The economies of “pooling” are non-trivial. Whether it’s car-pooling with co-workers, buying life annuities, or joining an old-fashioned community “swim club,” the efficiencies that come from sharing an expense, a chore or a risk can deliver significant individual savings.

But pooling brings frictions and complexities as well. That’s why many people choose to install their own backyard swimming pools, avoid illiquid annuities, and commute solo to work every day.

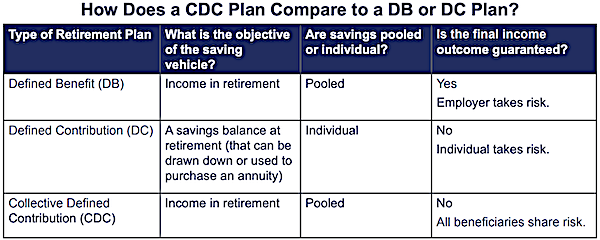

Which brings us to the concept of “collective defined contribution” or CDC plans. A timely new white paper from the Center for Retirement Initiatives at Georgetown University makes a case for these retirement plans, which try to blend elements of defined benefit pensions and of defined contribution plans in a best-of-both-worlds hybrid.

“A CDC plan is similar to a DB plan, but does not provide a guaranty from the employer,” write Charles E. F. Millard, David Pitt-Watson, and CRI executive director Angela M. Antonelli in “Securing a Reliable Income in Retirement.” They contribute to the ongoing debate over how best to help DC plan participants turn their tax-deferred savings into reliable income.

Like a DB plan, a CDC plan is overseen by a professional investment management team with the goal of paying participants an annual retirement income equal to a percentage of their final or average pay. The white paper describes the potential benefits and avoidable pitfalls of using CDC, and highlights lessons learned from CDC experiments in the Netherlands and the United Kingdom.

Ultimately, the authors favor CDC. “Recent studies suggest that a CDC plan will generate a retirement income at least 30% higher than a typical DC plan,” they write. “Recent reforms in the United States offer a potential new opportunity for the greater adoption of pooling, the introduction of CDC plans, and other future plan design considerations for policymakers.”

© 2021 RIJ Publishing LLC. All rights reserved.