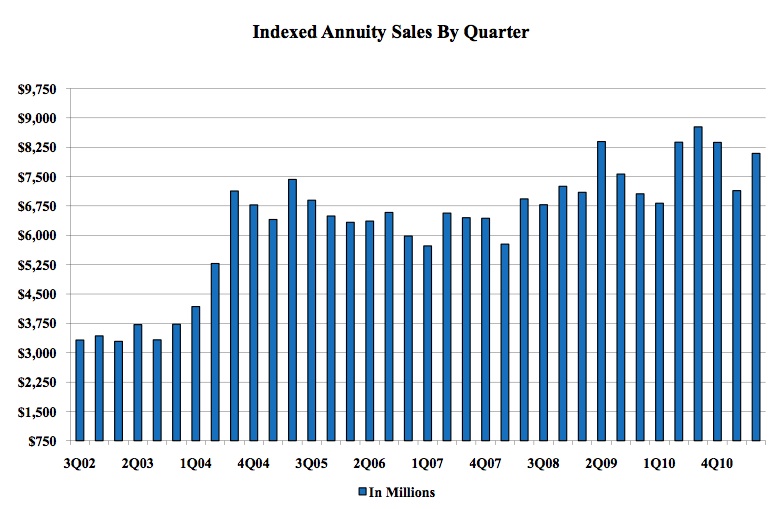

New rate-sensitive crediting strategy for ING FIAs

To calm fears among fixed-income investors about the potential for interest-rate hikes, ING USA Annuity and Life Insurance Company (ING USA) has introduced a new crediting method called Interest Rate Benchmark Strategy for its indexed annuities.

During each annuity contract year, any increase in the 3-Month LIBOR Interest Rate will be multiplied by a predetermined factor (the Interest Rate Benchmark Participation Multiplier) and credited to the contract, up to a stated cap. If rates remain the same or fall, there will be a floor of zero crediting.

The Interest Rate Benchmark Credit Cap and Interest Rate Benchmark Participation Multiplier are declared in advance, guaranteed for one year, and may change annually for each contract. This strategy tends to credit more interest than other indexed or fixed-rate strategies during a period when interest rates are rising.

“Many consumers are parking their long-term money in short-term savings vehicles because they’re paralyzed by the current rate environment. This new crediting strategy addresses the concerns about low rates and the possibility that they will rise in the near future,” said Chad Tope, president of ING Annuity and Asset Sales at ING.

With the addition of the ING Interest Rate Benchmark Strategy, the ING Secure Indexed Annuity platform now offers three core ways for consumers to pursue an interest crediting strategy. The new strategy will complement existing indexed strategies and fixed-rate crediting strategy available on the products.

Annuities are issued by ING USA Annuity and Life Insurance Company (Des Moines, IA), member of the ING family of companies. ING Annuity and Asset Sales is a department name within ING’s U.S. operations.

Stock funds lost assets in July; stock ETFs and bond funds grew: Strategic Insight

U.S mutual fund investors sold about $23 billion in stock mutual fund shares and bought about $8.4 billion worth of bond mutual fund shares in July, for a net outflow of about $16 billion, or 0.2%, from combined US stock and bond mutual funds in July 2011 (in open-end and closed-end mutual funds, excluding ETFs and funds underlying variable annuities) according to Strategic Insight.

The sharp decline of stock prices in early August incited further redemptions. In the first week of August, SI estimates that stock fund net redemptions equaled about 0.3% of the more than $6 trillion held in equity funds. The dramatic volatility this past week may have resulted in further stock fund net withdrawals of about 0.5% of stock fund assets.

International/global equity funds saw net outflows of nearly $1 billion. Money-market funds saw net outflows of $113 billion in July. This represented a widening of outflows from June, when money funds saw net outflows of $44 billion.

These tiny ratios are reassuring, and are in line with historical redemption patterns studied by SI over the past 20 years and before, according to SI.

“While some short-term redemptions from equity mutual funds during recent weeks and possibly in coming ones are likely, Strategic Insight’s research has shown that redemption spikes after stock market price declines have historically been limited in scope and short-lived,” said Avi Nachmany, SI’s Director of Research.

July’s bond mutual fund inflows were fueled by demand for global and emerging markets bonds, as investors continued to search for low-risk alternatives to low-yielding cash vehicles.

Through the first seven months of 2011, bond funds saw net inflows of $77 billion, a healthy pace if off 2010’s pace. Strategic Insight expects demand for select bond funds to persist as long as near-zero yields on cash investments and stock market anxieties continue.

Strategic Insight said U.S. exchange-traded funds (ETFs) in July experienced roughly $15 billion in net inflows. Through the first seven months of 2011, ETFs (including exchange-traded notes, or ETNs) saw net inflows of $68.5 billion. At the end of July 2011, U.S. ETF assets stood at $1.104 trillion.

Insider buying at three-year high: TrimTabs

TrimTabs Investment Research reports that buying by corporate insiders has picked up dramatically as stock prices have swooned.

Based on the latest filings of Form 4 with the Securities and Exchange Commission, insiders have bought $861 million so far in August. Insider buying this month is running at the fastest pace since May 2008, and insider buying this month is already higher than in any other month this year.

TrimTabs regards the pickup in insider buying as a bullish sign. Since insiders know more about their companies’ prospects than anyone else, it is positive that insiders are putting some of their own cash to work in the market.

But TrimTabs cautions that insiders are not infallible. Insiders were also buying heavily in late 2007 and early 2008, right before the financial crisis intensified.

Great-West Retirement Services establishes fee-disclosure template

Great-West Retirement Services has created a disclosure template that it says provides plan sponsors even more information about its services, fees and expenses than will be mandated by the Department of Labor’s 408(b)(2) disclosure regulation, whose compliance deadline is next year, the company said in a release.

“We combined almost all fee disclosure information into a single, comprehensive document, and even disclosed certain fees not required by the new regulation,” said Charlie Nelson, president of Great-West Retirement Services, the fourth largest retirement recordkeeper in the U.S., by number of participant accounts, according to Pensions & Investments.

The company is a subsidiary of Great-West Life and Annuity Insurance Co., which is a unit of Great-West Lifeco Inc., which is part of the Canada-based Power Corp. Great-West Retirement Services provided 401(k), 401(a), 403(b) and 457 retirement plan services to 25,000 plans representing 4.5 million participant accounts and $155 billion in assets at June 30, 2011.

“We surpassed other requirements as well,” Nelson added. For example, the regulation doesn’t require a service provider to show fees in dollars and percentages instead of formulas; however, we provide our disclosure in both dollars and percentages. We also provide a summary of fees as well as a detailed breakdown by category.”

The template provides third-party certification from DALBAR, Inc., that it complies with the regulation, Nelson said. A sample template is available upon request by emailing [email protected].

Brinker Capital Taps Bill Simon to Head Retirement Plan Services Group

William P. Simon, Jr. has joined Brinker Capital, an investment management firm, in the new position of managing director, Retirement Plan Services. Simon will also serve on Brinker Capital’s Operating Committee. He reports to Brinker Capital President, John Coyne.

Before joining Brinker Capital, Simon served as Managing Partner at PPB Advisors LLC. Previously, he spent 22 years at American Funds, initially as a mutual fund wholesaler. Between 2003 and 2009, he held a variety of senior positions. He also held positions at Van Kampen Merritt and with Federated Investors, where he began his career.

In June, Brinker Capital, based in Philadelphia, added seven ETF strategies to its Defined Contribution retirement plan offering.

In another personnel move, Brinker Capital announced that Paul Cook has joined the firm as Regional Director in the Retirement Plan Services Group. He will help to build new advisor relationships, expand the scope of existing advisor relationships, and introduce new tools and services to existing advisors.

Cook comes to Brinker Capital with experience in retirement plans from his roles at Vanguard, SEI, USI, Stancorp Equities, Bisys, and Valley Forge Asset Management. He holds a BA in marketing from Penn State.

Downgrade of U.S. debt sparks expansion at compliance consulting firm

FrontLine Compliance LLC, a regulatory compliance consulting firm, has expanded its customized investment guideline review service for large money managers following the U.S. debt downgrade issued by Standard & Poor’s on August 5.

“Investment advisers will have to conduct an inventory of all advisory accounts invested in U.S. debt,” says Amy Lynch, president and founder of FrontLine Compliance and a former SEC regulator. “This is especially important for institutional managers to large entities that typically have strict investment guidelines regarding the quality of fixed income investments.”

FrontLine Compliance offers experienced trading compliance experts that have conducted numerous investment guideline reviews for many large money managers. This type of review is typically outsourced because it is very labor intensive to review all of the related account level documentation against the transactions and holdings.

“The prudent manager should assess account holdings against investment guidelines as stated in client agreements or policy statements,” says Lynch. “It’s common practice for large pensions, foundations, and endowments to restrict debt holdings to AAA rated only. Unfortunately, due to the recent downgrade, an account with this restriction could be out of compliance if it holds long-term U.S. debt.”

In order to comply with Section 206 of the Investment Advisers Act of 1940 investment advisers must follow client investment objectives and guidelines.

New John Hancock RPS website serves plan sponsors, consultants, et al

John Hancock Retirement Plan Services (RPS) has introduced the John Hancock Education Resource Center, a website and materials ordering portal, designed to help plan sponsors, plan consultants and financial representatives educate and motivate employees about planning for retirement.

“We’ve given all of our 47,000+ plan sponsors, as well as the plan consultants and financial representatives that we work with, an easy and intuitive way to deploy a comprehensive education and communications campaign to help employees get ready for retirement,” said Andrew Ross, senior vice president of marketing, John Hancock RPS.

The site provides:

- A Solution Center which helps the user leverage the appropriate education programs and communications to suit their specific needs

- A wealth of employee paper based and electronic materials and tools on retirement, investing, the elements of retirement plans and planning for retirement

- The ability to easily browse materials by life stage or by communications type

- The option to choose various methods of communication such as brochures, online education tools, seminars, and posters

- Instant access to the materials

RIJ spoke with Walter (right) and one of his associates, Alexandra Orozco, at their offices in Guatemala City by Skype telephone earlier this summer. In September, Redcamif will begin its pilot micro-pension project, hoping to enroll 12,500 people in three years.

RIJ spoke with Walter (right) and one of his associates, Alexandra Orozco, at their offices in Guatemala City by Skype telephone earlier this summer. In September, Redcamif will begin its pilot micro-pension project, hoping to enroll 12,500 people in three years.