with professional associations, and those associations can provide it as a service to their members. It’s directly available on prudential.com. Also, as advisors migrate up the wealth scale, they’re leaving a large segment of the population without advice. GIFT fits that underserved population. We are passionate about reaching the underserved.

RIJ: Thank you, Kent.

© 2019 RIJ Publishing LLC. All rights reserved.