Data Connection

IssueM Articles

“Regulatory arbitrage” has been cited by RIJ and others as a reason for the use of Bermuda reinsurance private equity-led U.S. life/annuity companies. But what does that jargonish expression mean in this context? Indeed, it would take an expert in international accounting rules to explain it accurately.

Moody’s does the necessary explaining in “Regulation contributes to material differences in private credit allocation,” one of the ratings agency’s Sector-in-Depth reports, published in May. The report is essential reading for anyone trying to understand the offshore leg of the “Bermuda Triangle” strategy.

“To highlight how variations in regulatory capital requirements and reserve calculations play a role in shaping life insurers’ investment choices,” Moody’s analysts compared and contrasted regulatory capital regimes in the U.S., Bermuda, Europe and Japan, as well as U.S. life insurers’ investment portfolio allocations in each jurisdiction.

Moody’s report clarifies the link between cross-border accounting maneuvers and life insurers’ investments in risky private assets. U.S. accounting rules, with their higher risk-related capital requirements, can make it uneconomical for private equity-led insurers to hold as much illiquid, opaque, customized, and high-yielding assets as they hope to. “whose regulatory treatment is unclear.”

“The development of new investment vehicles whose regulatory treatment is unclear, along with a release of capital under certain transactions as insurers transfer assets and liabilities among various jurisdictions, notably from the US to Bermuda, are pushing regulators to increase their scrutiny of reinsurance transactions and private credit assets,” the report said.

Moody’s notes that the accounting “regime in Bermuda tends to allow for a higher discount rate than other jurisdictions” and that this “directly impacts the level of liabilities and therefore an insurer’s level of available capital (the difference between the value of an insurer’s assets and the value of its liabilities). The more insurers can discount their liabilities, the stronger their solvency ratios are.” The unanswered question: Are they stronger in fact or only on paper?

“US life insurers have been increasing their allocation to private credit, an evolving asset class that includes private corporate lending, notably to middle-market companies owned by private equity. Private credit also includes various types of private financing, such as real estate and infrastructure projects, as well as private loans against a vast array of assets that can be grouped under the term asset-backed finance (ABF),” the report said.

“As of year-end 2022, U.S. life insurers held more than $4.5 trillion in total cash and invested assets in their general accounts, of which at least $1.5 trillion (35%) was invested in illiquid and private assets. These assets are concentrated in mortgages (17%) and securitized assets (16%), with noticeable growth in collateralized loan obligations (CLOs), which represent between 3%-4% of total cash and invested assets.”

On the one hand, regulatory arbitrage reduces capital requirements, giving life insurers “improved capital efficiency.” But in the process it can raise the degree of leverage in the insurance business, making it systemically more sensitive to a downturn in asset prices or a credit crunch. Moody’s report shows that both the NAIC in the US and the Bermuda Monetary Authority have written revised regulations that take effect this year. RIJ will report on those changes in future articles.

Moody’s defines private credit as:

“Non-bank lending to mostly private-equity owned, middle market companies that are not publicly traded or issued. This can be distressed or opportunistic and is typically below investment grade. For insurers, these asset classes form the minority of private fixed income investments.

“Our definition also includes significant exposure to classes such as real estate, including commercial mortgage loans, and infrastructure lending and private placements with corporate [bonds], which are typically investment grade and where most insurers invest, and other asset-based finance. Private credit offers incremental return, often referred to as ‘illiquidity premium,’ over equivalent publicly traded assets which have additional liquidity and market transparency.”

© 2024 RIJ Publishing LLC. All rights reserved.

When we talk or write about embedding payout options in 401(k) plans—annuities, systematic withdrawal processes, etc.—the role of recordkeepers doesn’t always get as much attention as the roles of plan sponsors, plan advisers, life/annuity companies, asset managers or participants.

There are a couple of reasons for that. Plan recordkeeping is a back-office or middle-office service, ideally as invisible as America’s electrical grid or its interstate pipeline system. Some recordkeepers are also full-service plan providers; keeping track of data is only part of what they do.

But the savings-to-income revolution in the 401(k) industry that the SECURE Acts of 2019 and 2022 prodded forward, and for which many financial and fintech companies have geared up, depends in part on the ability of the recordkeepers to support it.

The Retirement Research Center of the Defined Contribution Institutional Investment Association (DCIIA), a Washington, DC-based trade group, recently conducted a survey of recordkeepers to measure their progress toward facilitating income options in 401(k) plans.

The results of the recently-published survey showed that:

Regarding recordkeepers’ future plans to accommodate “in-plan guaranteed solutions” (i.e., annuities to which participants contribute while working), the survey showed that:

With respect to non-guaranteed income solutions, such as systematic or ad hoc withdrawal plans, the survey showed that:

© 2024 RIJ Publishing LLC. All rights reserved.

There are non-insurance alternatives to fixed indexed annuities (FIAs) as savings vehicles For cautious who want to eliminate all risk of investment loss on part of their portfolio but fear “missing-out” on a stock market rally, there’s a non-insurance solution.

So-called “structured ETFs” deliver “protected growth” through the purchase of a bracket of options on an equity index that’s stripped of its dividend yield, such as the S&P 500 Price Index. (The cost of options on price indexes is less than the cost of options on total return indexes).

The Calamos Structured Protection ETFs suite from Calamos Investments claims to do that. The one-year contract issued on May 1, 2024 provided 100% principal protection and a maximum credited interest of 9.81% at the end of the term, less a 0.69% expense ratio.

The options strategy of a structured ETF works a bit differently from the options strategy of an FIA. When building an FIA, a life/annuity insurance company invests most of a client’s principal in the company’s general account; it uses only about 4% of principal (depending on prevailing corporate bond rates and other factors) to buy options on an equity index.

With the Calamos structured ETF, most of the client’s principal goes to the purchase of options on the S&P 500 Price Index. The options strategy has three steps:

Calamos claims that saving with its Structured Protection ETFs is more tax-efficient than saving with FIAs. While FIA gains are subject to ordinary income tax (up to 37%) when withdrawn, gains on one-year structured ETFs are taxed at long-term capital gains tax rates (up to 20%).

ETFs are also more liquid than FIAs; are not subject to counterparty risk; have explicit, transparent pricing; have no investment minimums are price and are generally easier to trade and incorporate into a portfolio, according to Calamos.

© 2024 RIJ Publishing LLC. All rights reserved.

Micruity, a Toronto-based fintech, said it has expanded its collaboration with MetLife, Inc., which offers the MetLife Guaranteed Income Program and MetLife Retirement Income Insurance QLAC to defined contribution retirement plan participants.

The two firms have already worked together on connecting MetLife’s retirement income services with Fidelity’s Guaranteed Income Direct and State Street Global Advisors IncomeWise platforms.

A provider of technology for data-sharing between asset managers, life insurance and retirement plan recordkeepers, Micruity will help MetLife develop its Universal Digital Retirement Platform. The platform is an education, planning, and annuity purchasing tool that connects to existing employment benefit, third party administrator (TPA) and recordkeeping systems.

The new tool will help plan sponsors offer “educational resources on a broad range of retirement income-related topics… and expand access to immediate income annuities, allowing plan sponsors to easily offer these solutions within their defined contribution (DC) plans,” a Micruity release said.

MetLife’s 2024 Qualifying Longevity Annuity Contract Poll found that 91% of plan sponsors are concerned that future retirees will run out of money in their retirement.

“The Micruity Advanced Routing System (MARS) facilitates frictionless data sharing between Life Insurers, Asset Managers, and Recordkeepers through a single point of service that significantly lowers the administrative burden for plan sponsors and enables them to turn retirement savings plans into retirement income plans at scale,” the release said.

Micruity also announced that it closed $5 million in funding to expand support for accumulation annuities and non-guaranteed income products on the Micruity platform.

The round includes new funding from strategic investors Prudential, State Street Global Advisors, and TIAA Ventures, as well as additional investments from current partners Pacific Life and Western & Southern Financial Group. In total Micruity has raised over $11M from strategic partners in the retirement industry.

“The new funding enables Micruity to rapidly build out infrastructure not just for retirees in the drawdown phase of their retirement journey but also provide critical support for younger Americans still saving for retirement,” said Trevor Gary, Founder and CEO of Micruity.

“Successive financial crises have eroded the retirement savings of many Americans who now face the prospect of outliving their savings. By building the infrastructure necessary to enhance the user experience of both guaranteed and non-guaranteed income products, Micruity, along with our partners, can help close this gap and deliver a safe and secure retirement,” added Gary.

A recent US Retirement Survey found that non-retired Americans aged 27 to 42 face an average shortfall of $403,626 in their retirement savings. For Americans aged 43 to 58, that gap grows to $451,170.

The Micruity platform connects Recordkeepers, Life Insurers, and Asset Managers through a single secure connection, reducing the administrative burden of managing multiple products across several plans while delivering targeted savings and income solutions.

© 2024 RIJ Publishing LLC. All rights reserved.

The Department of Labor has decided not to shake up the regulatory foundation of the “pension risk transfer” (PRT) business—the replacement of defined benefit pensions by group annuities issued by life insurers—by amending its 30-year-old Interpretative Bulletin 95-1.

IB 95-1 requires retirement plan fiduciaries, among other guidelines, to choose the “safest available” annuity for plan participants. The life/annuity industry has changed enough since the bulletin was written, some observers claim, to warrant an update in its text.

The DOL’s Employee Benefit Security Administration (EBSA), said in a June 24 report to Congress, however, that it “is not prepared at this time to propose amendments to the Interpretive Bulletin to address [the] potential risk” posed by what RIJ has called “the Bermuda Triangle strategy.”

But the report conceded that “EBSA has not concluded that changes to the Interpretive Bulletin are unwarranted.” It explained why:

“Some stakeholders are very concerned about developments in the life insurance industry that may impact insurers’ claims-paying ability and creditworthiness. As set forth above, some stakeholders urged EBSA to update the Interpretive Bulletin to focus fiduciaries’ attention on issues such as insurers’ ownership structures; exposure to risky assets and non-traditional liabilities; and use of affiliated and offshore reinsurance.” [Emphasis added.]

The writers of the report referenced the growing ownership of life/annuity companies by holding companies controlled by “private equity” or “buyout” or “alternative asset managers,” the relatively heavy purchase of risky private assets and structured securities by those life/annuity companies, and use of reinsurance for the purpose of reducing surplus requirements. This the phenomenon identified by RIJ as the Bermuda Triangle.

For an RIJ story on an August 2023 meeting of the ERISA Advisory Council that helped inform the new DOL report, click here.

The new report happens to emerge amid class action lawsuits against AT&T and Lockheed Martin this spring for swapping their DB plans for a group annuities issued by Athene Annuity & Life, an affiliate of Apollo Global Management. The suit accuses AT&T and Lockheed Martin of failing to choose the “safest available annuity” for its DB plan participants when it chose Athene, as IB 95-1 requires.

The report does however give considerable space to the concerns expressed about private equity controlled life/annuity companies:

“Some stakeholders attributed concerning developments in these areas to private equity firms’ increased involvement in the industry. They said that private equity-affiliated insurers tend to engage in riskier practices than traditional insurers. Stakeholders were also concerned that private equity firms do not have a long track record of managing life insurance obligations and may lack a commitment to policyholder interests.

However, others say the concerning practices are employed on a more widespread basis in the industry. EBSA is not prepared at this time to propose amendments to the Interpretive Bulletin to address this area of potential risk. The issues raised by stakeholders are complex and there were few, if any, areas of consensus. As just one example of this, six ERISA Advisory Council members supported no changes to the Interpretive Bulletin, while the other nine members supported different positions on different issues.”

History is especially relevant here. As the June 24 DOL report points out, IB-95 was issued in response to the 1991 failure of First Executive Corporation, its Executive Life Insurance Company and a subsidiary, ELIC of New York. FEC and ELIC failed because in part because they were doing what the private equity-led life/annuity companies are doing now.

ELIC was selling fixed deferred annuities, buying large amounts of risky assets (Michael Milken’s junk bonds), and buying Bermuda reinsurance for “surplus relief.” ELIC was also in the PRT business—sometimes selling group annuities to companies that Milken had acquired through leveraged buyouts.

The interpretation evidently hasn’t prevented the recurrence of the same life insurer practices—holding high-risk assets, dealing with its own affiliates instead of third-parties, and buying reinsurance from an affiliate—that it was written to eliminate.

Moreover, the National Association of Insurance Commissioners (NAIC) itself created Risk-Based Capital rules in the 1990s after the ELIC bankruptcy, and those rules have not prevented the return of the strategy (Bermuda Triangle) that they were intended to eliminate.

The new report also reflects the fact that the DOL is caught between the NAIC and, on the other hand, the Senate Banking Committee, led by Sen. Sherrod Brown, and the Treasury Department’s Federal Insurance Office, a creation of the Dodd-Frank financial regulation.

In 2022, Brown’s committee and the FIO both sent letters to the NAIC expressing concern about potential misuses of insurance regulations and principles by private equity companies that have bought life/annuity companies in order to manage or control the assets backing their guarantees to policyholders. One of those misuses involves offshore affiliated reinsurance.

The DOL report acknowledged the concern about reinsurance:

“A number of stakeholders raised concerns that life insurers are using reinsurance to move liabilities to less regulated reinsurers. They mentioned less stringent reserving requirements and accounting arbitrage as reasons for their concern… The Department of the Treasury noted in its letter that the speed and scale of the growth of offshore and affiliated reinsurance ‘suggests the need for regulators and policymakers to better understand the role of offshore reinsurers and whether regulatory capital arbitrage opportunities, tax advantages, and other potential gaps that are not under the oversight of U.S. regulators are obscuring (or even amplifying) the level of risk stemming from these activities.’”

But the NAIC has not welcomed the attention of those federal entities, while doing little to slow down the expansion of the Bermuda Triangle strategy—even in the face of alarms sounded in the 2010s by academic economists, economists at the Federal Reserve, and in 2023tk by the International Monetary Fund.

© 2024 RIJ Publishing LLC. All rights reserved.

Nassau Financial Group, a fixed annuity issuer and asset manager, will receive a $200 million non-voting minority equity investment from Golub Capital, a direct lender and credit asset manager, the two companies announced last month.

Nassau and Golub Capital also will enter into a long-term Investment Management Agreement that will provide Nassau’s insurance subsidiaries with access to Golub Capital’s middle market direct lending strategies, through tailored capital-efficient solutions. The transaction is expected to close in the second half of 2024.

Nassau was in the news in May after a former subsidiary, PHL Variable Life, was deemed insolvent and taken into “rehabilitation” by the Connecticut insurance commission. In a 2021 restructuring, ownership of PHL Variable was “deconsolidated” from Nassau to Nassau’s majority shareholder, Golden Gate Capital.

Nassau was founded in 2015 with start-up and subsequent capital provided by Golden Gate Capital, Nassau’s majority controlling equity holder. It has since grown to $24 billion in assets under management and $1.6 billion in total adjusted capital. It had about 379,000 policies and contracts as of March 31, 2024.

Golub Capital will be the largest minority equity holder in Nassau. Fortress Investment Group invested in Nassau in 2023 and Wilton Reassurance Company and Stone Point Credit invested in 2021.

On the Golub transaction, Goldman Sachs served as Nassau’s exclusive financial adviser and Sidley Austin LLP served as its legal adviser. Morgan Stanley & Co. LLC served as exclusive financial adviser and Kirkland & Ellis and Foley Hoag as legal advisers to Golub Capital.

Nassau Asset Management oversees the assets of Nassau’s insurance companies and offers its specialty investment strategies to third-party clients. These strategies include public and private debt, collateralized loan obligations (CLO) debt and equity, real estate debt and equity, and alternatives.

AM Best has affirmed the Financial Strength Rating of A- (Excellent) and the Long-Term Issuer Credit Rating of “a-” (Excellent) of Aspida Life Insurance Company and Aspida Life Re Ltd. (Bermuda), collectively referred to as Aspida Group. The outlook of these Credit Ratings is stable.

The ratings reflect Aspida Group’s balance sheet strength, its adequate operating performance, neutral business profile and appropriate enterprise risk management, an AM Best release said. The stable outlooks reflect the expectation that Aspida Group will continue to receive capital infusions and financial resources of Ares Management Corp. and third-party investors.

Aspida Group is pursuing reinsurance growth through block acquisitions and flow reinsurance treaties and retail growth by expanding its distribution partners and its competitive annuity product suite. Ares Insurance Solutions (AIS), a unit of Ares dedicated to Aspida Group, has repositioned and deployed assets, focusing on structured credit in pursuit of wider interest rate spreads and higher yields.

AM Best said its outlooks also reflect the maintenance of an appropriate enterprise risk management framework. Operating trends are expected to remain positive over the near- to medium-term as management continues to focus on interest rate spread management.

The very strong balance sheet strength assessment considers Aspida Group’s risk-adjusted capitalization being at the strongest level, as measured by Best’s Capital Adequacy Ratio (BCAR), and AM Best’s expectation that Aspida Group will maintain similar levels of capital strength as the company executes its growth strategies.

Aspida Group had profitable adjusted operating income in 2023 and expects to continue to grow its operating income steadily driven by premium growth in both of its operating entities for the foreseeable future, the release said.

AM Best cautioned, however, that “Exposure to less liquid investments in Aspida Group’s general accounts are somewhat elevated compared with industry averages.” Aspida Group “does remain concentrated in interest-sensitive annuities, which currently account for all of its business… As with any newer organization, Aspida Group face execution risks, which are magnified by the increasingly competitive annuity market environment.”

Metropolitan Tower Life Insurance Co. has entered into a pension risk transfer (PRT) agreement with the 3M Employee Retirement Income Plan, a defined benefits plan worth about $2.5 billion, parent MetLife Inc. reported. A Metropolitan Tower group annuity will provide benefits to about 23,000 3M retirees and beneficiaries.

The group annuity contract was purchased from Metropolitan Tower Life Insurance Co. in June 2024, the release said. The 3M corporation’s retirees, retirees’ spouses and beneficiaries won’t see a change in the amounts of their monthly pension benefits.

Total U.S. pension risk transfer more than doubled in the first quarter, compared with the same period a year earlier, driven by so-called jumbo deals, according to the industry group LIMRA. PRT premium of $14.6 billion in the first quarter was 130% above 2023 figures, the group said in its U.S. Annuity Risk Transfer Sales Survey.

Metropolitan Tower and other MetLife underwriting entities have Best’s Financial Strength Ratings of A+ (Superior). Shares of MetLife Inc. (NYSE: MET) traded at $68.91 on the morning of June 17, up 0.53% from the previous close.

Apex Group Ltd. has received a $1.1 billion investment infusion from Carlyle’s Global Credit business and Goldman Sachs Private Credit, raising Apex’s “assets on platform” to about $3.1 trillion, “serviced across custody, administration, depositary and under management,” the global financial services provider reported June 24.

Carlyle and Goldman Sachs have committed to Holdco PIK Notes of Apex to continue to support the company’s focus on “optimizing the current platform, strategy and combined investment in technology innovation.”

Goldman Sachs Private Credit and Carlyle Global Credit purchased an initial Preferred Equity Note from Apex in 2020 and a follow-on issuance in 2021. Financial terms of the new investment were not disclosed.

Apex Group Ltd., established in Bermuda in 2003, provides financial services in 50 jurisdictions to asset managers, financial institutions, private clients, and family offices. The services include fund-raising solutions, fund administration, digital onboarding and bank accounts, depositary, custody, Super ManCo, corporate services, and an “ESG ratings and advisory” solution.

Carlyle (NASDAQ: CG) manages $425 billion (as of March 31, 2024) in private capital across three business segments: Global Private Equity, Global Credit and Global Investment Solutions. Goldman Sachs (NYSE: GS) manages more than $450 billion worldwide in alternative investments, including private equity, growth equity, private credit, real estate, infrastructure, sustainability, and hedge funds.

The alternative investments platform is part of Goldman Sachs Asset Management, which supervises more than $2.8 trillion in assets under supervision globally as of March 31, 2024. Established in 1996, the Private Credit unit at Goldman Sachs Alternatives manages $130 billion in assets across direct lending, mezzanine debt, hybrid capital and asset-based lending strategies.

According to the Corporate Finance Institute, a payment-in-kind or PIK loan allows borrowers to make interest payments in forms other than cash. It relieves the borrower of the burden of a cash repayment of interest until the loan term is ended. PIK loans are commonly used in leveraged buyout (LBO) transactions. In short, companies fund their liabilities with new liabilities.

Payment-in-kind loans (PIK) are usually issued by companies in poor financial condition that lack the cash to pay interest. The loans are purchased by lenders that don’t depend on the routine cash flow of the borrower as the repayment source of their investments. The payment of interest may be made by issuing another debt or by the issuance of stock options. At maturity or the refinancing of the loans, the borrower repays the original loan plus the PIK debt.

Though investing in a PIK loan offers higher yield than other loans that are charged on a compound basis, the loans have drawbacks. They do not generate any cash flow before term, are subordinated to conventional debt and mezzanine debt, and are generally not backed by a pledge of assets. In addition, PIK loans are usually treated as unsecured credit. They tend to lead to large losses in the event of a default.

From a borrower’s perspective, PIK loans may be utilized as a tranche or part of a bigger funding package to finance acquisitions and leveraged buyouts in general. However, it must be noted that it is fraught with risk and very high interest rates.

PIK loans can provide a company with the cash needed to recover or simply increase its indebtedness and multiply the lenders’ risks. Borrowers must weigh the benefits of the investments vis-à-vis their cost.

Oceanview Holdings Ltd., a provider of annuities and reinsurance solutions, has announced the establishment of its new subsidiary, Oceanview Secure Reinsurance Ltd., in the Cayman Islands. This expansion “strengthens Oceanview’s ability to deliver innovative reinsurance solutions globally,” a company release said.

Oceanview Secure Reinsurance Ltd. has received a Class D Insurer’s license by the Cayman Islands Monetary Authority (CIMA). This license will “complement and enhance Oceanview’s ability to provide global clients with advanced reinsurance options and will facilitate a broader array of customized reinsurance products to meet a wide variety of client requirements,” the release said.

Oceanview Holdings Ltd., established in 2018, provides retail annuities and asset-intensive reinsurance solutions through its subsidiaries. Oceanview Life and Annuity Company, an Alabama-domiciled insurer licensed in 47 states, and Oceanview Reinsurance, Ltd., a Bermuda Class E insurer, are rated “A” (Excellent) by A.M. Best. On a consolidated basis, Oceanview had over $12 billion in assets as of year-end 2023.

Investors Heritage Life’s (IHLIC) Long-Term Issuer Credit Rating (ICR) outlook has been down-graded to negative from stable by AM Best. The ratings agency affirmed the insurer’s Financial Strength Rating (FSR) of B++ (Good) and the Long-Term ICR of “bbb+” (Good). The FSR outlook is stable.

Given its ownership by Aquarian Holdings since 2018, its subsequent issuance of fixed indexed annuities, and its affiliation with Bermuda reinsurer Somerset Re, IHLIC fits RIJ’s definition of a “Bermuda Triangle” company. The company launched the Heritage Builder Multi-Year Guaranteed Annuity in 2018 and has since launched several fixed indexed annuity contracts.

The negative outlook for the Long-Term ICR reflects a decline in IHLIC’s risk-adjusted capitalization, as measured by Best’s Capital Adequacy Ratio (BCAR), to weak from adequate as of year-end 2023, an AM Best release said.

“Surplus declined throughout the year driven by operating losses, changes in asset valuation reserve, and changes in non-admitted assets. These factors were offset partially by realized gains in the investment portfolio. Risk-adjusted capital continued to decline into the first quarter of 2024 and operating losses accelerated due to new business strain from the sale of its fixed-indexed annuity products.

“The company is considering reinsurance arrangements currently to reduce surplus strain, and AM Best expects the company to contribute capital to support its annuity product sales growth in the near term. The balance sheet assessment has been revised to reflect these factors,” the release said.

The Credit Ratings reflect the insurer’s balance sheet strength, which AM Best assesses as adequate, as well as its adequate operating performance, neutral business profile and appropriate enterprise risk management.

IHLIC’s business profile was revised to neutral from limited, which is supported by its product and geographic diversification. Its improvements in market position, product concentration, and geographic concentration combined with its innovation initiatives should make the company more resilient to shocks in the market, AM Best said.

© 2024 RIJ Publishing LLC. All rights reserved.

The resemblances between today’s Bermuda Triangle strategy and the business model that Executive Life used in the years leading up to its record-breaking bankruptcy in 1991 are too many and too striking to be chalked up to coincidence, confirmation bias, or hindsight.

When I’ve asked, What could go wrong with the Bermuda Triangle strategy?, annuity industry veterans referred me to Executive Life (ELIC), its parent, First Executive Corp., and its fellow insurer, ELIC-NY. While researching the rise and fall of those companies, I found a prototype of today’s Bermuda Triangle.

The many books, news articles, and academic papers about ELIC and its helmsmen show a clear through-line from the treasure map drawn by ELIC CEO Fred Carr and “junk bond king” Michael Milken in the 1980s to the three-part strategy—nicknamed the Bermuda Triangle by RIJ—that Athene/Apollo, Global Atlantic/KKR, F&G/Blackstone, and others practice today.

The fixed deferred annuities that Carr sold, the junk bonds that Milken fabricated at Drexel Burnham Lambert, and the “surplus relief” that actuary Al Jacob arranged for ELIC, map closely to the annuities that Bermuda Triangle insurers sell, the private debt that their alternative asset manager-owners issue, and the “financial reinsurance” that helps them shrink their capital requirements.

Privacy and opacity, relative to public markets, was essential to both sets of financiers. And, remarkably, some of the personnel from the 1980s are still very much with us. Three prime movers of the Bermuda Triangle strategy—Apollo co-founders Leon Black, Marc Rowan, and Josh Harris—were protégés of Milken at Drexel Burnham Lambert.

The zig-zagging interest rates of the 1970s and 1980s had many consequences—good and bad, immediate and delayed, intended and otherwise—one of which was the opportunity for newer and nimbler life insurers to attract lots of money by selling high-yield but guaranteed single-premium deferred annuities (SPDAs).

ELIC’s SPDAs offered some of the highest yields, which made them easy for commissioned, insurance-licensed stockbrokers at the big brokerages to sell. “[SPDAs] are pure spread products, and in the 1980s, Executive Life had the spreads!” wrote former ELIC executive Gary Schulte in his book on Carr and ELIC, The Fall of First Executive (Harper Business, 1991). “The single pay segment of the company grew from nothing to about $13 billion companywide” [Schulte, p. 102].

To trick-out his contracts, Carr relied on the artistry of a versatile consulting actuary named Al Jacob. “A charming guy with an unusually creative spark,” as a fellow actuary described him to RIJ, Jacob designed catchy contracts like the “Ten-Strike” annuity, whose guaranteed rate increased by 10 basis points a year for 10 years. (Jacob is now deceased, but his family’s DataLife.com website survives.)

Today’s Bermuda Triangle life/annuity companies also sell SPDAs (now known as fixed-rate annuities or multi-year guaranteed rate annuities), albeit at much more modest guaranteed rates than in the 1980s. But their bread-and-butter product (until Fed “tightening” in 2022 turned simple fixed-rate annuities into hotcakes) has been the fixed indexed annuity, or FIA.

Built for the same mature, cautious savers, and with a similar no-loss guarantee, FIAs are actually quite different from SPDAs. FIAs offer a kind of floating rate that’s correlated with the performance of options on equity indexes. Their returns correlate mainly to stocks, which reduces their sensitivity to interest rate risk.

FIAs cost more to manufacture than SPDAs because there are more cooks in the soup. In their most recent iterations, FIAs use proprietary, custom-made indexes and volatility controls that help their issuers iron out the chance of suffering big, unanticipated claims. Providers of those indexes and controls have to be paid.

Distribution costs of FIAs (i.e., sales commissions) are higher than SPDAs’, but FIA contracts are “stickier”—that is, their contract terms (up to 10 years) are longer and their penalties for premature withdrawal are higher than SPDAs’. As long-dated liabilities, they match up well with the illiquid private loans originated by Bermuda Triangle investment companies with annuity-issuing subsidiaries: Apollo, Ares, Blackstone, Brookfield, Eldridge, Golden Gate, KKR, and others.

To get people to buy his SPDAs, Carr had to promise competition-crushing rates of return, and to do that he needed a steady, reliable source of IOUs that promised ELIC consistently high returns. Carr found that source when he took a meeting with fellow Los Angeleno Michael Milken.

Milken started out as a bottom-feeding bond trader, feasting on the bargains that rising rates indiscriminately created out of the debt of both weak and strong companies starting in the 1970s. Then he began creating his own high-yield paper—the famous below-investment-grade “junk bonds”— to finance leveraged loans, acquisitions, and buyouts.

Milken and Carr gave each other what they needed, and plenty of it. “The new breed of high-yield corporate bonds gave the kinds of spreads that would allow Carr to give the policyholder an interest rate unlike anything ever to come out of a life insurance company… Junk bonds gave Carr all he needed to dominate the single premium deferred annuity market with stockbrokers,” Schulte wrote [p. 35]. In A License to Steal, his 1992 book on Milken, Ben Stein wrote that ELIC was not the only life insurer shipping policyholder money to Milken. But it did so reliably, by the billions, and with little documented due diligence. “Carr just bought what Mike said to buy,” a junk bond buyer at another life insurer told Stein [p. 93].

Debt securitization, a financial magic trick that Lewis Ranieri of Salomon Brothers conjured up in the 1980s, helped Carr and Milken obscure ELIC’s concentration in low-grade bonds. According to Vic Modugno, an ELIC actuary in the 1980s and author of Broken Promises, a 1992 book about ELIC, they bundled Milken’s bonds into collateralized bond obligations, or CBOs, whose senior “tranches” were deemed sufficiently creditworthy for life insurers to buy.

Today, in the Bermuda Triangle, private credit, leveraged loans, and collateralized loan obligations are clearly descendants of Milken’s junk bonds and CBOs. The Economist’s Buttonwood columnist recently noted that junk bonds, private equity, and private credit each represent a different stage in “the history of leveraged finance.”

On the strength of its SPDA sales, ELIC soared dangerously close to the blazing sun of insolvency. For new life/annuity companies, rapid growth is a mixed blessing. If a client buys a million-dollar deferred annuity, for example, the insurer might have to contribute perhaps $50,000 to $100,000 of its own money in support of its guarantees. The more extravagant the guarantees of the contract, as in ELIC’s case, the larger the requirement for capital in the form of “deficiency reserves.”

ELIC “guaranteed high interest for a significant period of time. Normally, that would create a lot of deficiency reserves. If you were guaranteeing 8%, 9%, 10%, 11% returns, that creates a tremendous deficiency. No one could live under such a situation. So they went to overseas insurers who didn’t require deficiency reserves,” a former actuarial colleague and friend of Al Jacob told RIJ.

For surplus relief—an expression that describes the elimination of demands for fresh capital—an insurance company can use reinsurance. Faced with growing pains, ELIC periodically obtained so-called financial reinsurance, which papered over its capital shortfalls rather than filling the holes with real money.

To obtain this form of reinsurance, Jacob “was forever going down to the Cayman Islands,” his former colleague told RIJ. “He had set up some insurance companies there. It was not uncommon to have deals where potentially they could get letters of credit from a Cayman reinsurer that were as good as cash, as opposed to having huge reserves. My suspicion is that if you did it in the US you’d have to have assets equal to the letters of credit backing you. But lax capital requirements in Grand Cayman in the 1980s may have made it feasible to use that as a jurisdiction.”

“Because of the capital intensity of life insurance products, particularly annuities, [Executive Life] experienced terrible surplus strain from our growth,” former ELIC executive and author Gary Schulte told RIJ. “To relieve it, Al Jacob created the Bermuda Triangle strategy. He got letters of credit and reinsurance deals.” As in the case of ELIC’s investments, these deals were executed by individuals acting in concert, not true counterparties. One of the offshore reinsurers Jacob used, First Stratford, was co-owned by Carr and Milken.

“The main reason for doing that was surplus relief,” Modugno told RIJ in an interview. “In statutory accounting, you have to set up reserves that are higher than the premium you’re taking in. To get rid of that obligation, you do funds-withheld reinsurance. You’re taking liabilities off the balance sheet, so it looks like they’re not there.”

Today’s use of reinsurance by Bermuda Triangle companies is much more sophisticated than that arranged by Jacob. It can involve the efforts of teams of attorneys and actuaries in newly built office towers in Bermuda or the Cayman Islands. But it continues to provide profit-enhancing surplus relief, and its success continues to rely on the coordinated efforts of affiliated asset managers, insurers, and reinsurers.

Aside from the similarities in their annuity products, general account investments, and use of financial reinsurance, the business models of Carr’s life insurers and the Bermuda Triangle conglomerates also shared a reliance on transactions in private, less-regulated parts of the financial system and on coordination of activities among closely related businesses and people.

Characteristically, the Bermuda Triangle involves asset managers, insurers, and reinsurers in the same holding company. Operating in areas that require less transparency, less reporting, and less regulation, they get into and out of deals with maximum speed and minimum friction.

As noted above, players from the 1980s appeared in the 2010s, and at least three key people participated in both the ELIC episode and the birth of the Bermuda Triangle. Leon Black, Josh Harris, and Marc Rowan worked for Milken at Drexel Burnham Lambert. Black, whose financial and legal dealings with now-deceased convicted sex trafficker Jeffrey Epstein cost him the CEO job at Apollo in 2021, was once Milken’s “right-hand man,” according to Time magazine.

Black, Harris, and Rowan started Apollo Global Management in 1990 with billions of dollars in assets that Black and Credit Lyonnais, the French bank, salvaged from the ELIC bankruptcy, contributing to the reduction of annuity benefits to policyholders. (See “The Collapse of Executive Life Insurance Co. and Its Impact on Policyholders,” U.S. G.P.O., 2003.)

After 2009, Apollo invested in the crisis-weakened life/annuity business. It started Athene Holding, converted Aviva USA to Athene Annuity and Life, became a leading issuer of FIAs, and became brought vast amounts of annuity liabilities under its own management. With the creation of Bermuda-based Athene Life Re, the Bermuda Triangle strategy was born, soon to be emulated by a horde of large and small “alternative” asset managers and their pop-up life/annuity companies and reinsurers.

© 2024 RIJ Publishing LLC. All rights reserved.

In 2012, then-United Technologies Corporation embarked on a grand retirement income experiment. The giant defense contractor closed its defined benefit pension and began offering participants in its 401(k) defined contribution plan a deferred variable annuity (VA) instead.

The new “in-plan” annuity was built for UTC (now RTX Corp.) by investment company AllianceBernstein (AB), which managed the participant savings. AB engaged three life insurers to share the risks and rewards of underwriting the VA’s pension-like retirement income feature.

AB calls the product, “Secure Income Portfolio” or SIP. Despite its complex internal machinery, it worked. In 2014, AB adopted SIP for its own 401(k) plan. In 2019, the Illinois State Universities Retirement System signed on. According to AB, there’s currently about $4 billion in the SIP variable annuity.

“This is the most flexible in-plan retirement income solution on the market today,” Kevin Hanney told RIJ. A former senior director of pension investments at UTC and now consultant at CapitalArts Global, Hanney helped onboard the first version of SIP and Lifetime Income Strategy (LIS), AB’s target date fund, at that company.

Now, AB and its life insurance partners—Jackson National, Lincoln National, and Nationwide—are pitching SIP and LIS to the wider plan sponsor market. Like other insurers and asset managers, they’re counting on the 2019 and 2022 SECURE Acts to encourage the integration of retirement income solutions into 401(k) plans.

SIP works much like any deferred variable annuity with a guaranteed lifetime withdrawal benefit rider, except that the annuity gets funded incrementally instead of at one time. As participants of the same age gradually shift savings from other 401(k) funds to SIP, the life insurers periodically cover those discrete clusters of contributions with guarantees that entitle participants to a certain amount of future income.

SIP is a collective investment trust (CIT) rather than mutual fund. Its assets consist of 50% equities (33% US and 17% non-US) and 50% fixed income (30% core bonds and 20% US Treasury Inflation-Protected Securities). These asset allocations remain fixed, even after participants retire.

When participants retire, the SIP’s income rider kicks in. At 65, give or take a few years, retirees can start receiving an income stream—a percentage of the SIP’s highest value—that’s guaranteed to last as long as the owner is living. The owner may be a single person or couple.

For insurers, annuities with income riders are hard to price. Contract owners can drop the rider at any time. They can move money out of SIP, before or during retirement. SIP’s 120 to 129 basis-point fee pays for the management of SIP assets, the floor that the insurer put under the income-generating value of SIP assets, and the cost to the insurer of keeping the money liquid for the participant (as pension law requires).

AB gives plan sponsors two way to adopt SIP. Plans can use SIP as a component inside AB’s own Lifetime Income Strategy (LIS) target date fund (TDF) series (into which auto-enrolled participants can be directed). Alternately, plans can offer SIP as a stand-alone option in their investment menu. Plan sponsors can keep their current TDF and still add SIP to the menu.

“This solution is designed for flexible implementation, adapting to plans’ diverse needs and preferences—whether it’s alongside a plan’s existing target-date fund, as an allocation in a managed account or in a ‘do-it-yourself’ approach, with participants selecting AB’s Secure Income Portfolio from their plan’s core menu,” AB said in a release.

If SIP is inside the AB LIS TDF, money will start moving automatically to the SIP when the participant reaches age 50 or so. If SIP is outside a TDF, participants decide when and how much money to move into—or out of—SIP. Some participants will start contributing to the annuity at age 50. Others might wait until just before they retire.

The sooner participants start putting money in SIP, the sooner they start paying its fee. Lest plan sponsors worry that auto-enrolled participants might someday object to having paid 120 basis points in fees every year for 15 years for a benefit they’ll never use, AB gives them sponsors control over SIP start date.

“Plan sponsors can set the buy-in period,” said Andrew Stumacher, managing director, Custom DC Solutions at AB, in an email to RIJ. “The plan sponsor may only want participants to begin purchasing the guaranteed income component one year prior to retirement so that participants are much less likely to pay fees on an income benefit they did not want.”

The AB program’s key distinction is its use of several annuity providers (life insurers) at once. The multi-insurer approach means that plan sponsors aren’t putting all their eggs in one insurer’s basket. AB assumes “fiduciary” responsibility for vetting and selecting the specific annuity providers. Plan sponsors can remove or replace an insurer if they wish.

Participants, meanwhile, get the benefit of competition. Each quarter, when insurers enter bids on SIP assets, they are effectively offering future retirement income to cohorts of same-age participants for different prices. The bids are driven by current interest rates, market volatility, and the insurers’ own desire or capacity for the business.

In an illustration found in AB’s website, one hypothetical insurer offered to pay participants 3.9% of a specific tranche of savings for life starting at age 65. A second insurer bid 4.1%. A third bid 4.4%. The bids were added together to produce a weighted average payout at age 65 of 4.2% for a single quarter’s block of business.

In retirement, SIP contract owners would receive an annual payout calculated by multiplying the average of all the bids by the highest value of their SIP portfolios. If a participant decides to start receiving income later (or earlier) than age 65, their payout rates would be adjusted up (or down) according to their life expectancy.

Based on the insurers’ bids, an AB algorithm metes out a proportionate share of the business—and of the fees—to each participating insurer. In the hypothetical scenario above, the insurers who bid 3.9% were awarded 26% of the quarterly tranche, the bidder of 4.1% got 32%, and the bidder of 4.4% got 42%. The auctions occur every quarter.

A competitive, pre-retirement bidding process allows participants to “dollar-cost average” their way into an annuity. “They’re buying a little bit of income at a time over a multi-year period. They’re not waiting to make a single big purchase, which could happen at an inopportune time or right after a down market,” Stumacher said.

The bidding process also lets the life insurers manage their costs under the threat of unpredictable market conditions. If the insurers’ cost of writing SIP guarantees rises—because of interest rate changes or market volatility—the insurers can’t pass the cost along to the plans; SIP fees are fixed at 120 to 129 basis points. Within limits imposed by the competitive bidding process, the insurers can share the changes in their own costs with participants by raising or lowering their bids.

© 2024 RIJ Publishing LLC. All rights reserved.

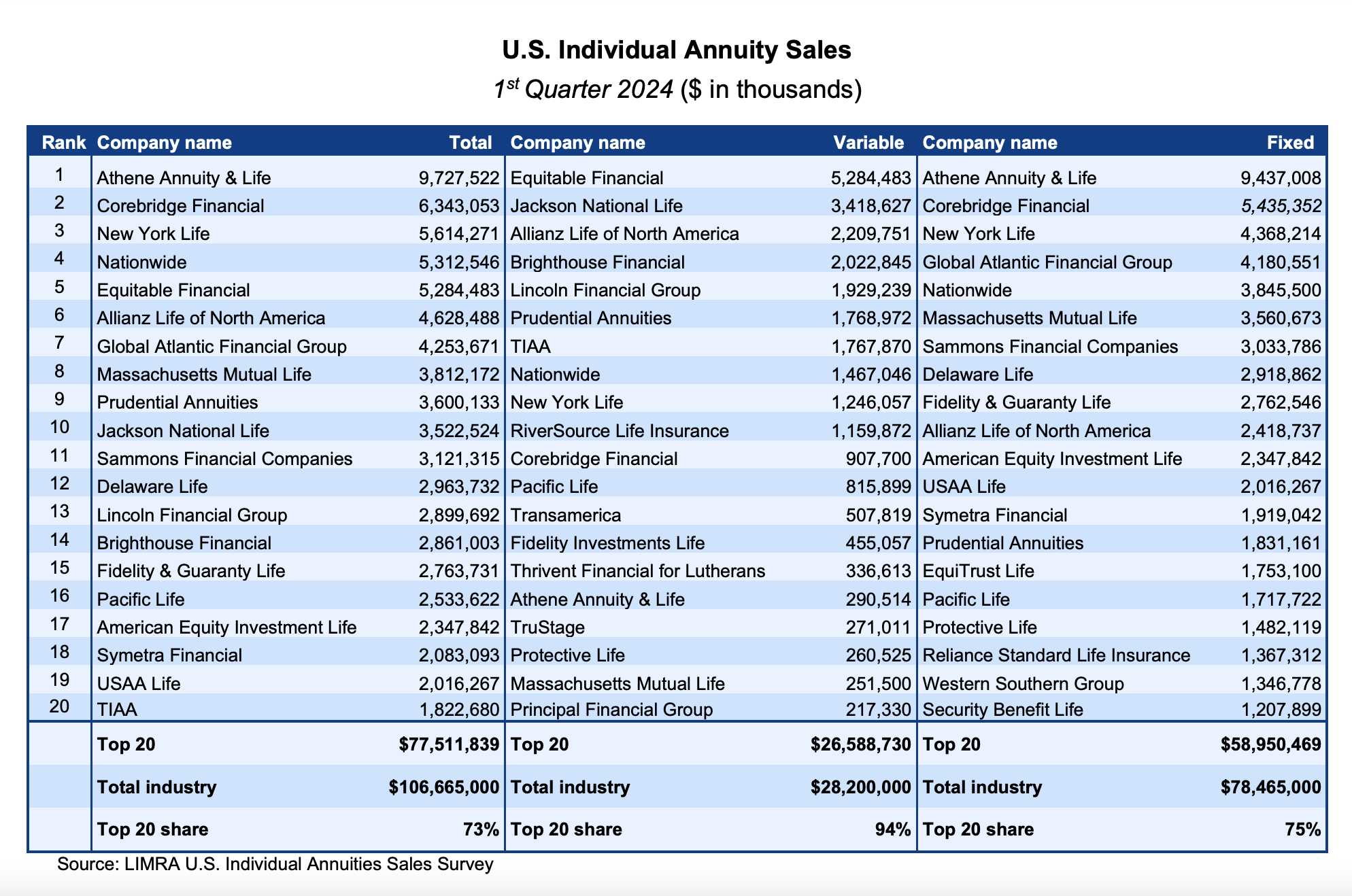

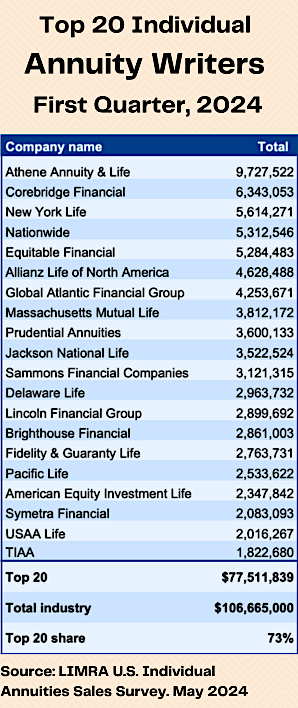

U.S. annuity sales were $106.7 billion in the first quarter of 2024, 13% above prior year results, according to results from LIMRA’s U.S. Individual Annuity Sales Survey. This is the highest first quarter sales results since LIMRA started tracking sales in the 1980s. The survey covers 92% of the total U.S. annuity market.

“Demand for investment protection and guaranteed retirement income remains strong. This is the 14th consecutive quarter of year-over-year growth in the U.S. annuity market,” said Bryan Hodgens, head of LIMRA research, in a press release.

“That said, total annuity sales have come down from fourth quarter 2024, largely due to a softening in the fixed-rate deferred annuity market. However, LIMRA expects annuity sales to perform well through 2024.”

Fixed-Rate Deferred

Total fixed-rate deferred annuity (FRD) sales were $43 billion in the first quarter, 4% higher than first quarter 2023 sales. This is the ninth consecutive quarter of growth for FRD annuity sales. FRD annuities remain the primary driver of annuity sales growth, representing more than 40% of the total annuity market in the first quarter.

Fixed indexed annuities

Fixed indexed annuity (FIA) sales had a record first quarter. FIA sales totaled $28.6 billion, up 24% from the prior year. FIA sales have experienced 12 consecutive quarters of year-over-year growth.

“Growth was widespread with 61% of FIA carriers and 8 of the top 10 carriers reporting sales growth,” the release said. “Sustained strong interest rates have allowed carriers to improve FIA crediting rates and raise cap rates, which increased the overall product line attractiveness. LIMRA expects FIA sales to continue to grow through 2025.”

Income annuities

Income annuity product sales continue to thrive under the higher interest rates. Single premium immediate annuity (SPIA) sales were $3.6 billion in the first quarter, 6% higher than the prior year’s results. Deferred income annuity (DIA) sales were $1.2 billion in the first quarter, increasing 40% year over year.

Registered index-linked annuities

For the fourth consecutive quarter, registered index-linked annuity (RILA) registered record quarterly sales. RILA sales increased 39% in the first quarter to $14.5 billion.

“For the second consecutive quarter, RILA sales outperformed traditional variable annuities (VAs). RILA sales should continue to outpace traditional VA sales throughout 2024. LIMRA is forecasting RILA sales to surpass $50 billion in 2024,” the release said.

Traditional variable annuities

Traditional VA sales improved in the first quarter, up 7% year over year to $13.7 billion.

“While traditional variable annuity sales grew in the first quarter, sales remain historically low,” said the release. “Today’s investors have more annuity options to achieve their accumulation goals than they did a decade ago.”

© 2024 RIJ Publishing LLC. All rights reserved.

So many annuities, so little time. For 401(k) plan sponsors who feel inclined to add a guaranteed income option to their plans, the learning curve is likely to be steep and high. In-plan or out-of-plan annuity? Fixed, fixed indexed, or variable? Which life/annuity company?

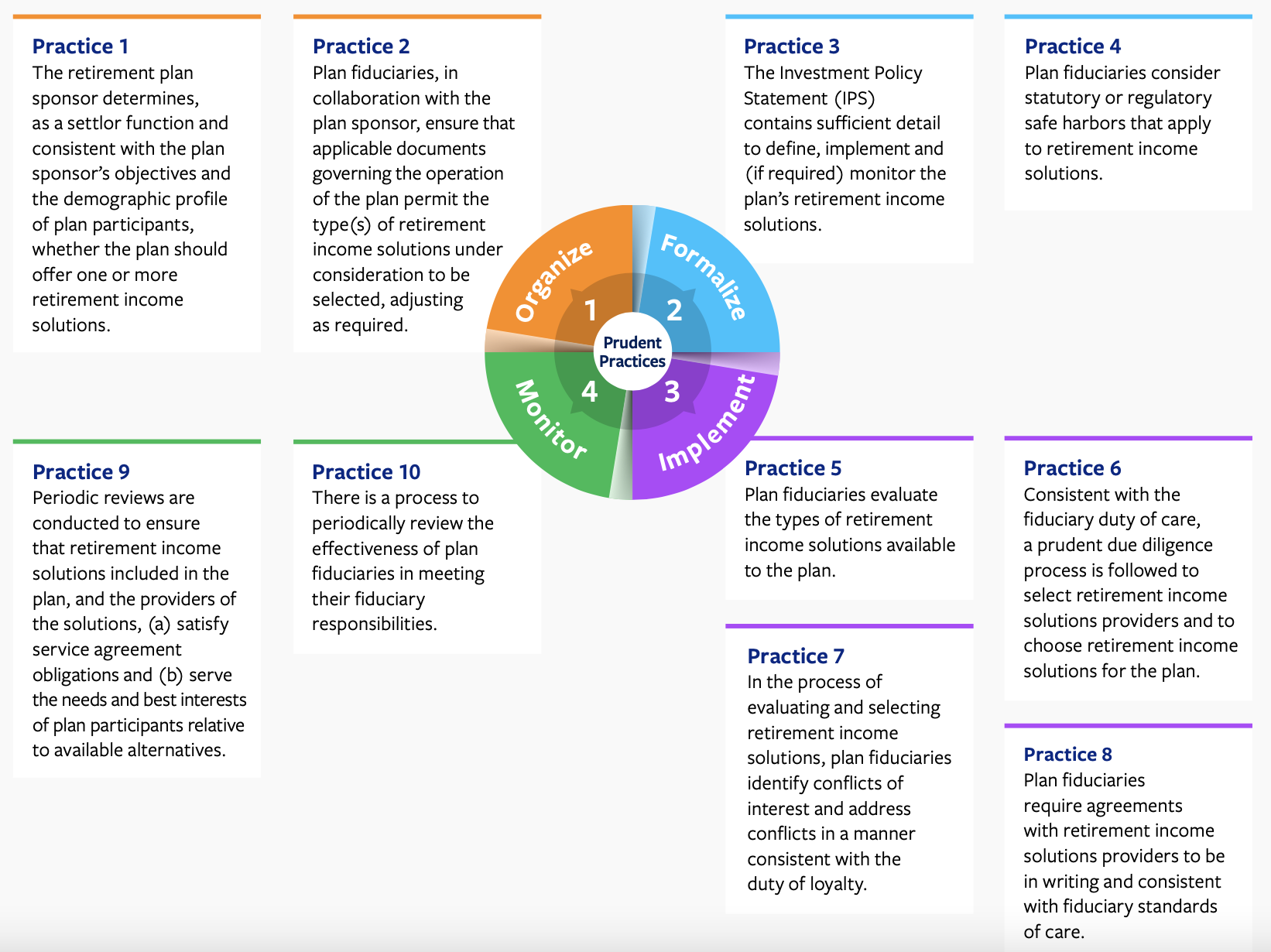

A new whitepaper aims to flatten and shorten that curve. The 39-page document, “Prudent Practices for Retirement Income Solutions,” is sponsored by companies with both long experience and substantial stakes in the growth of the 401(k) annuity phenomenon.

Led by Broadridge Financial Solutions, the group includes Broadridge’s fi360 service for plan fiduciaries, annuity product data providers CANNEX and The Index Standard, internet “connectivity” provider, Micruity, and ERISA lawyer Fred Reich of Faegre Drinker Biddle & Reath.

Broadridge is not alone in anticipating the need for guides to assessing 401(k) annuities. “[The National Association of Plan Advisors] has already developed an education program for plan advisors to help them understand the process for evaluating lifetime income options. PSCA [Plan Sponsor Council of America] is in the process of doing the same for plan sponsors to be launched toward the end of this year,” Brian Graff, CEO of the American Retirement Association, the umbrella organization that includes NAPA and PSCA, told RIJ last week.

The Broadridge whitepaper suggests a process that plan “fiduciaries”—consultants whom the Employee Retirement Income Security Act of 1974 requires to act solely in the best interest of plan participants when recommending or managing plan investments or administering a plan—can use if and when selecting one or more decumulation strategies for the plan.

“We’re focused on increasing consideration of retirement income in 401(k) plans. A rising tide will lift all ships, so it benefits everyone [to] have a standard way of looking at it and educating the market,” Broadridge’s John Faustino told RIJ in a recent interview. “Plan sponsor advisers will be able to use our technology to identify the options and needs of a given plan and monitor it on automated basis.”

The ten-step process is described in the table below, reprinted from the whitepaper.

According to Faustino, three types of income tools are available to plan sponsors: fixed income annuities, target date funds with flexible lifetime withdrawal benefit riders, and managed payout programs without guarantees.

“A lot of our work is focused on hybrid and insurance side. But the consortium advocates for consideration of introducing retirement income while purposely staying away from making recommendations,” Faustino told RIJ. Broadridge intends to involve other retirement trade groups in the consortium’s work. Faustino mentioned LIMRA, SPARK Institute, and the American Retirement Association.

Together, these groups are encouraging and preparing themselves for a world made achievable by the SECURE Acts, passed by Congress in 2019 and 2022. The first SECURE Act introduced a new “safe harbor” that was meant to “remove the plan fiduciary’s fears that it would have to make a determination as to the viability of an insurer to provide lifetime benefits, and the concern that it could be liable for the future insolvency of an insurance carrier the plan fiduciary may select,” according to the white paper.

If, as appears to be the case, the push for annuities in 401(k) plans has come mainly from insurers and asset managers—more than from plan sponsors or plan participants—then it’s not surprising to see the push for education about annuities and retirement income coming from the same source. The Broadridge initiative bears that out.

Some surveys have shown that participants want retirement income tools, at least in principle. But most participants aren’t asking plan sponsors for annuities. At the most recent national conference of the Plan Sponsor Council of America, a panel took up the question of retirement income solutions in plans.

In a report on the PSCA website’s news page, the author wrote, “A refrain heard a few times throughout the conference was ‘retirement income products are like automatic enrollment, participants weren’t asking to be auto-enrolled, but the solution was developed to meet a need and is now commonplace.’ This refrain seems to be pushing back against the notion that there isn’t a need for retirement income solutions because no one is asking for them.”

The largest plan sponsors are likely to be the first to adopt income solutions, to be among the first to be approached by annuity providers, and to be able to dedicate the most resources to educating participants about retirement income. Of some 710,000 defined contribution plans in the US, about 1,200 have at least 10,000 participants. These large plans account have 42.1 million participants (42% of the total participant population) and $3.6 trillion in plan assets (46% of total DC assets).

© 2024 RIJ Publishing LLC. All rights reserved.

A “pension risk transfer” or PRT allows a company to swap its traditional defined benefit plan for a group annuity issued by a life insurer. To help ensure that plan participants get their benefits from the life insurer in retirement, US pension law requires companies to select the “safest available annuity.”

A federal class action suit, filed last March 13, charged aerospace and defense contractor Lockheed Martin and its plan adviser, State Street Global Advisors, with failing to pick the safest available annuity in 2021 when they replaced Lockheed’s $9 billion pension with a group annuity from Athene Life and Annuity, a leading life/annuity company. The suit was filed by a group of the plan’s participants.

The lawsuit is noteworthy. Athene was the largest seller of annuities in the US in the first quarter of 2021, with $9.73 billion in sales, and it executed the largest PRT transaction of 2023: the transfer of AT&T’s $8.05 billion pension to an Athene annuity. St. Louis attorney Jerry Schlichter, famous for his successful suits against defined contribution plan sponsors for not protecting their participants from high fees, co-filed the suit against State Street and Lockheed.

Thomas D. Gober

On May 28, in a new filing on behalf of the plaintiffs, certified fraud examiner Thomas D. Gober charged that State Street shouldn’t have recommended Athene to Lockheed, and that Lockheed shouldn’t have bought its group annuity from Athene, because of what Gober described as Athene’s thin surplus, illiquid investments and use of opaque offshore reinsurance with its own affiliates. Athene itself is not a defendant in the case.

The fraud examiner’s 16-page filing said, in part:

By Apollo causing most of the business to be sent to offshore affiliates that do not file under SAP [statutory accounting principles], it makes opaque the solvency or liquidity of the offshore reinsurers. Relevant here, as of December 31, 2023, Athene Iowa is counting on more than $155 billion of reinsurance with its own captives and offshore affiliates.

Comparing that amount in affiliated reinsurance with Athene Iowa’s total reported surplus (its only buffer between a viable carrier and one in receivership) of $2.88 billion [1.44%, or assets of $202 billion divided by liabilities of $199 billion] the gravity of the lack of transparency and risk of the offshore reinsurers is of great concern.

The fact that the Bermuda-based Athene Re controls such a large percentage of Athene Iowa’s assets would make an orderly liquidation under state insurance laws unwieldy and costly as marshaling assets located in Bermuda for the benefit of pensioners will not be a simple and straightforward process.

The surpluses of other large life/annuity companies, such as TIAA (13.83%), New York Life (12.24%), Nationwide (6.77%), and Pacific Life (6.5%) are much higher than Athene’s, Gober said.

Athene rejects the allegations. An Athene spokesperson told RIJ in a May 30 email:

These are baseless complaints instigated by class action attorneys who are attempting to enrich themselves at the expense of retirees. Athene is a safe and secure provider of annuity benefits, with outstanding financial strength, proper reserves, excellent capitalization, and strong credit ratings.

Pension group annuities provide many protections that enhance retirement security. Insurers like Athene have deep expertise in managing annuity obligations, are subject to robust regulation, and hold regulatory capital to protect policyholders.

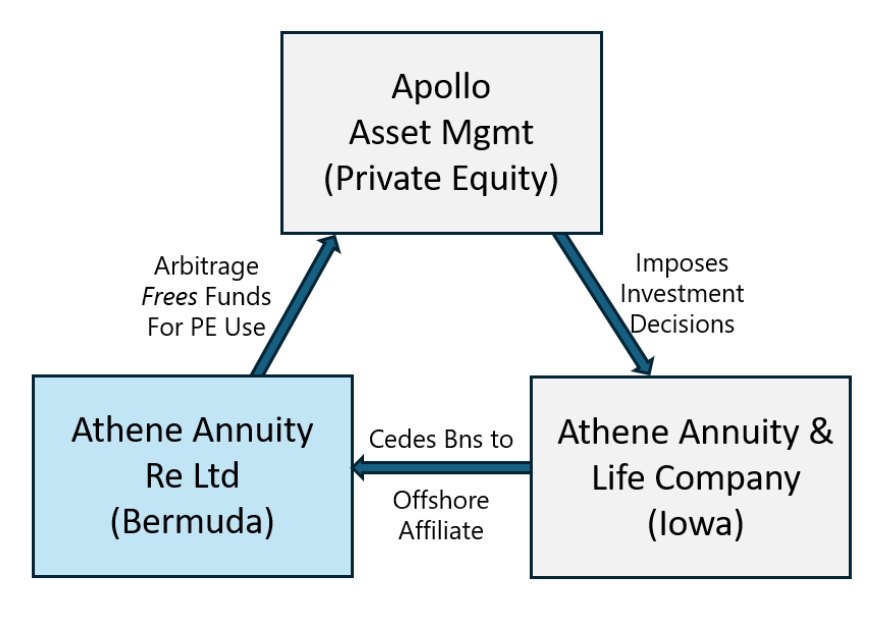

The suit may serve as a test of the legal soundness of what RIJ has called the “Bermuda Triangle” strategy, a business model initiated by Athene and copied by other annuity issuers. In Gober’s statement, he referred to the model as the “Bermuda triangle” and illustrated it with this graphic:

The strategy varies in its details but typically involves a US life/annuity company that sells fixed rate or fixed indexed annuities, a Bermuda or Cayman-based reinsurer, and a large asset manager or investment firm that devotes a portion of the annuity reserves to investments in “alternative” assets, such as collateralized loan obligations and asset-backed securities. In the strategy, all three entities are often affiliated or part of the same holding company.

Practitioners of the Bermuda Triangle business model claim that the reinsurance reduces capital requirements and alternative assets bring in higher investment yields. This allows annuity issuers to offer higher crediting rates for annuity policyholders and higher profits for equity shareholders—a win-win for all stakeholders.

Critics claim that the strategy produces under-capitalized, shakier life/annuity companies, and that without the use of questionable “regulatory arbitrage” between the US and reinsurance havens like Bermuda, some of those life insurers would be insolvent.

The regulation at the heart of this case, Instructional Bulletin 95-1, “was issued on March 6, 1995, in the wake of the failure of Executive Life Insurance Companies of California and New York,” according to a Department of Labor document. “[IB 95-1] provides guidance to pension plans considering the purchase of annuities ‘to transfer liability for benefits purchased under the plan to [an] annuity provider.’ IB 95-1 also emphasizes the fiduciary responsibility owed to plan participants in the selection of the ‘safest annuity available’ and makes it clear that ‘[c]ost consideration may not … justify the purchase of an unsafe annuity;’ nor is it appropriate to rely solely on insurance rating services.”

A June 4 Best’s Special Report, “Annuity Premiums Soar, Surrender Protection Strengthens,” states that annuity products have been attractive for consumers in the last few years, propelled by the rising interest rate environment and crediting rates that generally have been higher than competing products offered by larger national banks.

As insurers look to capitalize on the favorable environment, newer market entrants have added much-needed capacity to the market, particularly through multiyear guaranteed annuities (MYGA) with their attractive interest rate spreads and shorter durations. With the overall 2023 premium growth, annuity writers posted a 68% year-over-year increase in indexed annuity net premium income to $28.9 billion; 48% growth in fixed deferred annuities; and a 33% increase in premium for variable annuities without guarantees.

“Growth in the annuity market has heightened competition, as many new companies have entered the space, including several new private equity and asset management-backed insurers looking to capitalize on the difference between the cost of liabilities and potential favorable investment returns,” said Erik Miller, director, AM Best. [Emphasis added.]

Baby Boomers seeking income and wealth transfer solutions for trillions of dollars in assets is also driving consumer demand. Additionally, surrender benefits rose 32% in 2023; however, according to the report, the share of policies with market value adjustment surrender charges also has more than doubled in the last 10 years.

“Older annuity policies with lower rates were outside of the surrender charge protection, and so with the favorable crediting rates, insurers have been able to sell new annuity products with the higher rates to these customers while also locking them into policies with surrender charges,” said Jason Hopper, associate director, industry research and analytics, AM Best.

26North Reinsurance Holdings, which was founded in 2022 by one of the co-founders of Apollo Global Management, closed a $4.9 billion reinsurance deal with Life Insurance Company of the Southwest (LSW), a unit of National Life Insurance Co., 26N Re said in a release.

The deal will see a subsidiary of 26N Re reinsure a “seasoned and diversified” block of multi-year guarantee and fixed annuity products issued by LSW, the company said. LSW is a member company of National Life Group, which was founded in Vermont in 1848.

In addition, 26N Re agreed to provide a quota share reinsurance agreement for future fixed annuities issued by LSW. The transaction brings 26North’s total assets under management to approximately $22 billion.

“This transaction will significantly scale our reinsurance business and continue to diversify 26North’s platform,” said Josh Harris, founder of 26North and co-founder of Apollo in 1990, in a statement. “We believe that our culture of prudent risk management and strong governance allows 26N Re to partner with the highest-quality cedants who are looking to leverage our long-term capital and asset management expertise.”

Harris has a long history in private equity. He worked for Drexel Burnham Lambert for two years in the 1980s, left to get a degree at Harvard Business School, and then joined former Drexel partners Leon Black and Marc Rowan to establish Apollo Global Management in 1990, according to Harris’ Wikipedia page.

By then, Drexel had filed for bankruptcy due to illegal junk bond activity. A major investor in Drexel junk bonds (i.e., financer of Drexel’s leveraged buyouts), the Executive Life insurance companies, failed in 1991.

In a separate news release last month, Agam Capital, “an analytics-driven platform partnering with insurance companies to enhance their financial flexibility,” is advising and partnering with 26N Re in the formation and launch of AeCe ISA, Ltd. (“AeCe”), a Bermuda-domiciled Class E life and annuity reinsurer. Agam’s founders are Chak Raghunathan and Avi Katz.

National Life Group is a minority owner in AeCe, which will reinsure single premium deferred annuities written by LSW.

Agam’s “pALM” analytical platform and other Bermuda capabilities will support 26North in the development and establishment of a new entrant into the fast-growing market for life and retirement reinsurance solutions in Bermuda. Agam described pALM as a “proprietary asset and liability management (ALM) system” offering “a fully embedded dynamic strategic asset allocation (SAA) and enterprise risk management (ERM) infrastructure.”

As part of the launch, AeCe will leverage Agam’s Bermuda ISAC structure which offers a comprehensive suite of operational, management and governance services to Bermuda based reinsurers. Separately, Agam and AeCe entered into a long-term Management Services Agreement.

Clear Blue Insurance Co. and Aon plc, the insurance broker, will have until June 21 to present motions in Clear Blue’s lawsuit again the Aon plc and Aon Insurance Managers (Bermuda) Ltd. in a case related to the bankruptcy of the insurtech firm Vesttoo Ltd., AM Best reported in May.

Clear Blue seeks to recover damages from Aon for, according to the complaint, “hosting a rogue operation on its Bermuda-based platform in clear violation of law, regulation, contract and standard market practice.”

Clear Blue sued Aon in New York state court in 2023 for alleged damages connected with letters of credit issued by Vesttoo involving Aon and its Bermuda-based segregated cell entity, White Rock. The complaint said, “Clear Blue entered into a series of reinsurance transactions with and/or involving Aon, its wholly owned subsidiaries Aon Insurance Managers, White Rock and White Rock’s various segregated accounts, causing material financial, regulatory and reputational damage to Clear Blue.

“Aon and its entities could have stopped the Vesttoo fraud ‘dead in its tracks,’ but “facilitated it by removing all the statutory, regulatory and contractual safeguards and ignoring standard market practice.”

“This complaint is meritless,” an Aon spokesperson told AM Best. “Vesttoo has publicly admitted that its executives conspired with third parties in a highly sophisticated and elaborate fraud. As one of the victims of that fraud, Aon is focused on continuing our work to develop a path forward for all affected parties.”

The Supreme Court of Bermuda recently sanctioned a bankruptcy plan filed by Vesttoo creditors and approved the joint provisional liquidators (JPLs) of Aon’s White Rock Insurance SAC to remove objections to the Chapter 11 plan involving White Rock and other parties, AM Best said.

The Bermuda court’s decision, filed with the U.S. Bankruptcy Court for the District of Delaware, allows the JPLs to unconditionally withdraw their objections to previously proposed versions of the bankruptcy settlement plan and cedent settlements with the Official Committee of Unsecured Creditors of Vesttoo, appointed in the Vesttoo Chapter 11 case involving White Rock. The liquidators are also authorized to consent to confirmation of the plan.

The liquidators are also allowed to consent to cedent settlements with the committee and JPLs for White Rock involving insurers Clear Blue, Chaucer, Beazley plc., Markel Corp. and Porch, according to the Bermuda court ruling. Underwriting entities of Clear Blue parent Pine Brook Capital Partners II (Cayman) have current Best’s Financial Strength Ratings of A- (Excellent).

In May, AM Best downgraded the financial strength rating (FSR) to A (Excellent) from A+ (Superior) and the long-term issuer credit ratings (Long-Term ICR) to “a+” (Excellent) from “aa-” (Superior) of Everlake Life Insurance Company and Everlake Assurance Company, collectively known as Everlake Life Group (Everlake Life). Both companies are domiciled in Northbrook, IL.

According to AM Best:

The outlook of these Credit Ratings (ratings) has been revised to stable from negative. The ratings reflect Everlake Life’s balance sheet strength, which AM Best assesses as very strong, as well as its strong operating performance, neutral business profile and appropriate enterprise risk management (ERM).

The change in Everlake Life’s business profile assessment to neutral from favorable reflects the strong competitive environment for bidding on flow reinsurance of annuities; Everlake Life’s moderate market share and reserve profile; and is similar to peers with a strategy of seeking flow reinsurance of annuities.

Everlake Life’s reserve profile, which includes universal life with secondary guarantees and structured settlements, is unlikely to change in the near term, even with the successful acquisition of additional multiyear guarantee annuity business, which was done in 2023 and is expected to continue.

According to its website, Everlake Life Insurance Company and Everlake Assurance Company are US based insurance companies specializing in life insurance and annuities. Everlake U.S. Holdings Company purchased Allstate Life Insurance Company and Allstate Assurance Company on November 1, 2021.

Everlake Life has over 1.6 million policies in force and over $23 billion in assets under management. It also administers select policies issued by Lincoln Benefit Life Company, Surety Life Insurance Company, American Maturity Life Insurance Company, and Columbia Universal Life Insurance Company.

According to AM Best, Everlake Life’s balance sheet strength assessment benefits from its strongest level of risk-adjusted capitalization, as measured by Best’s Capital Adequacy Ratio (BCAR), prudent asset liability management and development of its own internal capital modeling. This is partially offset by affiliated reinsurance in support of a significant block of term life insurance.

The operating performance continues to be assessed as strong given the three- and five-year return on equity ratios, which compare well against other strong-level peers, in addition to diversified profits between ordinary life and individual annuity products.

Everlake Life’s growth will be dependent on management successfully executing its strategy to acquire new business given the run-off of a large in-force block, but management has recently been more successful in acquiring new business. The ERM approach employs a typical three lines of defense strategy, including individual risk owners in the business areas, an ERM committee and an audit risk committee that reports directly to the board of directors. Risk appetite and tolerance statements with limits and triggers are quantitative and clear.

Capital Income, Midland National’s first commission-free fixed index annuity (FIA), was named top fee-based fixed index annuity in 2023, according to LIMRA.

The product emerged from Midland Advisory, an internal team that Midland National Life formed in 2021 to design annuities for registered investment advisors (RIAs) and their clients. Midland is part of Sammons Financial Group.

Since its launch, Capital Income has consistently ranked high as a strong indexed annuity choice for advisors. In addition to earning the 2023 overall top spot from LIMRA, Midland National performed well in fourth quarter 2023 sales. Notable results from the Q4 2023 Wink Report include:

No. 3 Deferred Annuity Companies – RIA Distribution

Midland National Capital Income carries a guaranteed lifetime income rider with an income multiplier that can double income payments for up to five years for contract owners with health problems.

If a fee-based advisor does not have an insurance license but wants to provide a client with an annuity, Midland National makes Capital Income available through outsourced insurance desks that can act as agents of record. This enables the advisor to maintain discretionary authority over the client’s account.

© 2024 RIJ Publishing LLC. All rights reserved.

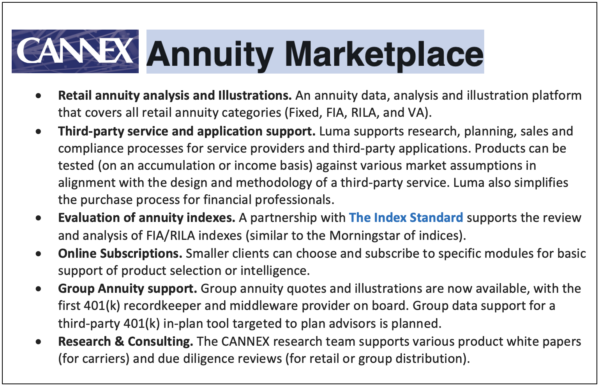

CANNEX, the annuity data provider, has partnered with Luma Financial Technologies, a fintech firm, to launch the CANNEX Annuity Marketplace. The new platform is designed to help financial professionals at small and mid-sized firms research, compare, and select annuities for clients.

Advisers, agents and retirement plan sponsors can use the platform, accessible through a portal on Luma’s website, to analyze the performance of hundreds of fixed, fixed indexed-linked, variable, and income annuities based on CANNEX’s annuity data, research, and illustration resources.

The Annuity Marketplace will provide income, rate, yield, and product information on annuities from more than 60 issuers, a CANNEX release said. Advisers can illustrate the outcomes of market scenarios and investment choices across products, asset allocations, riders, and annuity categories.

The proliferation of new annuity products, the expansion of annuity sales, and the passage of regulations that require advisers and agents to find products “consistent with best interest requirements and client goals” has increased “the importance of being able to understand and evaluate annuities on a standardized basis” said Gary Baker, president, CANNEX USA, in a release.

The proliferation of new annuity products, the expansion of annuity sales, and the passage of regulations that require advisers and agents to find products “consistent with best interest requirements and client goals” has increased “the importance of being able to understand and evaluate annuities on a standardized basis” said Gary Baker, president, CANNEX USA, in a release.

“The marketplace provides an important resource for financial professionals looking to help clients incorporate annuities into their financial plans,” added Jay Charles, director of Annuity Products, Luma Financial Technologies.

CANNEX is an independent financial data and research services company with operations in Canada and the U.S. Since 1984, it has provided data, analytics, illustrations and research services to insurance companies, banks, brokers, service providers and independent advisers.

Fintech software developed by Luma Financial Technologies is used by broker/dealer firms, RIA offices, and private banks worldwide. Founded in Cincinnati in 2018, Luma also has offices in New York, Zurich and Miami.

© 2024 RIJ Publishing LLC. All rights reserved.

Our financial lives would probably be both more difficult and easier if we all knew exactly when we would die. Personal credit would presumably dry up as the “deadline” approached. But deciding how much to save for retirement would be easier.

A new white paper from HealthView Services, a Danvers, MA-based firm that collects longevity data for advisers, financial institutions and employers, could help advisers estimate how much longer a 65-year-old is likely to live.

From a mountain of data gathered from 266 million people, HealthView teases out predictions that individuals and advisers can use in planning for retirement. The white paper shows, for instance, that 65-year-olds with no chronic health problems should expect to live to age 88 (if male) and age 90 (if female).

But only about one in 20 Americans are disease-free at age 65. People suffering from high blood pressure, diabetes, heart disease, cancer, and other chronic diseases die one to six years sooner. Men age 65 with diabetes have a life expectancy of only 79 years.

Turning the data around, the white paper also reports the probabilities of living to age 90 for people with various diseases. People with no chronic disease at age 65 have a one in five chance living to age 95 “and beyond.” Those with diabetes should forget about living to 95.

HealthView quantifies the somewhat morbid inverse relationship between life expectancy and spending capacity. Assuming a new retiree with $1.1 million in savings, the paper’s authors conclude that, compared with someone in excellent health, a high blood pressure sufferer could afford to spend $448,000 more in retirement, smokers can afford to spend $616,000 more, and diabetes sufferers can spend $728,000 more, because of their shorter life expectancies.

The white paper describes a hypothetical couple, both 55 years old. One has a history of diabetes and a life expectancy of age 82. The other is healthier and can expect to live to age 90. By HealthView’s calculation, the healthier partner can expect to spend $3.17 million in retirement (including Social Security benefits and income from an annuity) while the partner with diabetes can expect to spend only about $2 million.